Review of 2018 Investment Themes

2018 was an uneven year for our market predictions. We were right on six calls and wrong on four calls. While we were right about the general market direction, a few of our sector specific calls were off the mark.

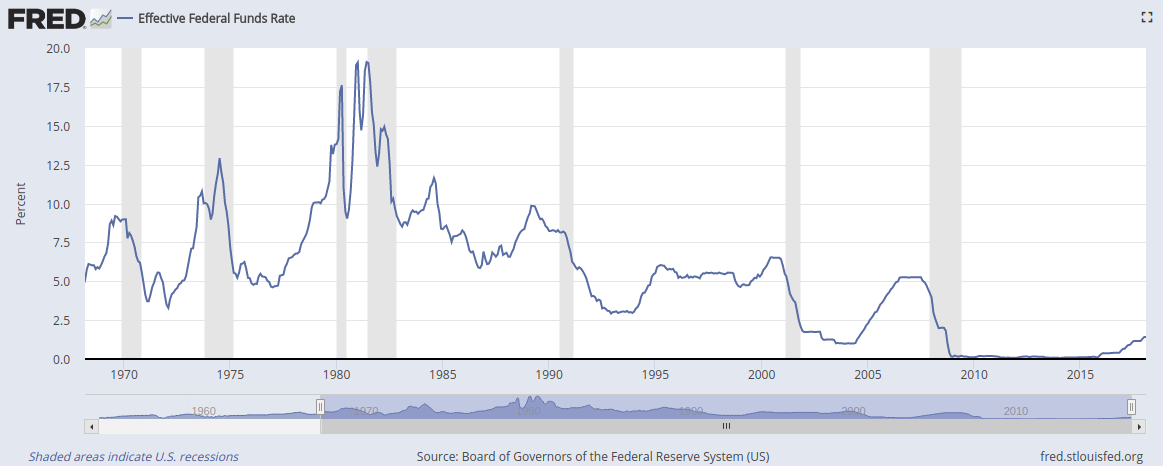

- Slow But Steady Rate Rise: We expect the Fed to maintain the normalization plan and continue tightening rates in 2018 with the Fed Funds rate ending the year in the 2%-2.5% range. The Fed started 2018 with a target interest rate of 1.25%-1.50%, raised rates four times by 0.25% to finish the year with a target rate of 2.25%-2.50%. This was precisely in the range we expected.

- Year of the Donkey: We expect the mid-year election of 2018 to mark a sharp reversal for Republicans, who currently control all three branches of federal government. The 2018 midterm elections resulted in a sharp rebuke to the Republican agenda. Democrats won the House popular vote by a whopping 8.6% and had a net gain of 40 House seats, taking back control of the House of Representatives. They also had a net gain of seven governorships and six state legislative chambers.

- The Bull Runs Out of Steam: We expect 2018 to be a difficult year for equities markets given the extremely high levels attained over the past two years. After a fast start in January, 2018 turned into a down year globally for stocks. In the US, large caps fared best as the S&P 500 index finished the year at -4.38%. Mid caps were hit harder as the S&P MidCap 400 index returned -11.08%. Small Cap value stocks brought up the rear in the US as the S&P 600 Value index returned -12.64%. International stocks lagged the US as the FTSE All World (Ex-US) index returned -14.13%.

- Rise of the Machines: As we did in 2017, we expect AI/Automation stocks to outperform consumer discretionary stocks. While we strongly believe Artificial Intelligence and Automation companies will be integral to the global economy in years to come, 2018 saw stocks in this sector hit a speed bump as investors sold off more speculative technology names. The Global Robotics and Automation index finished the year at -20.92% while the S&P Global Consumer Discretionary index returned -6.24%.

- International Beats Domestic: We expect international stocks, especially European markets, to outperform the US in 2018. We were flat out wrong on this call. International stocks fared worse than US stocks in 2018, with European stocks performing particularly poorly. The S&P 500 index posted a return of -4.38%, the FTSE All World (Ex-US) index returned -14.13% while the MSCI EMU index returned -16.90%.

- Bitcoin Bust: Bitcoin prices themselves are in a speculative bubble which we expect will reset in 2018. Bitcoin’s meteroic rise in 2017 saw a sharp reversal in 2018 as speculators fled en masse. Bitcoin opened 2018 at $13,444.88 per coin, but finished the year at $3,880.15 per coin, a drop of 73.70%.

- Renewables Redux: 2017 saw renewable energy YieldCos outperform conventional fossil-fuel based electric utilities. We expect this trend to continue through 2018. While we strongly believe in the long term prospects of renewable power, YieldCo stocks trailed conventional utilities for a variety of reasons: energy prices fell (because of higher up-front costs, YieldCos tend to be more attractive when energy prices are high) and a flight to safety from investors (conventional utilities are a popular safe haven in times of market volatility). The INDXX Global YieldCo index finished the year -4.98% while the S&P Global 1200 Utilities Sector index was up 1.69%.

- Organics Go Mainstream: We think organic food stocks will outperform conventional food stocks this year. 2018 was a tough year for packaged food stocks across the board. That said, organic companies performed notably worse than conventional food companies. The MSCI World Food Products index returned -12.99% while the Solactive Organic Food index returned -26.61%.

- New Dawn of Space Race: 2018 will see a number of commercial space ventures mark milestones, including manned-flight into low-earth orbit and potentially a lunar orbital space tourism mission. 2018 saw several space related milestones. The highest profile was a successful test launch for SpaceX’s Falcon Heavy rocket, which placed a car in a helio-centric orbit that takes it past Mars. Virgin Galactic completed testing a craft designed for sub-orbital space tourism flights. The most interesting project is the Japanese Hayabusa2 mission. Hayabusa2 successfully rendezvoused with the asteroid Ryugu and placed multiple rovers on the surface. The spacecraft will return a sample from the asteroid to Earth. This mission provides a viable template for future space based mining endeavors. These technological advances will take a decade or more to reach industrial scale, but once they do we believe they will significantly alter the nature of the mining industry.

- Net Neutrality Fallout: Telecommunications firms have risen in the past month as a result of this ruling, but we believe the medium and longer term prognosis is less rosy, with the prospect of new entrants and even more consumer dissatisfaction. 2018 did see a backlash against the major telecom companies and the net neutrality ruling certainly didn’t help to reverse the cord-cutting trend. Telecoms underperformed the broader market in 2018 as the S&P 500 Telecom Services Index returned -7.20% while the S&P 500 index returned -4.38%.

Dear Friends,

Dear Friends,