The financial markets saw a substantial sell-off in risk assets today as all major US stock market indices closed down over 7%. Current market levels are roughly 1-2% away from levels that would signal a bear market (20% down from recent highs). The decline was so steep, market circuit breakers kicked in this morning, halting trading for 15 minutes. Market wide trading halts have not been triggered since 1997. Currency and commodities markets have also seen extreme moves.

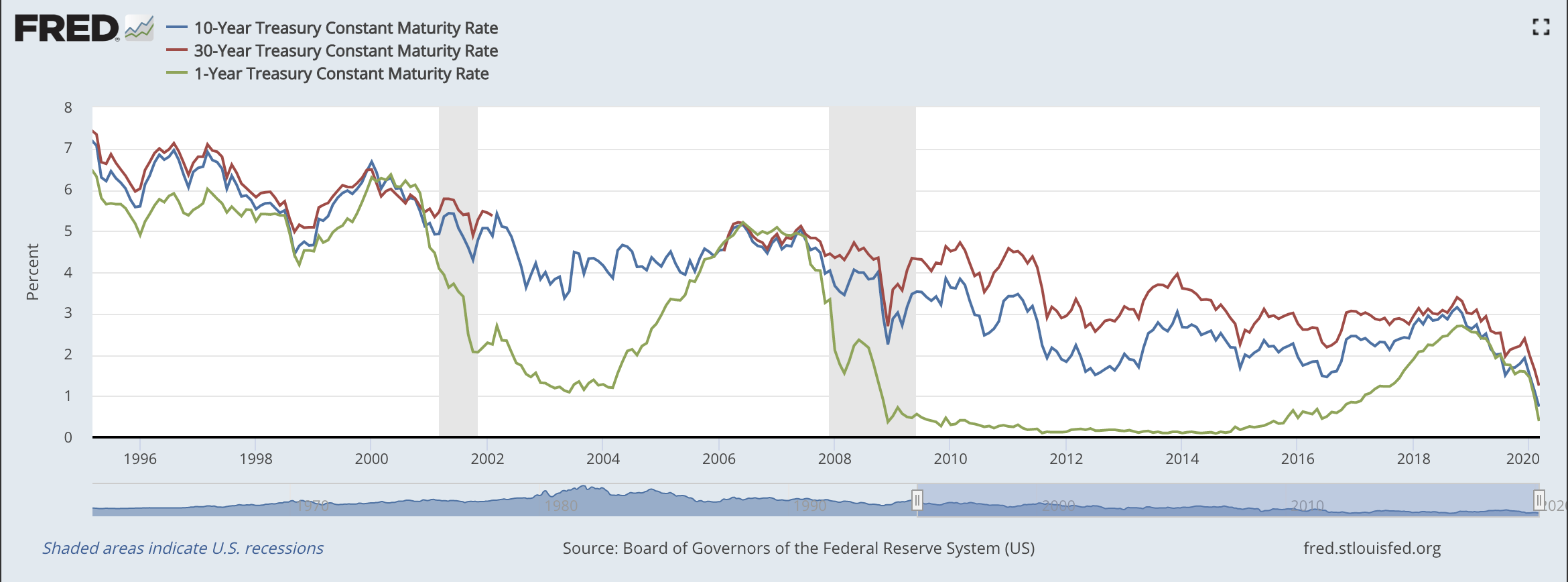

The moves in the bond market can only be described as unprecedented. The yield on the entire US Treasury bond curve is now below 1%. Investors are demanding less than 1% annual interest to lend to the US government for 30 years. These levels have never been seen before, and are indicative of a flight to low-risk assets by investors. Gold, another safe haven asset popular during volatile times, also reached a 7 year high today.

In our view, there are two precipitating factors for these moves:

We are at the end of an 11 year bull market where US equities have returned over 400%. Valuations were, and continue to be at high levels.

As we discussed in our note last week, the measures being taken to contain the Corona virus outbreak have an impact on economic activity and could lead much of the world into recession.

Our view on the first is not a surprise. to our readers. We have expressed our valuation concerns for several quarters and are not taken aback that the broader market has begun to share them.

On the second, we believe the measures required to contain this dangerous virus may easily have a significant impact on the economy. Several regions across the world, including all of Italy, have mandated quarantines and closed schools. Such steps can curtail economic activity for weeks. Major employers in the north-western US have mandated employees work from home. Many large US employers have curtailed non-essential travel. The impact on the airlines, hospitality and oil industries is already significant, with airline executives comparing the environment to the period after 9/11.

We believe there are significant risks that remain to be expressed. We have repeatedly asked ourselves where the good news is, and cannot come up with a good answer. The market is already pricing in zero interest rates for the next 30 years. Interest rate policy has effectively been neutered. The Federal Reserve has lost substantial credibility under this administration. The market seems skeptical of both fiscal and monetary stimulus, unconvinced either or both can prevent further drops.

We continue to advocate a defensive position and do not see a quick recovery to previous levels for risky assets like stocks. That said, with steep sell-offs come opportunities and we are looking closely at where to deploy capital when valuations become more favorable. We don’t think valuations are there yet, but at some point there will be an opportunity to buy high quality companies at discounted prices.

Please contact us if you would like to discuss your portfolio or investment allocation.

Regards,

Subir Grewal, CFA, CFP Louis Berger

What would a Bernie Sanders administration mean for the economy and markets?

With the Iowa, New Hampshire and Nevada largely behind us, and South Carolina tomorrow, the likelihood that Bernie Sanders will be the Democratic nominee for president has grown. 538 now places this probability at 40%. We believe it is time to meaningfully engage with this possibility and consider what it would mean for the US economy and the markets.

In our view, Sanders’ agenda is a robust response to rising income inequality and market failures in the 21st century. His biggest proposals, Medicare for All and College for All, enjoy majority support among voters. There is evidence to suggest US voters (particularly younger ones) are not as ideologically fixed as many assume. Lastly, since his initially quixotic 2016 campaign, Senator Sanders has succeeded in expanding the overton window, i.e. what is considered possible in US politics. We take his agenda seriously.

A full consideration of Sanders’ program will require more than a single blog post. We choose to begin with a look at Senator Sanders’ signature policy proposal, his Medicare For All plan. Other major policy proposals and stances will be considered in later installments. We should however, make some general thematic remarks on Senator Sanders policy platform.

Senator Sanders’ proposals are often presented as “radical”. In truth, they match the social democratic policies in place across much of Europe and the rest of the industrialized world. Proposals such as College for All align well with past US policy. College tuition at most public colleges in the 60s/70s was either very low or free.

Some of Sanders’ more ambitious policies attempt to tackle systemic risks related to market failures. His proposals to address climate change, extreme inequality and breaking up the largest banks are pretty conventional prescriptions to address the market’s inability to price externalities, protect the rule of law, and prevent speculative credit crises respectively. There is a case to be made that such measures would make our economic system more resilient and lay a lasting architecture for prosperity.

Many of Sanders’ policies have been enacted in other parts of the world so we have a benchmark to compare against. The United Kingdom, France, Italy and Canada have single-payer healthcare systems, few would claim this has impacted their long-term growth negatively. If anything, there is some evidence that the unpredictability of health care costs in the US has driven industrial production towards Canada, where a single payer system equalizes costs among employers.

We should also note that improving the health, well-being and longevity of the human population is a valuable and laudable goal. Even when using the narrow criteria of economic/GDP growth, healthcare and public health are critical. Our economy depends on human ingenuity to add value to material resources. Health and well-being are necessary to make this possible. The public health crisis that is the COVID-19 virus outbreak brings this into sharp relief. The rapid spread of this virus has already impacted economies and markets on multiple continents. Healthcare systems that are free at the point of service, with a strong primary care network lead to early diagnosis and response to such outbreaks. Imagine a healthcare system where people who are sick do not visit the doctor because they cannot shoulder the costs, or worse yet, continue to work because they do not have paid sick leave. Both have deleterious effects on short-term economic activity and long-term potential, by impacting human capital.

We assume most readers are familiar with the contours of Senator Sanders’ Medicare For All proposal. The highlights:

creates a “public option” in the first year

expands Medicare services to cover dental, vision, long-term care and all necessary medical procedures

eliminates co-pays and deductibles, making healthcare free at point of service

covers the cost of all prescribed medications

expands eligibility to cover all US residents over four years, creating a single-payer healthcare system

private insurance is prohibited from covering services covered by Medicare For All

eliminates all past-due medical debt

Medical service providers (hospitals, doctors, laboratories) continue to operate independently and bill Medicare for services.

If enacted, this proposal would make health insurance companies largely obsolete. Some rump services (elective surgery, health insurance for foreign travelers, etc.) would survive. Most health insurers would shrink to other insurance lines (P&C, life, liability etc.). Service providers that refuse to accept Medicare and its reimbursement rates would be left with a small pool of US patients who can afford to pay for medical services entirely out of pocket.

This is clearly negative for the health insurance industry. The proposal includes funding to retrain workers and help them find work, but there is no such provision for businesses. The US spends an outsized amount on healthcare, Senator Sanders claims his proposals would reduce this fraction while expanding coverage. This is only possible if the system reduces costs significantly.

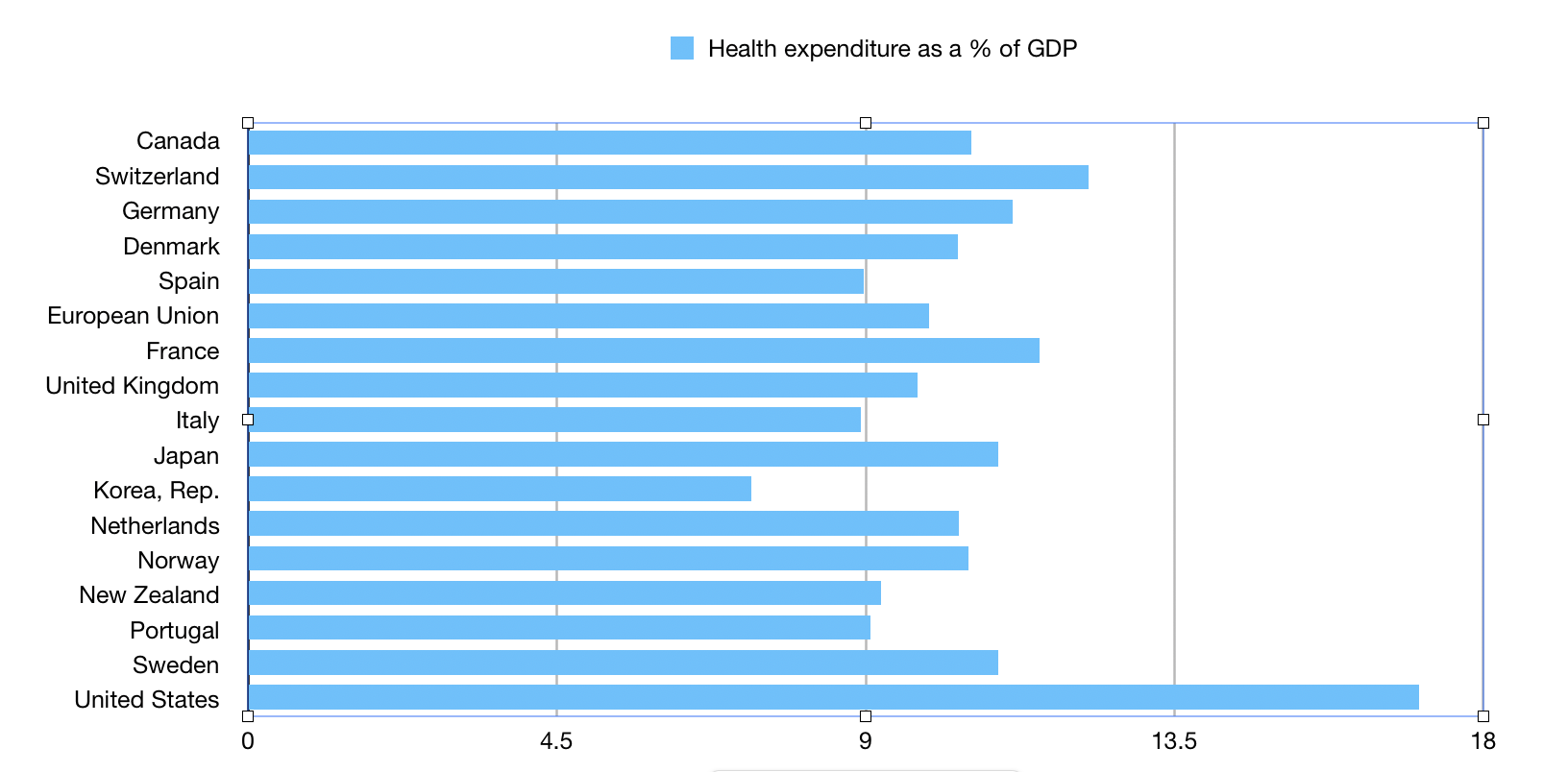

US healthcare expenditures are an outlier among OECD countries. World Bank data.

If a single-payer system is implemented in the US, it would almost certainly reduce costs. Some of this would come from lower overhead. Health insurance companies typically expend 20% of their revenues on costs other than reimbursement for medical services. In contrast, the current Medicare system operates at a much lower 3% overhead. Most observers also believe additional savings would be realized by delivering timely primary and preventative care to all, rather than expensive emergency care when maladies have become worse.

A detailed study published in The Lancet arrives at similar conclusions:

Taking into account both the costs of coverage expansion and the savings that would be achieved through the Medicare for All Act, we calculate that a single-payer, universal health-care system is likely to lead to a 13% savings in national health-care expenditure, equivalent to more than US$450 billion annually (based on the value of the US$ in 2017). The entire system could be funded with less financial outlay than is incurred by employers and households paying for health-care premiums combined with existing government allocations. This shift to single-payer health care would provide the greatest relief to lower-income households. Furthermore, we estimate that ensuring health-care access for all Americans would save more than 68,000 lives and 1.73 million life-years every year compared with the status quo.

Under Medicare for All, medical service providers would also face restructuring. Medicare’s reimbursement rates are generally lower than those offered by private plans. This may be partially offset by eliminating the complexity involved in billing thousands of health insurers and millions of individual patients. Since Medicare is a reliable payer, the effort and expense involved in managing unpaid bills would disappear for most health practices. These assumptions are validated by a survey of academic literature in the academic journal PLOS Medicine:

We found that 19 (86%) of the analyses predicted net savings (median net result was a savings of 3.46% of total costs) in the first year of program operation and 20 (91%) predicted savings over several years; anticipated growth rates would result in long-term net savings for all plans. The largest source of savings was simplified payment administration (median 8.8%), and the best predictors of net savings were the magnitude of utilization increase, and savings on administration and drug costs (R2 of 0.035, 0.43, and 0.62, respectively).

The benefits of Medicare for All would accrue to a broad cross-section of individuals and employers:

Health-care costs should begin to trend downward over time, from roughly 16% of GDP currently, to the 8-10% average across OECD countries.

Individuals would be guaranteed health-care free at the point of service. Our expectation is that this will quickly lead to better health outcomes across the US, eventually matching other developed countries.

US life expectancy should rise over time from the current 79 years to approach Canada’s 82 years.

US infant mortality rates should also fall from 6.5 per 1,000 live births to Canada’s 5.0.

By removing all cost-related barriers to health care, Medicare For All should result in increased use of preventative healthcare. This in turn should lead to a healthier work-force, increasing productivity.

Employers would no longer have to expend significant resources to evaluate, choose and maintain health insurance plans for employees.

Individuals would no longer have to expend time and effort on choosing plans and battling for reimbursement when they have medical expenses. By our estimate, this should result in a time savings of 2 days for every person in the US.

Almost 79 million US residents have medical debt. Academic research suggests such overhangs reduce economic activity and consumer spending. Medical debt also leads to hundreds of thousands of bankruptcies each year. Wiping out such debt should have a positive effect on growth.

Labor mobility should be improved by instituting universal healthcare that is free at point of service. The academic literature is quite clear that employer-linked health insurance reduces labor mobility and locks employees to jobs that may not be a desirable. COBRA does alleviate some of these concerns, but not entirely.

With such varied effects, it is difficult to estimate the overall short and medium term impact on US economic activity overall. From the experience of other industrialized economies, it seems clear that investments in public health improve long-term economic prospects. Taken together, these effects could add up to several points in additional GDP growth over 10 years.

We generally assume that the market reaction to a Sanders’ Medicare For All enactment will be negative to flat. Health markets in most jurisdictions do have some sort of price control and there is a case to be made for them in a market with the sort of information disparities and local monopolies that health care has. Yet many market participants instinctively recoil from price controls and our assumption is that the general market reaction to a single payer plan will be negative. Any longer-term impacts will take a while to materialize. Sanders’ proposals to raise capital gains rates, implement wealth taxes and a capital markets transaction tax are all more likely to affect market sentiment.

We will evaluate Senator Sanders’ College for All proposal in a later post, for now, we will note that home-ownership and head-of-household rates for adults in their 20s, 30s and 40s have been declining since 2007 and never recovered. That is a very strong indicator of lasting debt overhangs.

forgiving student debt would allow deeply indebted graduates an opportunity to embark on household formation without the burden of a debt overhang.

Each of these claims should be evaluated on its merits. We are skeptical of arguments relying on conventionally accepted political principles that dismiss this reasoning out of hand (eg. “it would never work”, “it is too costly”, “it’s insane”). There are several industrialized economies where higher education is free or very low-cost, these can serve as a model for analysis.

Market update: Measures to stall Coronavirus’ spread begin to impact global economic activity

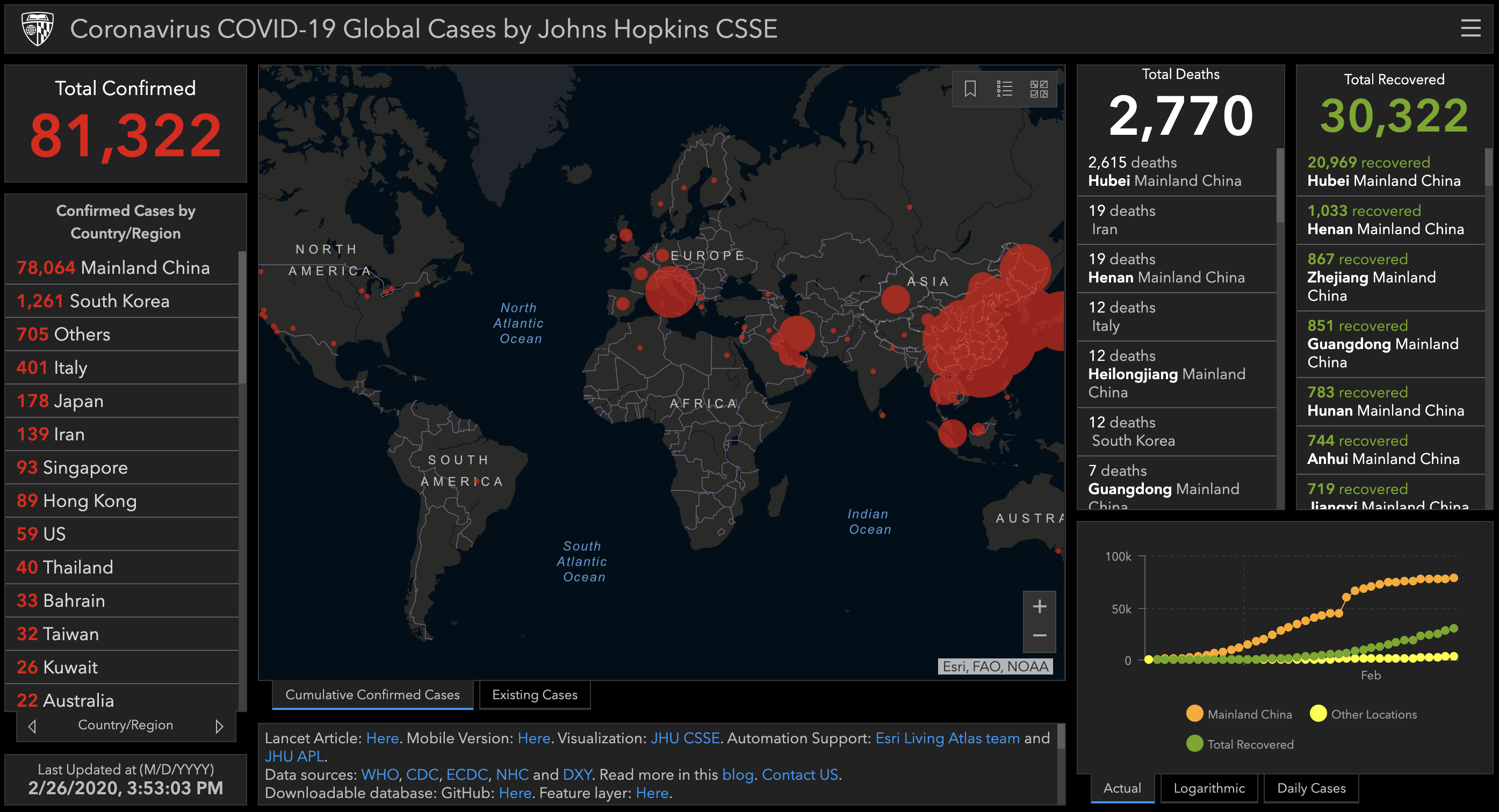

This week has seen two precipitous declines in US stock markets. The volatility has been attributed to fears of the Coronavirus strain named COVID-19. This infectious disease has now spread to several countries and caused over 2700 deaths. The reports of confirmed cases have almost certainly been under-counted as numerous developing countries with weaker health systems lack the resources to identify and respond to such outbreaks. To keep things in context, the annual flu causes more deaths in the US alone.

The market drop on Monday was driven by fears about the impact of COVID-19 on global trade. On Tuesday, federal officials warned that COVID-19 would almost certainly spread in the United States. They indicated that health professionals, hospitals, communities, businesses and schools should begin making preparations. This would include “social distancing measures,” like smaller groups in classes, canceling meetings or conferences and making arrangements to work from home. Dr. Nancy Messonnier, director of the National Center for Immunization and Respiratory Diseases, said in a news briefing that “it’s not so much of a question of if this will happen anymore but rather more of a question of exactly when this will happen.”

If the measures discussed by the CDC were to be implemented in the US, there would be a significant impact on economic activity and by extension corporate earnings. Millions of Americans can telecommute to work and it is reasonable to expect they could continue to work through such a potential crisis. However, a large segment of the US manufacturing and service sectors would be hobbled. This includes most entertainment, food service, travel, manufacturing and retail. It is difficult to estimate the precise impact on earnings, but the fact that we were recently at all-time highs and at the end of a maturing business cycle suggests any drop in expected earnings would have a significant impact on markets.

We are also concerned about the current administration’s preparedness for such a crisis. In 2018, part of the pandemic response infrastructure put in place after the Ebola outbreak was dismantled, without an adequate replacement put in place. This gap may lead to less than optimal coordination between federal agencies. The current crisis also reminds us of Michael Lewis’ 2018 book, The Fifth Risk. Lewis interviewed senior staff and ex-staff across numerous government agencies after the current administration took office amid reports of a haphazard transition with qualified personnel were leaving without being replaced. One of Lewis’ observations is that the Federal government is partly in the business of risk management. It evaluates and contains risks that are too big for any other US organization to handle. Funding cuts and the loss of experienced personnel severely undermines this mission.

Our healthcare system also has idiosyncratic vulnerabilities when dealing with such public health crises. Unlike other developed countries, most Americans face out of pocket expenses for healthcare. There are reports that individuals asking to be tested for COVID-19 received large medical bills. We know that the fear of unexpected bills often prevents people in the US from seeking timely care, necessitating expensive, late-stage interventions. The lack of timely diagnosis and treatment could exacerbate the spread of COVID-19 and have widespread public health impacts.

Even prior to the COVID-19 outbreak, we believed high equity valuations merited caution. Containment measures in China have already begun to impact the global economy, we expect the rising number of cases in Europe will have similar effects. If containment measures are required in the US, they are likely to have a significant impact on corporate earnings.

We reiterate our recommendation that investors maintain a defensive position in equities and other risk assets. We recommend caution as this situation continues to develop.

As Sen. Sanders and Warren’s portfolios show, divesting from fossil fuels isn’t easy

In the last debate between Democratic presidential candidates, moderators challenged billionaire Tom Steyer on his commitment to combating climate change. Steyer made his fortune in the hedge-fund industry by investing in fossil fuel businesses among other things. He said this was before he fully understood the challenge posed by climate change and has since divested of all such investments. By way of explanation, Steyer said his businesses invested widely in all sectors of the economy, including fossil fuels.

Not all investors are billionaires who can launch self-funded campaigns for the presidency, but the point Steyer made actually can apply to almost anyone who invests in public markets: divesting entirely from fossil fuel companies is rather challenging when you hold a diversified portfolio.

The demand for ethical investment choices is as old as the modern stock market itself. When shares in public companies first began to trade in the 18th century, Quaker endowments confronted the discomfiting fact that some of their investments might be profiting from the slave trade. This realization led to an early divestment campaign. Institutional investors like pension funds and endowments have long included ethical factors in their investment decisions. This has often been a response to prodding by activists and students, most famously during the campaign against apartheid in South Africa. Individual investors have generally not faced such pressure, though some of our clients with politically aware children would beg to differ.

We do not believe consumer or investor choices alone can deliver structural change. Yet where we invest is a window into how we think about the impact of our investments, or whether we’ve thought about it at all. As investment professionals focused on socially responsible investing, we speak daily with families who want their investments aligned with their values. Our clients have varying motivations for engaging us. Many are concerned about the environment, war, human rights, gun violence and worker’s rights. While seeking to avoid investing in companies that profit from destructive practices, we simultaneously seek investments in sustainable companies (a process called positive screening).

In recent years, millions of Americans have begun to examine their investment decisions with a moral/ethical lens. Few are as outspoken about economic morality, or have as large a platform as the leading candidates for the Democratic nomination. We decided to put the two progressive candidates (Bernie Sanders and Elizabeth Warren) to the test by evaluating their investment portfolios against their rhetoric.

Our analysis makes it clear that even well-informed investors with access to the best information have a tough time incorporating their values into their portfolios. For years now, Senator Warren has criticized the CEOs of both J.P. Morgan and Facebook. Yet, by our estimate, Senator Warren and her husband have approximately $50,000 invested in each company’s shares. This would almost certainly come as a surprise to Senator Warren, as it would to most Americans with conventional portfolios.

To calculate this number, we used self-reported, 2018 senate asset disclosure forms for Senators Bernie Sanders and Elizabeth Warren. Since candidates are only required to report broad ranges for the value of their investments, our analysis has to be limited to these ranges as well.

Both candidates hold substantial amount of cash, so let’s start there. Sanders has publicly chastised America’s largest banks with some regularity, and his banking relationships reflect that criticism. He banks with the Senate Federal Credit Union and two community banks. If you are concerned about the outsized power that very large banks wield, you would do well to follow his lead and switch to a credit union or community bank.

Senator Warren’s banking choices are rather inexplicable. She has been trenchant in her criticism of the largest American banks (notably, she had a very public spat with J.P. Morgan’s CEO Jaimie Dimon last month). Warren has publicly and legislatively supported community banks. In a banking proposal her campaign unveiled this summer, she envisions a partnership between community banks and the postal service to deliver low-cost banking services to underbanked communities. Despite several good community banking options in both Massachusetts and DC, Senator Warren seems to have chosen to patronize larger banks, including two behemoths, Capital One and Bank of America.

Senator Warren’s investment portfolio looks very much like that of a former educator. She holds a number of broad-based, low-cost index funds, many of them at TIAA-CREF, an investment firm that has had a long partnership with colleges and schools. These are cost-effective saving and investment vehicles. However, broad index funds incorporate virtually every industry in the economy including arms manufacturers, polluters and companies which have worked to undermine unionization efforts. These holdings are at odds with Warren’s political positions.

Throughout the campaign, Senator Warren has presented a robust climate change policy. Yet, over 4% of her stock portfolio is invested in the oil and gas industry, including approximately $40,000 in Exxon Mobil.

Bernie and Jane Sanders’ investment portfolio consists largely of mutual funds. In common with Sen. Warren and her husband, Jane Sanders has several investments with TIAA-CREF. This is an unremarkable coincidence given their work as educators.

The Sanders have begun to take the first steps towards ethical investing since their holdings include a socially responsible mutual fund. The couple appear to be familiar with how SRI fund managers push companies to adopt more responsible practices. By seeking out socially responsible investments, they demonstrate greater awareness than most Americans. Yet their portfolios still contain numerous investments they would doubtless find objectionable.

The moral or ethical questions surrounding business activities can get obscured when considering a small investment in a large multi-national corporation with dozens of operations in several countries. Mutual funds often contain hundreds of individual investments, creating an even greater challenge for investors who seek to implement a social responsibility mandate. Like most investors in mutual funds, the Sanders don’t appear to have fully investigated what their mutual funds are invested in. For example, Bernie Sanders has sparred with Bill Gates over taxes and the outsized influence billionaires have on US politics. Yet, the Sanders single biggest stock holding is Microsoft, entirely via mutual funds. Despite Senator Sanders best intentions, and even though they invest in a socially responsible fund, his investments do not seem to fully align with the Senators’ values.

Since many companies do not accurately report on social/ethical criteria, implementing a SRI mandate becomes an insurmountable challenge for most individual investors. Most investment professionals in the industry have no experience in socially responsible investing. Many will cavalierly dismiss ethical criteria by making unfounded claims that ethical portfolios negatively impact performance.

In fact, SRI helps reduce economic risk in a portfolio. Unsustainable and exploitative business practices create significant risk of fines and accrue unaccounted liabilities. The example of tobacco companies is instructive, and we would suggest that fossil fuel investors may soon face a similar situation as governments and communities across the world seek to recoup the costs of climate change from the most culpable and largest actors.

Broader adoption of ethical criteria by investors on its own is insufficient to reverse systematic trends like climate change, wars and runaway inequality. It does, however, have an impact. If, for example, we wish to see meaningful policy action on climate change, investors have to speak up, with both their voices and their dollars. Separating our investments from other spheres of our lives simply perpetuates the status quo.

What then should families who wish to incorporate ethical criteria into their investment process do? The first step would be to engage an investment professional with extensive experience in the area. Our firm has 15 years of experience advising families on how best to incorporate their values into their investments. When done with care and diligence, ethical investing can reduce both economic and idiosyncratic risk and help improve portfolio performance.

As we close the books on 2019, we wish you and your family the best for the upcoming year.

2019 was an unexpected year for investors. Despite pressures from trade wars and uncertain policy, stock markets bounced back from a rough close to 2018 and rose significantly (over 25% in the US). GDP growth is estimated at a respectable 1.9% for the year and unemployment fell. The blockbuster stock market performance was boosted by multiple rate cuts by the Federal Reserve and corporate tax cuts also juiced profits significantly. While the tax cuts have benefited stock market returns, they have further deteriorated US public finances and widened the wealth gap.

2020 is an election year, and we expect it to be a particularly interesting one, with sharp contrasts in policy and vision. One issue we would like to see more discussion of, is US national debt and how its proceeds are used. The budget deficit for fiscal year 2019-2020 is estimated to be $1.10 Trillion, a staggering level at any time, but inconceivably large for a non-recessionary year. As long-term, value investors we believe the debt is appropriate only when used to finance long-term capital investment. The recent tax cuts were advertised as an incentive to such investment, but this has not materialized. The Fed’s capital expenditures index actually dropped over the course of the year. The end result is that our rising national debt has created no long-term investments in human or physical capital which might pay off in decades to come. In our view, the next administration must seek to better allocate national resources, and meaningfully address the public and private debt load future generations are poised to inherit.

We have attached our review of our 2019 themes, we didn’t do as well as we’d like, with most of our projections being unrealized. Since 2020 is the start of a new decade, we have opted to take a longer view and have prepared our top ten themes for the coming decade.

We wish you and your families the very best for the 2020s!

To speak with us about your investments or financial plan, please call +1.646.450.9772 or e-mail us (info@wsqcapital.com).

Regards,

Subir Grewal, CFA, CFP Louis Berger

Economic Themes for the 2020s: 20/20 Vision May Not Be Perfect

Since 2020 marks the beginning of a new decade, we focus on themes we expect to play out over the next ten years.

Emerging Markets continue to take over the world. Population growth and younger demographics in emerging markets will continue to drive growth through the 20s, as the population in developed market economies continues to age. We expect emerging & developing market GDP growth to stay above 3% for the decade.

Autonomous Vehicles in our neighborhoods. A confluence of various technologies has made it possible for drones and self-driving cars to pilot themselves. The coming decade will see millions of autonomous vehicles take to our roads and skies. Our vision of the robotic future has been heavily influenced by sci-fi representations of humanoid robots. The reality is that the robots of our future are more likely to be a pizza delivery drone.

Genetic testing becomes commonplace. The cost of genetic testing has fallen dramatically over the past few years. By the end of the decade, we expect genetic testing and sequencing to be commonplace and most healthcare facilities in the developed world to offer full-genome sequencing to all patients. This powerful technology raises enormous ethical and moral questions which will make the road bumpy, but won’t materially slow the growth.

Blurring the line between reality and games. We expect the 2020s to be the decade where augmented reality, virtual reality and the line between games and real life will become blurred. These advanced functions will require ever more powerful graphics processing units (GPUs). We expect software and hardware companies in this space to grow especially as their products become more affordable to a wealthier, growing population in emerging markets.

Business opts for computing as a service. The biggest change in commercial computing over the past decade has been the rise of central, shared datacenters operated by the largest tech companies. We expect this trend to accelerate over the coming decade, with self-managed datacenters becoming increasingly rare.

Climate Change is here. The 2020s are shaping up to be the decade where climate change begins to impact large swaths of the population. We’ve already seen an increase in the incidence of extreme climate events (such as the enormous wildfires in Australia), a trend that has not gone unnoticed by the insurance industry. Over the course of this decade, we expect this conclusion to become almost universally accepted in the US. This will have an impact on the fortunes of the energy industry and many others. A number of our other long-term trends will focus on aspects of climate change.

Water, water everywhere / Nor any drop to drink. As rainfall patterns change and we experience hotter and drier weather for longer, obtaining potable water will become harder for much of the world’s population. We expect the market share of water-related technology and infrastructure companies to grow as communities across the world work to use fresh-water resources more efficiently by recycling, desalination and gains in efficiency.

Renewable Energy as the sole growth area. By 2030, we expect conventional power sources to begin sunsetting. Renewable power sources will account for over 150% of net new power capacity as conventional power generation facilities are mothballed (renewable capacity was 75% of net new power capacity growth in 2018).

A plant and lab future. We expect plant-based and lab-grown meat substitutes to displace significant amounts of meat consumption in the US and Europe by 2030. This will result in lower meat consumption across the developed world and slower growth in global meat consumption.

Tech enters banking in force. As the technology sector matures and ever larger companies look for areas of growth, we expect focus to shift to commercial and retail banking services. This is an industry already seeing significant disruption from advances in technology. Major technology companies have begun to dip into the waters with credit card and peer to peer payment offerings. By 2030, we expect over 15% of payment/banking services by value to be provided by companies that were not banks in 2020.

2019 Economic Themes: Return of the Bear – Reviewed

Bear Market Comes out of Hibernation. […] We contend this reversal gains steam this year as stocks globally will finish 2019 in firmly negative territory. […] – We were flat out wrong on this one. After being down 4.45% in 2018, total return on the S&P was an eye-watering 31.29% in calendar year 2019. The MSCI world index was up 24%.

Peak Interest Rates. […]At the start of 2019, the effective target rate stands at 2.25%-2.50%. While the Fed has signaled a continuation of rate hikes this year and into 2020, we think rates will peak in 2019 and the Fed will pause before potentially cutting rates if/when a recession materializes. […] – We were right on this. The Fed cut rates a bit earlier than we expected, but 2.5% marked the high point for short term rates in this cycle.

Unemployment Rises. 2018 saw the US unemployment rate reach a 49-year low of 3.7%. […] this expansion cycle looks due for a reversal and we expect the unemployment rate will climb back over 4% in 2019. […] – We were wrong here. Unemployment dropped slightly over the course of 2019, ending the year at 3.5%. A Brookings institution study released in November noted that 53 million workers in the US are making low wages, with median annual earnings of $17,950. Under such conditions, it is questionable whether unemployment is a good estimate of economic prosperity.

Investors Want Value. […] We believe value will outperform growth this year as economic expansion slows and investors shift investment capital into more defensive sectors. […] – We were right here, barely. While stocks rose indiscriminately in 2019, The S&P500 Value index was up 31.93% while the S&P500 Growth index saw gains of 31.13%.

The Unwinnable War. […]We see 2019 ending with some measure of tariffs still in place, continued global hostility towards the Trump administration and ongoing damage to the US reputation and economy. – We were right here. Despite numerous announcements of progress or deals, the trade dispute between the US and China remains unresolved.

Real Estate Reckoning. […] The S&P/Case-Shiller 20 City Composite Home Price index peaked in April 2006 and didn’t reach a bottom until March 2012. […] We think this streak comes to an end in 2019 and the index will finish the year lower. – We were wrong here, the Case-Shiller index remained largely flat. It stood at 212.66 in December 2018 and the latest data for Oct 2019 has it at 218.43, up 2.7%.

Oil Prices Flounder. […] we believe Brent Crude will dip below $50 per barrel and finish the year under that level as global trade slows and energy consumption slackens. – We were wrong here too. Brent closed the year at $66/barrel.

High Times for the Cannabis Industry. […] We expect 2019 will bring more legislation to expand the recreational market and more investments from multinational conglomerates (2018 saw Altria and Constellation Brands invest in the space). We expect publicly traded marijuana stocks will outperform consumer discretionary stocks in 2019. – We were partially right here. Legalization continues to gain steam, with NY state on track to legalize marijuana in 2020. Though there is no index for Marijuana related stocks, the largest ETF ended the year down significantly.

China Stumbles. […] we believe 2019 will continue to be a flat to negative market for Chinese equities. The Shanghai Composite remains around 2,500. This is less than half the 5,178 level reached in 2015, which was lower than its all time high of 5,800 in 2007. – We were wrong here, the Shanghai composite ended the year up at 3,050.

Battery Power. […] We expect EV sales to continue to grow in 2019, and global liquid fuels growth to be below 1.3%. – We were right on this one. Global electric vehicle sales were up 46% in the first half of 2019, then slowed due to expiring subsidies in China. EV sales for 2019 are expected to still be above 2018. Global liquid fuels consumption was 99.97 million barrels/day in 2018. For 2019, the figure is estimated at 100.72 million barrels/day, or under 1%.

We trust you’ve all had a pleasant summer. As we head

into autumn, the question on every investor’s mind seems to be when the longest

running bull market in US history will end. For several quarters, we’ve

advocated caution based on our view that equity valuations continue to be

unreasonably high. We have, however, always kept Keynes’ adage in mind, that

“The market can remain irrational longer than you can remain

solvent”. Keynes learned this valuable lesson through his own experience

trading currencies and investing on behalf of the King’s College endowment from

1921-1946. Many things have changed in the investment world since Keynes coined

that phrase, but economic cycles have not. And just as it was during

Keynes’ time, all bull markets eventually come to an end (sometimes abruptly)

and usually with a recession.

When assessing the health of the economy, there are

several indicators investors and economists monitor to gauge whether the

business cycle is approaching a recession. Let’s consider them one by one:

Consumer Confidence Index: This index published by The Conference Board measures economic optimism of US consumers via their spending/savings activities. The Consumer Confidence Index dropped 9 points to 125 in September, with both consumers and businesses indicating conditions were not as good as they were earlier in the year, however levels are still fairly high. The same organization publishes a “CEO Confidence index” which also dropped 9 points to the lowest level in our decade long expansion, suggesting the corporate C-suite is showing more trepidation than consumers at the moment.

Stock Prices: are considered a leading indicator of economic activity since valuations are based on future earnings. The S&P 500 reached an all time high in August (3007 points), we are now approx 4-5% below that high.

Purchasing Managers Index: The Institute for Supply Management publishes an aggregate measure of the US manufacturing sector. This index dropped to 47.8% in September (from 49.1%). Any reading below 50 signals a contraction. A key measure of exports dropped to the lowest level (41%) seen in a decade. The corresponding measure for the services sector (the NMI) stands at 52.6%.

Durable and manufactured goods orders: The US Census Bureau reported that durable goods orders increased by 0.2% in August, while shipments and inventories of durable goods rose marginally. New orders for manufactured goods dropped by 0.1% in August, shipments and inventories rose marginally.

Housing starts: The Census Bureau also reported that building permits rose 7.7% in August (seasonally adjusted). New residential construction is at the highest level it has been since 2007 (but well below the highs of 2005). Some of this can be attributed to falling interest rates lowering the cost of capital.

Weekly Hours: This measure estimates the number of paid hours worked by the hourly workforce. This indicator bottomed out at 33.7 hours in 2009, it reached a high of 34.6 hours in 2016. It is now close to that high, at 34.4.

Global Trade: The WTO measures trade in goods and services across the world. Its most recent report indicates global trade in both goods and services has weakened in all regions this year. The softness is largely driven by unresolved trade disputes. The Global PMI stands at 47.5, which is the lowest level since 2012.

Taken in aggregate, consumer confidence (the most

forward looking measure) and the PMI indicate some softness in the

economy. Global trade activity is weakening, which is also a negative

sign. Other indicators signal low to moderate growth. The services sector

appears to be growing, with exports and manufacturing showing no growth or mild

contraction.

Interest Rates are also considered a leading indicator of economic

activity. Lending for long periods of time carries greater risks than short

term lending, and investors generally demand higher rates to lend for longer

periods. When long term interest rates are higher than short-term rates, the

“yield/rate curve” is considered to be normal. When long-term

interest rates fall below short-term rates, it implies that bond investors

believe rates will be lower in the medium-long term (i.e. the Fed will lower

rates in response to a worsening economy). This is often called an

“inverted yield curve”.

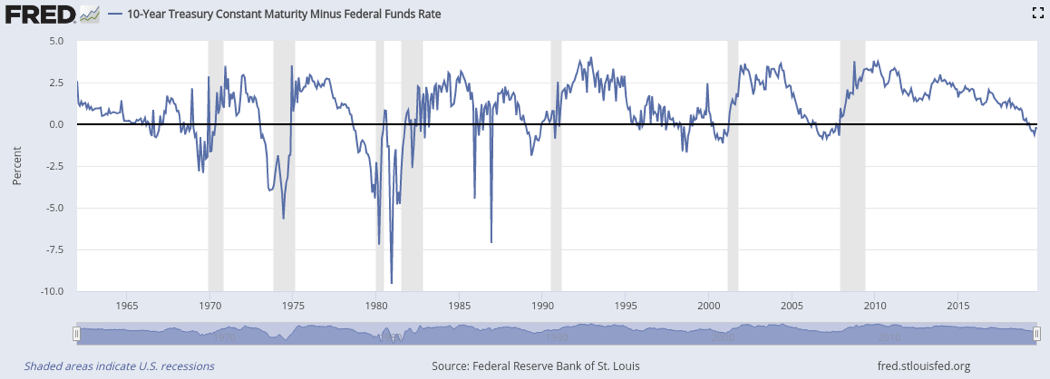

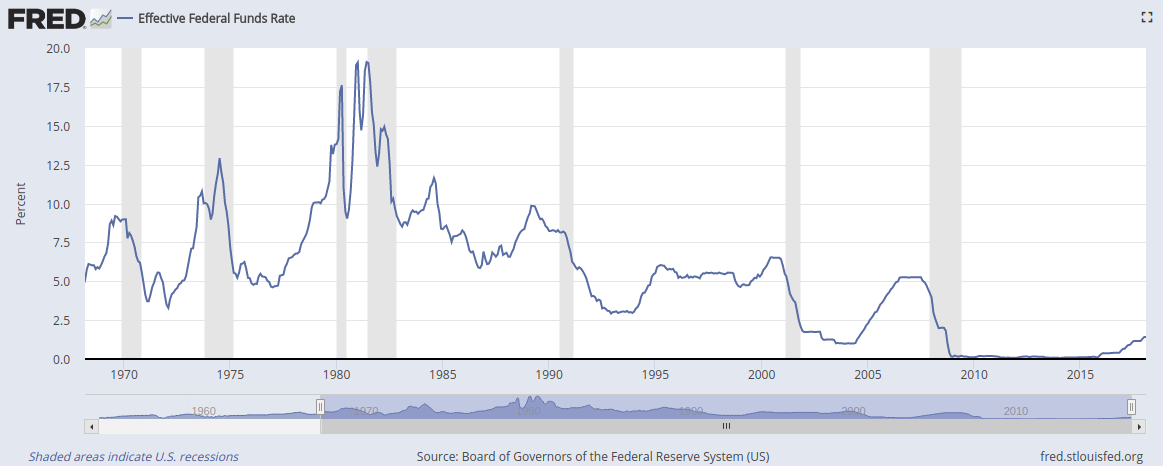

Many participants watch the “10 Yr – Fed Funds

spread” to gauge the shape of the curve. This measures the difference

between 10 Year interest rates and overnight Fed funds rates. When the

overnight (1 day) interest rate is above the 10 Year rate, the spread is

negative. The graph below shows a history of this rate spread. Every recession

since 1960 (see shaded columns) has been preceded by a negative spread,

i.e. an inverted yield curve.

Unemployment rates are the strongest

single indicator that a recession has begun. Unemployment claims tend to rise

almost exactly as the economy contracts. Businesses know it’s expensive

to hire and train staff, so managers often wait to reduce headcount until

they’re certain markets are shrinking. When large numbers of workers are laid

off, they change their consumption behavior, spending less. This change in

behavior can become “contagious” as neighbors and former colleagues

of the unemployed also retrench, reducing their own consumption in the face of

economic uncertainty. This feedback loop in turn deepens the recession.

Overall, we believe there are significant

risks of a recession ahead. If the unemployment rate rises, and the stock

market slides further, that should be seen as a confirmation that the economy

has begun contracting. We would then recommend very defensive positioning in

client portfolios.

Our current recommendation to investors

is to maintain caution and vigilance, rebalancing portfolios to be defensive

and be prepared to act if conditions deteriorate further.

The interest rate outlook has changed considerably since the

beginning of the year. Investors entered

2019 with an expectation the Fed was likely to continue raising rates

over the course of the year. However, recent comments from Fed officials have

made rate hikes far less likely. There seem to be three factors

influencing this sudden shift in Fed

policy. The first is gathering signs of a softening economic activity across

the world (the IMF estimates countries representing 70% of the global economy

will slowdown in 2019). The second is continuing uncertainty surrounding the

US’s trade policies. The last is the political pressure being placed on the

Fed, mainly expressed in the form of public statements and tweets from the

president as we head into a presidential election next year. Rate cuts at this

juncture would prolong the rally and the current economic expansion, aiding the

administration’s prospects in 2020. Though other administrations have tried to

coax the Fed, they’ve done so more quietly. We don’t know whether Fed officials

will find Trump’s more public approach tougher to ignore. The bond market itself

seems to be anticipating cuts, the yield curve is “inverted”, i.e.

near-term rates are lower than those further out. This has historically been an

accurate indicator of an upcoming recession.

As we begin the third quarter, the stock market remains close to

all time highs, with the S&P 500 hovering at just under 3000 points.

Despite some turbulence, stocks continue to be led by the technology sector,

which is now over 26% of the S&P 500’s market capitalization. That factor

has only been higher once, during the peak of the tech boom when it crested

over 30%. The Nasdaq, which contains a large number of technology companies, is

above 8000, an all-time high. However, there are some indications that the

technology rise has run its course. This year has seen a steady spate of large

technology IPOs for companies that have grown privately over the past ten

years. This includes: Lyft, Uber, Slack and Pinterest among others. Historically,

such a spate of stock sales has been an indication that professional tech

venture capital investors see the current price environment as a

high-watermark, and an ideal time to exit investments that have grown in value

for several years.

In general, the economy remains at very high levels of capacity

utilization. Unemployment remains at a multi-decade low and wages rose swiftly

in the past two quarters. The manufacturing and services sector remain at high

levels, but growth in new orders has slowed. The purchasing managers indices

for both manufacturing and services fell below 51 (a level of 50 indicates no

growth). Anecdotal reports suggest the weakness is at least partly due to trade

uncertainties. Consumer confidence also remains high, despite a sharp drop in

May.

Our general view remains that investors should exercise caution.

We continue to recommend a defensive allocation with greater exposure to high

quality bonds and lower exposure to risk assets.

Spring is in the air. Subir’s younger daughter won’t step

outside without checking to see what plants and trees have flowered. It is a

special joy to be reminded of the resilience of life and the cycle of the

seasons.

Back in the more quotidian world of markets, Q1 saw US equities

rally sharply, recovering from the lows seen in December. Stocks remain below

the highs of last summer. Part of this can be explained as a relief rally after

a tough Q4. Year-end consumer spending was not as bad as feared. The government

shutdown did eventually end and everyone apart from contractors was paid for

time lost. Of course, time is a non-renewable resource and several weeks of

human effort were lost.

A more influential factor spurring the rebound was the Federal

Reserve reversing policy in early January, telegraphing a pause in interest

rate hikes. The Fed appears to have been spooked by a confluence of factors

including: the shutdown, Brexit, the Q4 correction, deterioration in hiring,

and a softening of real-estate prices in several markets. Going into the

year-end, we’d expected two rate hikes in 2019. It is now far less likely that

this will happen. In our view, this weakens the Fed’s ability to act if we do

enter another recession.

There is some speculation that the Fed’s back-tracking was a

response to pressure from the White House. If that were the case, it would be a

cause for concern. It’s clear to all concerned that the president would like to

see an accommodating, low-interest rate policy heading into the 2020 election

cycle. In that respect, this White House is no different from any other

first-term administration. However, the nature of the President’s statements is

somewhat unprecedented. The Fed is largely independent of the government and

such attacks do present another test to our institutions. However, most market

participants have been ignoring rhetoric coming out of the White House. As long

as the Fed governors don’t let this affect policy, and chairman Powell can brush

off the president’s frequent bromides, the White House’s statements are likely

to have no impact on the market.

Looking beyond our shores, we still see an unsettled

environment. The United Kingdom continues to lurch towards a break with the EU,

without any firm plan in place. In our view, the UK’s exit from the EU system

will have a significant economic impact, but it is unlikely to be extreme. We

do not ascribe to the doomsday Brexit scenarios.

Further afield in Asia, we still see unsettled questions around

trade with China impacting real economic activity. Companies continue to shift

production out of China and into other South Asian countries. We believe these

trade spats portend a major shift away from the post-war order. For over 70

years, we have seen free, global trade as the reigning orthodoxy for relations

between nations. This is now being replaced by a more mercantilist stance in

both the EU and US. The US response to the rise of Huawei and other 5G Chinese

manufacturers underscores this. In Japan, the details of Charles Ghosn’s arrest

suggest that Japanese officials moved out of fear a top-3 Japanese automaker

would be absorbed into Renault.

If we are honest with ourselves, we will admit that various European

countries, and Japan have always had a mercantilist trade policy supporting

national champions. The US less so for most of the 20th century (outside of

energy policy). That is clearly no longer the case, at least under this

administration.

There are several reasons for this shift, the most significant

is the clear rise of China under a semi-managed system. The development of an

information-based services economy and the disruption of manufacturing

industries through outsourcing is also part of the explanation. These momentous

changes taken together have brought into question the 20th century orthodoxy of

free-trade in goods/services as the only route to prosperity. Many in developed

countries challenge these assumptions by pointing to declining living standards

among the general population. They can also point to examples like China, which

continues to keep much of its domestic economy closed and props up state-owned

national champions. All this creates a more unpredictable investment climate,

where we now have to consider the political links of major companies alongside

their purely commercial prospects.

From an investment perspective, we continue to advise investors

to maintain cautious allocations. Though markets have recovered from their

December lows, the past 15 months have seen increased volatility and we expect

that to continue going forward. As we enter the spring, we will remain watchful

for long-term opportunities that arise from any further correction.

We hope you’ve had a restful holiday season with family and a pleasant start to the New Year.

The fourth quarter of 2018 saw steep declines in US stocks, with certain indices entering bear markets (20% below their highs). Amid these moves, the Federal Reserve followed through on broadly held expectations and raised its benchmark Fed Funds rate to 2.5%. Taking a longer view, it’s clear the post 2000 era has been unusual. From 1962 to 2000, the Federal Reserve had never lowered rates below 2.5%. Since 2000, rates have remained below 2.5% for 15 of the last 18 years. Extremely low interest rates were made feasible by the near disappearance of inflationary pressure in the US. Prices for most manufactured goods have been kept low for over two decades as manufacturing was outsourced and large Asian populations were integrated into global industrial production. This multi-decade trend has allowed US and European central banks keep interest rates at historic lows without triggering inflation. Absent a dramatic reversal in global trade policy, we do believe this long-term trend will continue. In the near term, the Fed chairman has signaled two more interest rate hikes are expected in 2019 which would take the benchmark rate to 3%. We believe the Fed is more likely than not to follow through on these hikes, for two reasons:

1. Q4 saw unprecedented pressure from the White House on the Federal Reserve to avoid a rate hike. This included rumors that the president had sought to dismiss chairman Powell in an attempt to influence interest policy. The White House does not have the authority to dismiss the chairman except for cause, and we believe the Fed will be keen to demonstrate its independence by following through on its previously broadcast intentions.

2. Fed governors are well aware that recessionary risks are high in 2019. If the Fed Funds peaked at 3%, the Fed would have more room to respond to a downturn using rate cuts alone. We believe Fed governors would prefer to use interest rates to respond to the next recession, rather than a revival of the unprecedented Quantitative Easing (QE) program put in place in 2008.

Normalized rates, trade disputes, a faltering Chinese economy, and concerns about asset valuations in a long-running US bull market combined to deliver a very volatile stock market in December. Stepping back to get a wider perspective, we are nearly ten years into an exceptionally long bull market. Several risks to economic growth materialized over 2018. Central banks globally have pulled back from the exceptional liquidity programs adopted after the financial crisis. These factors combine to create a less forgiving investment environment and makes a so-called soft-landing less likely. In our view, the underlying risks to the US and global economy advocate for continued caution on the part of investors. As always, long-term opportunities will present themselves in choppy markets and we intend to capitalize on them when they do.

We have enclosed our 2019 investment themes as well as a review of our 2018 themes. We hope to have an opportunity to discuss them with you in the near future.

Regards,

Subir Grewal, CFA, CFP Louis Berger

2019 Economic Themes: Return of the Bear

Bear Market Comes out of Hibernation. 2018 saw a major speed bump in the nearly 10 year global bull market run in stocks. We contend this reversal gains steam this year as stocks globally will finish 2019 in firmly negative territory. Trade wars, rising interest rates, inflated asset valuations, and a general slowdown in economic activity will contribute to a “risk-off” environment where investors prefer protection over speculation.

Peak Interest Rates. In December of 2015, after seven years of 0% interest rate policy, the Federal Reserve shifted course and slowly began to raise interest rates in 0.25% increments. At the start of 2019, the effective target rate stands at 2.25%-2.50%. While the Fed has signaled a continuation of rate hikes this year and into 2020, we think rates will peak in 2019 and the Fed will pause before potentially cutting rates if/when a recession materializes. We do not think the Fed will raise past 3% in this year.

Unemployment Rises. 2018 saw the US unemployment rate reach a 49-year low of 3.7%. The US economy has come a long way since unemployment peaked at 10% in October 2009. That said, this expansion cycle looks due for a reversal and we expect the unemployment rate will climb back over 4% in 2019.

Investors Want Value. Since 2009, US growth stocks have outperformed US value stocks in seven of those ten years (including three of the last four). We believe value will outperform growth this year as economic expansion slows and investors shift investment capital into more defensive sectors.

The Unwinnable War. Despite rhetoric from president Trump that trade wars are “easy to win” and a March 1 deadline to resolve the US/China trade dispute, we see no quick and easy resolution to this fiasco. We see 2019 ending with some measure of tariffs still in place, continued global hostility towards the Trump administration and ongoing damage to the US reputation and economy.

Real Estate Reckoning. 2018 saw residential real estate prices finally eclipse the peak reached before the credit crisis. The S&P/Case-Shiller 20 City Composite Home Price index peaked in April 2006 and didn’t reach a bottom until March 2012. Since then, it has seen a nearly 7 year uninterrupted run-up of higher prices. We think this streak comes to an end in 2019 and the index will finish the year lower.

Oil Prices Flounder. After peaking at $86.07 on 10/4/18, Brent Crude oil prices tanked in Q4, finishing the year at $51.49 per barrel. While there may be a short term bounce in prices to start the year, we believe Brent Crude will dip below $50 per barrel and finish the year under that level as global trade slows and energy consumption slackens.

High Times for the Cannabis Industry. In recent years, marijuana has made a steady push into the mainstream as several US states and a few countries have passed legislation to legalize recreational consumption. A nascent industry has emerged to service this growing demand. Many of these companies are small, regional operators, but recently, larger and better-financed corporations have entered the space with many becoming publicly traded entities. While the road has been rocky and the sector has seen large price swings, we think this is an industry poised for long term growth. We expect 2019 will bring more legislation to expand the recreational market and more investments from multinational conglomerates (2018 saw Altria and Constellation Brands invest in the space). We expect publicly traded marijuana stocks will outperform consumer discretionary stocks in 2019.

China Stumbles. Over the course of 2018, we saw several worrying signs that the Chinese economy is slowing. Property prices, which have propped up all other assets for years have slowed, and there are numerous reports that several non-bank lenders have halted redemptions. The trade war with the US has also been a major drag on the economy. 2018 was a terrible year for Chinese stocks — the S&P China Composite index returned -27.82% — and while some investors expect a bounce-back year, we believe 2019 will continue to be a flat to negative market for Chinese equities. The Shanghai Composite remains around 2,500. This is less than half the 5,178 level reached in 2015, which was lower than its all time high of 5,800 in 2007.

Battery Power. A long-term trend we are highlighting in our thinking for 2019 is the growth of plug-in electric vehicles. Roughly 2 million four wheel electric vehicles were sold in 2018. US sales of EVs represented over 1% of total vehicle sales. In California, the largest passenger vehicle market, EV were 4% of all vehicles sold spurred by tax incentives and emissions targets. When we include plug-in hybrid electric vehicles, EV sales account for over 7% of all vehicle sales in California. These figures portend a long-term shift in the transportation industry, of the same degree as driverless cars. 10 years from now, we expect 25% of the world’s vehicle fleet to be battery powered. Over the long-term, this implies a very difficult environment for the oil and gas industry. We expect EV sales to continue to grow in 2019, and global liquid fuels growth to be below 1.3%.

2018 was an uneven year for our market predictions. We were right on six calls and wrong on four calls. While we were right about the general market direction, a few of our sector specific calls were off the mark.

Slow But Steady Rate Rise: We expect the Fed to maintain the normalization plan and continue tightening rates in 2018 with the Fed Funds rate ending the year in the 2%-2.5% range. The Fed started 2018 with a target interest rate of 1.25%-1.50%, raised rates four times by 0.25% to finish the year with a target rate of 2.25%-2.50%. This was precisely in the range we expected.

Year of the Donkey: We expect the mid-year election of 2018 to mark a sharp reversal for Republicans, who currently control all three branches of federal government. The 2018 midterm elections resulted in a sharp rebuke to the Republican agenda. Democrats won the House popular vote by a whopping 8.6% and had a net gain of 40 House seats, taking back control of the House of Representatives. They also had a net gain of seven governorships and six state legislative chambers.

The Bull Runs Out of Steam: We expect 2018 to be a difficult year for equities markets given the extremely high levels attained over the past two years. After a fast start in January, 2018 turned into a down year globally for stocks. In the US, large caps fared best as the S&P 500 index finished the year at -4.38%. Mid caps were hit harder as the S&P MidCap 400 index returned -11.08%. Small Cap value stocks brought up the rear in the US as the S&P 600 Value index returned -12.64%. International stocks lagged the US as the FTSE All World (Ex-US) index returned -14.13%.

Rise of the Machines: As we did in 2017, we expect AI/Automation stocks to outperform consumer discretionary stocks. While we strongly believe Artificial Intelligence and Automation companies will be integral to the global economy in years to come, 2018 saw stocks in this sector hit a speed bump as investors sold off more speculative technology names. The Global Robotics and Automation index finished the year at -20.92% while the S&P Global Consumer Discretionary index returned -6.24%.

International Beats Domestic: We expect international stocks, especially European markets, to outperform the US in 2018. We were flat out wrong on this call. International stocks fared worse than US stocks in 2018, with European stocks performing particularly poorly. The S&P 500 index posted a return of -4.38%, the FTSE All World (Ex-US) index returned -14.13% while the MSCI EMU index returned -16.90%.

Bitcoin Bust: Bitcoin prices themselves are in a speculative bubble which we expect will reset in 2018. Bitcoin’s meteroic rise in 2017 saw a sharp reversal in 2018 as speculators fled en masse. Bitcoin opened 2018 at $13,444.88 per coin, but finished the year at $3,880.15 per coin, a drop of 73.70%.

Renewables Redux: 2017 saw renewable energy YieldCos outperform conventional fossil-fuel based electric utilities. We expect this trend to continue through 2018. While we strongly believe in the long term prospects of renewable power, YieldCo stocks trailed conventional utilities for a variety of reasons: energy prices fell (because of higher up-front costs, YieldCos tend to be more attractive when energy prices are high) and a flight to safety from investors (conventional utilities are a popular safe haven in times of market volatility). The INDXX Global YieldCo index finished the year -4.98% while the S&P Global 1200 Utilities Sector index was up 1.69%.

Organics Go Mainstream: We think organic food stocks will outperform conventional food stocks this year. 2018 was a tough year for packaged food stocks across the board. That said, organic companies performed notably worse than conventional food companies. The MSCI World Food Products index returned -12.99% while the Solactive Organic Food index returned -26.61%.

New Dawn of Space Race: 2018 will see a number of commercial space ventures mark milestones, including manned-flight into low-earth orbit and potentially a lunar orbital space tourism mission. 2018 saw several space related milestones. The highest profile was a successful test launch for SpaceX’s Falcon Heavy rocket, which placed a car in a helio-centric orbit that takes it past Mars. Virgin Galactic completed testing a craft designed for sub-orbital space tourism flights. The most interesting project is the Japanese Hayabusa2 mission. Hayabusa2 successfully rendezvoused with the asteroid Ryugu and placed multiple rovers on the surface. The spacecraft will return a sample from the asteroid to Earth. This mission provides a viable template for future space based mining endeavors. These technological advances will take a decade or more to reach industrial scale, but once they do we believe they will significantly alter the nature of the mining industry.

Net Neutrality Fallout: Telecommunications firms have risen in the past month as a result of this ruling, but we believe the medium and longer term prognosis is less rosy, with the prospect of new entrants and even more consumer dissatisfaction. 2018 did see a backlash against the major telecom companies and the net neutrality ruling certainly didn’t help to reverse the cord-cutting trend. Telecoms underperformed the broader market in 2018 as the S&P 500 Telecom Services Index returned -7.20% while the S&P 500 index returned -4.38%.

As we approach the end of an eventful 2018, there continues to be a steady torrent of major news stories dropping daily. From CEOs tweeting about taking their companies private, to escalating global trade wars, to bitter battles on Capitol Hill, the financial markets have had a lot to digest. Though the news can seem overwhelming at times, we believe investors should remain focused on the issues that matter for their investment portfolios: valuations, interest rates, economic conditions, and global trade. Each of these factors are at levels that indicate a richly valued stock market in the final stages of a historically long expansion with potential for major risk ahead. Let’s walk through each of them one-by-one.

Interest Rates. As expected, the Federal Reserve raised interest rates in the third quarter and the Fed Funds rate now stands at 2.25%. The 10 Yr Treasury rate is almost at 3.25%, which is the highest it’s been since 2010. It’s likely the Fed will raise rates again by 0.25% in December and continue to raise rates at a similar pace (quarterly) in 2019. While rates remain on the lower end historically, rising rates will continue to take a chunk out of corporate profits as companies raising funds for projects in the debt markets are now paying higher rates than they have in years. The tax cut passed by Congress last year has provided a bit of a tailwind for corporate profits, but this boon will likely be offset by the costs associated with higher interest rates, especially for sectors that depend on high levels of debt.

Global Trade. Despite a major change in trade policy (tariffs), trade levels remain high. That said, there are several looming disputes (US-China, US-Europe) that may cause continued dislocation. We are beginning to see American companies modify their supply chains in response to tariffs. Though, in the long run, this will lead to the growth of manufacturing in new markets and new sources for intermediate and finished goods, in the shorter run this is likely to lead to some dislocation. History shows us that tariffs are almost always a net negative on economic output (as open trade is closed off) and we see no reason why the current tariff war will result in anything other than economic slowdown. If the results of the “new NAFTA” is any indication, the tariff wars will not bring increased economic prosperity to the US, but rather, hurt industries dependent on foreign trade while damaging relations with our trade partners/allies and eroding their trust.

Valuations. Stock valuations remain at cyclical highs. The S&P 500 is trading at 25 times historical earnings, which is about 50% higher than the historic average. When we look at cyclically adjusted measures of earnings, these are at even higher levels. Yale professor Robert Shiller’s Cyclically Adjusted PE ratio (which uses the past ten years of earnings as a denominator to account for the business cycle) is currently over 33. The only other time it has been higher than 30 was in 1929, on the eve of the great depression, and in 1999-2001 during the tech boom. This measure has been above 30 for most of 2017 and 2018. Can this continue? It certainly can, but if we use history as a guide, economic expansion can end quickly, rendering current valuations as especially lofty in hindsight.

Economic Conditions. Despite the concerns mentioned above, economic conditions in the US continue to be quite strong, with consumer confidence levels high and the unemployment rate low. Inflation is relatively tame and average hourly wages are finally rising. However, debt levels — corporate, government and consumer — are all at precariously high levels. If interest rates rise, trade wars persist and valuations remain elevated, we could see these conditions deteriorate.

In addition to these factors, there is a potential major market-moving event on the horizon: the mid-term elections on November 6th. Mid-term elections tend to be a referendum on the White House and ruling party in Congress. Given the president’s low approval ratings, we believe Democrats are likely to re-take the House. We think they have an outside chance at winning back the Senate. This is far less likely because there are fewer Republican seats up for election, and because small, low-population inland states get as many senators as large coastal ones. We think a House controlled by Democrats will lead to meaningful investigations of political corruption in the Trump administration. All indicators suggest this is a target-rich environment for such investigations. If the White House decides to work with Democrats, as they indicated they might in 2017, we could see a curtailment of tariffs and a wide-ranging infrastructure bill. Given the highly partisan political environment, however, compromise seems less likely and gridlock the norm.

How will markets respond? It’s difficult to predict, but if we see a Democrat controlled house, the Congressional agenda of the past two years (deregulation, protectionist trade policy, tax breaks and loosening of environmental regulations) will likely end. Investors in sectors like conventional energy and materials/mining will see this as a negative. Sectors like renewable energy and industries dependent on trade, like technology, are likely to view it as a positive development.

We continue to recommend balanced investment portfolios and a reduction of exposure to risk assets that may be vulnerable in a market correction.

Regards,

Subir Grewal, CFA, CFP Louis Berger

Keeping an eye on what matters for the economy, Trade.

Over the past year and a half, trying to absorb news has felt a bit like drinking water from a fire hose. Like many of you, we have steadily become more concerned and simultaneously more accustomed to the chaos being created by the current US administration. While the actions of our government have deviated from the values of the American people in the past, this disconnect is especially evident today. The government’s high disapproval ratings reinforce the fact that its actions represent a minority of American society. A large majority of Americans are not beguiled by the administration’s base appeals to fear.

Amid all the animosity directed at weaker members of our society, the administration has also undertaken ill-considered actions on trade that we believe will impact investors.

In many industrial fields, US protections for workers and the environment outpace those in developing parts of the world. This, coupled with our relative wealth, creates a situation where set-up costs tend to be higher in the US than they are in less wealthy nations. The international trade norms which have been adopted by much of the world over the past several decades acknowledge this fact. They establish basic labor and environmental protection standards which most nations adhere to. The expectation is that as industries in other countries mature, they face natural pressures to improve labor and environment practices. We can see this dynamic in effect in China, India and much of the developing world as a more assertive labor force organizes itself and citizens demand safer, cleaner, healthier environments. Previous US administrations have largely stuck with this bargain and helped cement it. This administration’s response is markedly different. It has worked relentlessly to demolish protections for workers and the environment, engaging in a race to the bottom. Such an effort will have a long-term impact on our human and ecological capital.

US workers, citizens and enterprises have legitimate concerns about our trade policies. Much of what our country exports is ethereal: movies, software, music, designs and technology are simple to reproduce if the original source is available. American technology companies fend off numerous attempts each day to steal valuable designs or content. Some of these attempts are successful. In several cases, the perpetrators and beneficiaries of such thefts are politically connected businesses.

Prior administrations have worked to slow down and deter such anti-competitive trade practices, opting for targeted action that sought to limit the impact on other industries. The current administration has repeatedly shown a penchant for using a sledgehammer when a scalpel is more appropriate, and this matter is no different. It has embarked on a series of wide-ranging punitive tariffs on a range of goods, from a number of different countries, including China and close allies like the EU and Canada. These countries have begun to respond, slapping tariffs on American exports.

As the cycle of tit-for-tat increases in import duties gathers steam, markets have begun to wobble. Global trade and supply chains rely on orders placed months ahead of time. For the system to function, some degree of price stability has to exist. When prices, or in this case, duties are changing rapidly, traders are apt to overcompensate, not knowing whether the worst of the increases are baked in. An increase in duties can force companies to modify supply chains, moving production to different areas in an effort to avoid tariffs. Newer centers of production take time to ramp up and build expertise. When enough of this happens, supplies become constrained, prices rise, and quality suffers. None of these are good outcomes for enterprise or consumers.

As the administration’s trade war intensifies, driven by a president whose instinct is to always double down, we are not complacent about the risks.

A decline in trade levels will impact a wide swath of American industry, which is deeply interwoven into a global network of production. When trade levels fall, we will see this ripple through corporate expectations and outlook, eventually reducing valuations, earnings and prices.

Based on this outlook, we recommend investors maintain caution and adopt defensive positions. Reducing risk assets and holding a portion of portfolios in low risk securities such as short-term government bonds, fixed deposits or cash remains our priority.

Regards,

Subir Grewal, CFA, CFP Louis Berger

2018 Q1 letter: Why the roller-coaster market is back.

As we noted in our 2017 year-end review, we expect 2018 to be a tough year for the domestic stock market. Rising interest rates and valuation concerns are going to be the major story for investors this year. Stock market valuations remain elevated, with the S&P 500 currently priced at 24 times last year’s earnings. This is far higher than the post-war average of 17 times earnings.

The primary justification for high P/E ratios is the extremely low interest rate environment we’ve experienced in this century. For much of the 80s and 90s, interest rates remained above 5% (see chart below). In contrast, since April 2001, US interest rates have kept well below 5%, apart from 13 months spread between 2006-07.

This unusually low interest-rate environment has support stock prices throughout the 21st century. Low interest rates spur higher stock prices for a variety of reasons:

Income oriented investors are driven to the stock market since bonds and bank deposits offer very little return.

Future corporate earnings are valued more highly since the discount rate is lower.

Consumers and companies take advantage of low interest rates to finance projects and purchases cheaply. This spurs sales.

Leverage becomes cheap for speculators, amplifying the amount of money invested the market.

When rates begin to rise, all these supportive factors are reversed, acting as a head-wind for stocks. The Fed has signaled that it intends to continue raising interest rates since unemployment is low and the overall health of the economy remains strong. In our view, rate hikes are the crucial factor driving the recent stock market drops, and we believe this volatility will continue.

There’s no denying the market has been more volatile since January. Over the past three years, the S&P 500 has seen 20 days when it was down more than 2%. Seven of those days have occurred in 2018 (and we’re only in early April). As of this writing, the S&P 500 is now 10% below the peak reached on January 26th. Technology stocks, which had seemed relatively immune to the downturn have also begun to sell-off. Over the long-term, we continue to believe technology will become a larger part of consumer’s lives and our economy. However, just as with every industry, business models can change and seemingly unassailable companies can falter. The current, sky-high valuations for many technology companies leave little room for error.