We hope you’re having a good start to the summer. This has been an eventful quarter.

On May 22, Kevin Warsh was confirmed as Fed chair, succeeding Jerome Powell who will finish the remaining two years of his term as a Fed governor, retaining a vote on interest rate policy. Powell survived extraordinary political pressure, including a DOJ investigation, which many believed was without merit and an effort by the Trump administration to force a more compliant monetary regime. The DOJ’s attempts to prosecute Chair Powell and the administration’s attempt to dismiss Fed Governor Cook for cause were both unsuccessful. Both cases were based on flimsy pretexts and driven by personal animus. The transition of power to Chair Warsh stabilizes the institution, which has seen its independence and stature challenged in profound ways during the second Trump administration.

Chair Warsh’s first statements have signalled continuity, sprinkled with some changes. It has been made clear that communication from the Chair will be markedly different in the Warsh era. Chair Warsh has indicated he prefers concise official statements and a return to the rather opaque Federal Reserve communications of the Greenspan era. Thus far, the bond market has taken this in stride, relieved that the immediate threats to Fed independence appear to have faded.

The equity markets have remained in bull market territory over this quarter, with occasional volatility. The story of the quarter has been anticipation of three blockbuster AI related IPOs over the remainder of this year. The first has already occurred. SpaceX’s IPO valued the company over $1.5 Trillion and its current market price places its valuation at over $2 Trillion. This is remarkable for a company that has not yet turned a profit, and has annual revenue under $20 billion. The bulk of SpaceX’s current revenues come from satellite-related communication services and rocket launches. OpenAI and Anthropic are expected to offer shares to the public in the coming months and each is expected to debut at a $1 trillion+ valuation. Perhaps in anticipation of these offerings, we have seen some rotation in technology stocks with several of the larger Tech companies seeing some investors reallocate capital.

As the USA enters the 250th anniversary of the country’s founding, the nation is embroiled in a war in the Middle East . Strangely, you could have said this for most of the past 40 years, and you would not have been wrong. The war in Iran appears to be qualitatively different from past wars the US has engaged in within the region. In the past, the superiority of American arms was abundantly clear. In the new world of drones and relative parity among missile defense systems, this is no longer the case. For markets, the most critical question, yet to be answered, is when the supply chain disruptions in the Persian Gulf will be over. Though there have been small reprieves, the Strait of Hormuz is still largely closed to commercial shipping that is not affiliated with Iran.

The disruption of oil supplies has had a limited effect on prices thus far, but this is entirely due to large scale releases from the strategic petroleum reserves of the US and other countries. These reserves are finite and the US’ Strategic Petroleum Reserve is now at its lowest level in over 40 years. The daily withdrawals from the reserve are north of a million barrels per day. At this rate, the ability to withdraw from the reserve will be severely limited in a few months. If that were to happen, we can expect oil prices to rise and inflationary pressure to drive prices for many goods and services up.

This is where the impact of the Federal Reserve will be felt most keenly. The new Fed chair will have one vote among twelve to set interest rate policy for the US Central Bank. Though most business media discussion focuses on the Consumer Price Index, the Fed evaluates a slightly different measure, PCE (Personal Consumption Expenditure). PCE year over year stands at 4.1%, as of May 2026. This is broadly in line with CPI figures, which are 4.2% annualized for May 2026. Much of the inflationary effect is due to fuel prices, which have seen a 20% rise, much of it ascribed to the war with Iran. The average consumer has seen electricity prices rise almost 6% over the past year, some of this is due to increased consumption by datacenters related to AI.

Bond markets now expect one, perhaps two rate hikes later this year, which would put the Treasury’s short-term interest rates at over 4% and long-term rates over 5%. At those levels, we can expect the dual impacts of investor rotation and debt servicing to apply downward pressure on prices and earnings in the equity markets respectively. In prior equity bull market cycles, it was interest rate rises that led to bear markets. In prior cycles, technology stocks would have been considered largely immune to interest rates since so few carried significant debt loads. The AI investment cycle has seen many tech firms raise tens of billions via debt. Though this has been raised at fixed yields, it makes many major technology companies look like more traditional industries where the cost of debt service impacts earnings.

Equity market valuations remain historically extreme. Trailing 12 month P/E is over 32, which is twice the long term mean of 16. Cyclically adjusted P/E is over 41, which is also twice the long-term mean of 17. The ‘Buffett Ratio’, Stocks as a percentage of GDP, is over 200 for the US, higher than it has ever been Valuations can remain above average for extended periods of time, that is what it means to be in a bull market. Such elevated valuations indicate that future returns for equity investors are likely to be muted unless growth too exceeds past history. The market currently seems to believe that will be the case, largely due to the advances made in Generative AI. However, we’re reminded of the dot com bubble when technology investors were also confident the emerging internet economy would transform the economy and usher in a golden age for technology stocks. While the economy was indeed transformed, during that cycle, the Nasdaq reached its peak in March of 2000 and didn’t eclipse that high water mark until April of 2015. Historically speaking, the highest levels of stock market volatility have come in the months of September/October.

We continue to recommend balanced allocations, with a bias towards caution with regards to equity portfolios. If technology stocks correct from their current loft highs, we expect to see investors diversify into defensive sectors, which look relatively undervalued. With the prospect of inflation coupled with rising bond yields, we recommend shorter than normal duration in bond portfolios, exposure to floating rate and inflation protected bonds as well as commodities.

If you would like to discuss any of these comments, please reach out to us via email.

This is a much longer letter than usual, its length is due to momentous changes that have occurred in the past three months.

This is a solemn spring, millions of people have been displaced and thousands have been killed in yet another war in West Asia. In our view, this war was initiated in a bout of hubris. Some in the White House and Congress appear to have believed they could assassinate the Iranian head of state and bring a more pliant government to power in Iran. In the first days of the war, the administration claimed this as a war of liberation for the Iranian people. The plan for a quick “regime change” appears to have been immediately dashed since many potential moderate politicians were killed in the initial surprise bombings. Four weeks later, US officials threaten to destroy Iran’s power plants, electricity, and entire infrastructure, returning it to the “stone age.” We doubt this is the sort of liberation even the most ardent internal critic of the Iranian administration would wish for. We are also increasingly unsure of the US’ objectives in this war and how it will end. One frequent refrain from our administration is that the Strait of Hormuz must be re-opened for the war to end. The Strait was, of course, open to all navigation prior to the US/Israeli bombing campaign that began on February 28. Iran maintains that the Strait has remained open to vessels not associated with the belligerents and it has begun to charge transit fees. It is unclear as to what rules will govern during the recently announced ceasefire, and in the long-term.

This is an investment newsletter, and at the risk of seeming callous, we shall set aside our own views on this war and the humanitarian considerations, as we attempt to understand what it portends for markets and the economy. The White House appears to have underestimated the capabilities of the Iranian armed forces and government, or ignored the advice of those who cautioned them that the Iranians are a formidable adversary. Several prior administrations chose not to embark on a war with Iran based on this counsel. We believe this war will have significant medium and long-term impact on the global economy, some of which has already occurred.

Immediately after the US/Israeli attacks on February 28, Iran’s government announced the Strait of Hormuz would be closed to traffic. Over 20% of the world’s supply of oil and gas, fertilizers and other industrial products such as helium, pass through a narrow channel that lies within Iranian territorial waters. The deepest channel, used by the largest ships, is close to the Iranian coastline.

We believe Iran can keep the Strait of Hormuz closed to commercial traffic for months, if not years if it wished to. A vast ground army would be required to destroy coastal fortifications and open the Strait by force. It is worth recalling that the US reached an agreement with the Ansar Allah (aka Houthi) government in Yemen, after failing to forcibly open the Bar el-Mandeb Strait on the Red Sea. Ansar Allah possessed a fraction of Iran’s capabilities.

The Iranian government has allowed some ships to transit the Strait, subject to a transit fee. Notably, they have required the fee to be paid in Chinese Yuan. Historically, the Middle-Eastern economies have benchmarked oil sales against the dollar and this led to most other regional transactions being dollar-denominated. The Iranians are shut out of the dollar economy by sanctions, and they seem to be deliberately taking aim at the dollar’s primacy in the region (often called the petro-dollar economy). The Iranians have said the passage fees will serve as restitution for the damage done by sanctions, and the current US/Israeli bombing campaign. In this effort, they have tacit support from China and Russia. Russia has required European buyers for its gas and oil to pay in Chinese Yuan as well. Over the past 20 years, successive US administrations have imposed economic sanctions on a broad range of actors. A shift to Chinese Yuan for transfer payments would would neuter such sanctions.

The Iranians have also responded to attacks on their industrial facilities by targeting US allies in the region whose territory was used for attacks on Iran. The UAE, Qatar, Kuwait, Bahrain and Saudi Arabia have sustained damage to military bases and industrial facilities. In some cases, these oil and gas facilities will not be restored to full capacity for many years. The closing of the Strait, and damage to industrial plants has begun to impact the supply of numerous petro-chemicals. Even if the cease-fire announced today were to hold, the impact of the war would be felt for months.

The Iranians do not believe the US administration can be trusted in negotiations, having twice been attacked by US forces during negotiations. These breaches of trust will make reaching a long-term agreement difficult, and it is entirely possible that naval traffic in the region remains affected for many months. Iranian officials have indicated that they are prepared to continue the war beyond the US mid-term elections.

As oil and gas prices rise (and supply contracts), economies in Asia (particularly developing countries) have begun to be impacted. Some countries have moved to a four day work week, and gas shortages have shuttered industrial activity. Iran has increased its exports of oil and gas, finding new buyers for its hydrocarbons, which has bolstered its finances. The same is true for Russia. Meanwhile, the exact opposite is true for US allies in the region. Most of the Gulf Cooperation Council (GCC) countries have seen revenues from oil/gas sales drop precipitously. The GCC countries run large public deficits which are funded by their state owned oil companies. As oil revenues dry up, they will face enormous economic pressures. These countries have historically invested their sovereign wealth funds in the US and Europe, we expect they will be forced to make sales as this war drags on.

Since transportation costs account for a fraction of all goods prices, the rise in oil prices will impact broader inflation. We are beginning to see early signs of this in smaller oil-importing countries in Asia. As gas prices rise in the US, we expect food and other goods prices to rise as well. This will lower discretionary income and US consumer spending over time. The supply chain impacts are much broader than oil or gas alone. For example, helium is critical to semi-conductor manufacturing. One-third of the world’s supply of helium comes from Qatar and is currently off-line. It’s reasonable to assume a shortage of advanced chips over the next few months. Production of other crucial goods is similarly impacted, this includes fertilizers that are widely used across the world.

Iran’s strategy is one of attrition and economic warfare. As the subject of sanctions for decades, Iran understands how economic stress can affect a country’s capabilities. Iranian military planners have a sophisticated understanding of US domestic politics, and know the impact an economic crisis will have on the US’s resolve. Similarly, they understand the politics of GCC countries in their immediate neighborhood. Large segments of the GCC populations see this war as an act of aggression initiated by the US and Israel. Sympathies for the US and Israel were already low after the heavy costs of wars in Gaza, Lebanon and Syria. Pockets of support for US/Israel do remain, primarily among the Jordanian, UAE and Saudi monarchies. Each of these governments are absolute monarchies with no tolerance for dissent. Broad public opinion does pose a threat, even to them, and there is a chance we see these monarchies backed into a corner by their populations.

This war has already lasted longer than the optimistic estimates first presented by president Trump. The US administration is clearly looking for an off-ramp, but the Iranians have very few incentives to provide one. The US and Israeli attacks on civilian infrastructure have shored up internal support for the Iranian government. Given their geography, current strengths, and past history, the Iranians are unlikely to lay down their arms unless they extract significant concessions.

We believe the unprompted US attack on Iran was ill-advised. Though ignorance is no excuse in such serious matters, we believe a large segment of the US elite do not understand Iran, and are uninterested in learning about it. We are reminded of an anecdote where another US president, Jimmy Carter, expressed frustrations with Iranian intransigence and, in his view, an inordinate focus on the past. An American analyst in an attempt to explain the Iranian perspective remarked “Mr President, the old souq in Iran is 6000 years old, and what they call the NEW souq, is 2000 years old.”

In our estimation, this war will end only when the Iranian government is ready to have it end. At that point, it is probable that the US’s GCC allies and Israel will have been significantly weakened. After seeing the rapid retreat of US forces under Iranian missile barrages, it is entirely possible the GCC will no longer be willing to host US military bases. Iran is also likely to continue charging fees for passage through the Strait of Hormuz. If the war resumes, GCC investments in the US may need to be liquidated to help fund public sector deficits. Qatar, Saudi Arabia and the UAE invest with many large private equity and venture capital companies in the US. As the inflow of capital from the GCC slows, it will eventually affect asset prices. We are beginning to see some stress in the debt of very highly levered companies (almost all of them funded by private equity). This could easily spill over and impact other markets.

We must note that this war has already caused unimaginable losses. The initial surprise bombings conducted by the US killed over a hundred schoolchildren and seventy-five adults in a series of strikes on a school in Minab, Iran. There have been reports that the target may have been selected via AI tools, which raises another set of very troubling moral and legal questions. This was only one of many bombings that have killed civilians. We believe this and other actions taken to initiate this war have hardened the resolve of the Iranian government. It has emboldened those who insist the only way to provide security for Iranians is to impose so heavy a cost on the US and its allies that they do not think of striking at Iran again. This is part of the reason we believe the war will not have a quick and easy resolution, unless the US capitulates to Iranian demands.

Moving to the other high impact story of the quarter, over the past few months, we’ve been evaluating the new AI models released by Anthropic and OpenAI. These releases have sparked a reassessment of the investment landscape in our minds as well as that of other investors. To illustrate the significance, we will review the impact on three industries that we know well. These are technology and software services, financial services and genetic testing. All three of these are information industries in the sense that the highest value services they have historically provided involve interpreting and acting on information as opposed to manipulating physical materials. They are, from the perspective of economics, knowledge industries.

AI models and tools are furthest along in terms of software development. We can reliably say that a development or debugging task that might have taken two weeks with a prior generation of AI has now shrunk to a couple of days. High performance, specialized software using highly customized or obscure tools, remains largely unaffected. But, for the majority of software and software services, this leap in ability has taken place. The result is that the “competitive moats” many software companies were assumed to have built with large code-bases and rich feature sets have shrunk or dried up. A competitor could leapfrog an incumbent at a much faster pace than previously considered possible.

In financial services, our own development and startup experimentation has led us to the conclusion that the majority of work being done within financial services by client-facing personnel and/or researchers could be radically re-organized with this class of AI tools.

In the field of genetic testing, which we know from past association, we can see many novel applications. Physicians or genetic counselors have thus far been responsible for analyzing genome sequencing results for a particular patient. This task can now be performed by AI more efficiently. We would point specifically to Anthropic’s test results for Claude Op.4.6 which indicate the model is equivalent to human analysis 65% of the time. Similar tests have been developed for the other industries. Some of these results should be taken with a cautionary note since the tests are developed internally, and in some cases their methodology is not publicly available. All indications we’ve seen suggest that the direction of travel and approximate accuracy of the models for these tasks is roughly correct.

The shift in capabilities is so dramatic that dystopian scenarios are possible as we noted in our June 2025 letter. Many, but not all, players in the space are responsible actors. There are major AI labs that are playing fast and loose with safety. 10 weeks ago the Grok LP/xAI tool (created by Elon Musk-owned X – formerly Twitter) allowed users to generate dangerous material for many hours before it was shut down. The possibility that a loosely controlled AI may allow humans to develop a bio weapon or other doomsday scenario is not outside the realm of possibility.

What does all this mean for investors? AI is an enormously disruptive change that will percolate through the economy for the next 5 to 10 years and perhaps even longer than that. There are true outlier scenarios, for example, emerging capabilities in industrial robots and AI may give us autonomous robots that can perform a variety of different tasks at very low cost. This would be akin to going from horse-drawn carriages to a modern electric vehicle in the span of five years.

In the short term, the capital investment cycle in AI will continue. We are skeptical as to the returns from the investment and physical plan. We believe AI cloud compute capacity will be rapidly commoditized. We believe it likely that the greater part of economic benefits will accrue to firms that are effective at adopting and delivering an innovative set of products using AI technologies.

In the short term, the market is a beauty contest. In the long run, it is a measurement contest. In the immediate short term, we expect market participants to identify a series of industries that will face radical disruption from new entrance and AI companies. These industries will see increased volatility just as SaaS and software services have over the past months. In contrast, defensive sectors such as consumer staples which cannot be impacted in the same way should see investor interest increase. The same is true for certain natural resource sectors.

Over the medium term, it will become clear which new entrants have capitalized on these new capabilities to build disruptive companies. We will also see some existing enterprises adopt AI effectively and capture a larger market.

We must caution all investors that the next few years are going to be a period of immense change. This includes regulatory and social/political change as societies adapt and respond to these rapidly evolving transformative technologies.

Regards,

Louis Berger

Subir Grewal, CFA

PS: We have included a military briefing below, with the caveat that this is not our area of expertise, we are largely relying on sources we consider reputable.

Appendix: Military Briefing and Analysis

Iran is an ancient, diverse and sophisticated culture. The topography and geographical position of Iran have made it a major power for many millennia. The Iranian plateau is ringed by rugged mountain ranges that contain many peaks over 15,000 feet high. It is also vast, covering an area larger than France, Germany and Spain combined.The country has coastlines along the Persian gulf, and the Caspian sea. In a literal sense, Iran has high walls and moats protecting it. These natural defenses have long made it resistant to most foreign invaders. The Achaemenid, Parthian, Sasanian and Safavid dynasties each ruled for hundreds of years. Iranian cultural and scientific institutions have played an important role in human development over millennia. We are aware of the old quip, that war is a very expensive way to teach Americans geography.

In more recent times, the Islamic Republic of Iran has invested heavily in public education and healthcare. Literacy rates are over 90%, with virtually all children receiving a formal education. Women make up roughly 60% of university students. 40% of Iranian graduates earn a STEM degree (this is twice the US rate). 45% of the student population has some form of university education, only slightly below those in the US (55%).

US-imposed sanctions have forced Iranian industry to develop domestic alternatives for many goods. Iran has advanced industrial capabilities, producing over a million cars a year, and more steel per capita than the US. These industrial capabilities have allowed it to develop a domestic arms industry, with a particular focus on drones, missiles and small, nimble boats.

Military planners on both sides have assessed each other’s weapons’ strengths and weaknesses over the years. The Iranian military has been preparing for an asymmetric war with the US for at least three decades. For its part, the US has been war-gaming a conflict with an adversary like Iran since the Millennium Challenge 2002. That exercise demonstrated that US forces would face significant challenges and losses when confronting a capable adversary using asymmetric warfare techniques. Though US and Israeli warplanes have successfully hit many targets in Iran, it is clear that Iran’s capability to deploy drones and missiles remains intact. By launching varying barrages of older missiles early in the war, the Iranian armed forces have depleted a large portion of the US and allied missile interceptor stock. Missile interceptors are expensive to produce, and the near-term supply is finite. The Iranian armed forces have also successfully destroyed many of the US’ advanced radars, which has degraded the ability to provide timely warnings. It has also forced the US to redeploy advanced radars from bases in South Korea, reducing the effectiveness of those allies’ defenses.

Iran has also struck arms manufacturing facilities and datacenters across the middle east. It is our assessment that Iranian missile and drone stocks have not been materially depleted. Iran has built fortified missile production lines which lie deep beneath mountain ranges. It continues to launch medium and long-range missiles several times a day from multiple locations. Its naval assets include small fast craft capable of launching missiles, as well as various marine drones and mines situated in fortified installations along its coast.

The Iranian armed forces have partially succeeded in pushing the US back to airbases away from the Persian Gulf. These remote airbases, in Saudi Arabia and Israel have also been subjected to missile and drone attacks, with several aircraft reported destroyed. A US aircraft carrier, the USS Gerald Ford was damaged in a fire, there are suspicions that the damage was caused by Iranian missiles or drones. It is now in the dock being repaired. A second carrier has been forced to retreat to 1000km from the Iranian coast for the past few weeks.

The loss of several aircraft over the past week belies the US administration’s claims that Iranian air-defenses have been destroyed. Military analysts have suggested that Iran may have preserved its mobile air defenses and missile launchers in the initial weeks by placing them in hardened bunkers. Some videos released by the US military as evidence of successful strikes, may have been hits on inflatable or painted decoys, which have been widely used in the Ukraine war as well. More significantly, the US’s stock of long-range missiles is limited. For the first few weeks, US aircraft were firing guided missiles from outside Iran’s airspace. In the past two weeks, the US and Israeli air-forces have switched to flights over Iranian airspace to drop gravity bombs. This makes the aircraft vulnerable to Iran’s surviving air-defenses, and may explain the recent losses of F-15s and F-35s.

We share these military details to support our argument that the Iranian armed forces are a formidable adversary for the US. The decentralized structure of the Iranian government and armed forces was built to survive the sort of “decapitation strike” the US and Israeli air forces attempted on the morning of February 28. It is also worth noting that US officials have consistently downplayed the extent of their own losses, ascribing many of them to accidents. This includes the losses over the weekend of two C-130s and several helicopters, blamed on mishaps during a rescue operation. Military analysts believe they were lost to Iranian fire during a failed attempt by a large US and Israeli special forces team to locate and steal Iran’s highly-enriched uranium stockpile. The accidents and “friendly-fire” incidents have begun to pile up, and it strains credulity to believe that none of these incidents are the result of Iranian actions.

The Iranian armed forces have publicly said they are prepared for a long war. They believe the ceasefire agreed to last year after the 12 day war was a mistake, and the last 10 months were used by the US and Israel to re-arm, conduct deceptive negotiations and strike Iran again. Iranian officials have repeatedly made public statements that they will not permit this cycle to repeat itself.

Iranian officials have shown that they will employ the economic weapons at their disposal in this war. We believe the Iranian government possesses both the resolve and the capability to prosecute such asymmetric, economic warfare for an extended period. They have prepared for a long regional war over the course of several decades, and all indications are that they believe they are in it now. The US and its allies have sanctioned Iran for decades. The Iranian government now sees the tables as having turned, and an opportunity to deliver some of the same medicine to the US and its allies. Iran is largely self-sufficient, and has transport lines to its allies (Russia and China) via the Caspian Sea and rail networks to the north). The Russian and Chinese administrations, which have also been the subject of US led sanctions and tariff warfare, are unlikely to find American appeals to intercede persuasive. The US has also, broadly speaking, alienated allies in Europe and the GCC with its actions over the past years. Iranian military and political analysts are well aware of the fissures that exist in US alliances, and will be ready to exploit them.

We wish you the very best for the new year ahead. Here at Washington Square Capital Management, we are marking our 18th year of providing independent financial advisory, retirement planning and investment management services to our clients and their families.

As we enter 2026, we find the investment landscape mostly unchanged from where we were in the latter half of 2026. Economic and fiscal risks remain elevated, but markets appear to be largely unperturbed. Since the turbulent weeks after the initial tariff announcements of last spring, markets have largely ignored news from DC. The implicit assumption seems to be that the Trump administration will back off from, or water down, policies if the market and businesses do not like them. This seems to hold true for both invasions of foreign countries and prosecutions of senior Federal Reserve officials.

Meanwhile, it is increasingly difficult to wave off the state of American public finances. The US continues to run 1.5 trillion dollar budget deficits per year, levels that were not seen previously except for deep recessions in 2009. Spending has risen from 20-21% of GDP pre COVID to 23% over the past 3 years. Revenue has fluctuated, but is trending a couple of points lower (16-18%) than it was in the early 2000s (18-20%).

If we do enter a recession, we can expect deficits above $3Tn, levels seen only in the Covid year. US Federal debt levels have grown from 55% of GDP in 2001, to over 120% today. This puts the US in the top two large economies by this measure, behind only Japan, where government debt stands at 235% of GDP. Japan has been able to sustain these levels by virtue of having very low interest rates. It differs from the US by having undergone a sustained deflationary period and a larger domestic bond investor base that has shied away from equities since the Japanese equity bubble burst in the 80s.

If rates on US debt average 4%, interest costs alone would stand at 5% of GDP. That would amount to 30% of the US Federal tax revenue. A business enterprise with interest expenses averaging 3/10ths of its revenue would be considered very poorly run. However, as the Japanese example shows, governments that issue most of their debt in their own fiat currency tend to have a lot more room to maneuver. The interest burden represents a transfer of tax revenue from households composed of workers to households composed largely of those with excess savings (or foreign investors). This is not a stable social arrangement unless there is real growth in incomes, something that the median American household has not seen for decades.

On the inflation front, official data shows CPI steady under 3%, after two years of 5-8% readings post COVID. The deflationary impact of mass production in Asian factories continues to help keep inflation in check, despite the impact of US tariffs. The scale and depth of the deflation was brought home to us in a recent story about the largest Sturgeon caviar farm, which happens to be in China. China has become the largest producer of caviar from Sturgeon, employing modern aquaculture techniques to produce a product that competes with other Central Asian countries that have a long history of producing this luxury product. Farms have been built on lakes and waterways along the Russian border, and in Zhejiang. A large majority of Michelin starred restaurants now source Caviar from these fisheries. The end result has been to ameliorate prices as demand for this luxury has increased, a microcosm of what we have seen in the prices of many other goods. Prices for branded luxury goods have seen a great degree of inflation over the past five years, but that appears largely to be the result of price management by large fashion houses, extracting rents from a status-chasing upper class. If this dynamic continues, we do not see inflation being a major factor in Federal Reserve decisions. The Fed appears to have many other things being pushed on its plate by the current administration.

US equity market indices remain close to all time highs, driven largely by technology stocks associated with the AI infrastructure buildout. The largest AI related stocks remained at their highs. This is despite concerns that the vast amounts being spent on fast depreciating hardware may not be justified by revenue or earnings for decades, if ever.

Prior technology cycles, even those vindicated by later advances (railroads, telegraphs, early Internet), have seen early over-investment end in tears. We do not know exactly how this technology investment cycle ends, but thus far, the immediate uses have been limited. The bill for infrastructure investments will likely come due well before the returns begin to justify the carrying costs for these outsized investments.

Geo-political events continue to be a risk factor with many foreign policy observers reading a broader change in the renewed US interest in Latin America. Since the fall of the Soviet Union in the late 80s, the US has enjoyed unrivaled influence on the global stage. The misadventures in Afghanistan and Iraq, combined with the rapid, steady rise of Chinese military and economic power has challenged this position.. One outcome would be a balance of powers arrangement, with various regional hegemons exercising control in their immediate vicinity. Another outcome would be two or more global powers competing across the world for political and economic influence, as was the case at the height of the Soviet Union. Constituencies for both strategies exist within the US, and in China. Less powerful states such as India, Russia, Brazil and the EU block would be courted by either side.

The economic risks in such a transitional period stem from the actions of the major political actors. One actor may disrupt trade in an attempt to gain an advantage. In many readings, that is what the US has been doing with its regime of sanctions, tariffs and other constraints on trade and the flow of payments. A second form of disruption would be open conflict between the great powers and their allies or proxies. We have also seen brief flashes of this in the Middle-East, Latin America, Africa and even Eurasia. There is a chance that these conflagrations subside and we step away into a new, largely peaceful arrangement. But substantial risks remain.

We continue to advise investors with a long-term outlook to maintain a balanced portfolio, weighted towards assets that can withstand sudden risk shocks.

The investment cycle in AI capacity continues to be the main story in equities markets. Though other parts of the US economy appear to be slowing, the hundreds of billions of dollars being invested in data center capacity and GPUs is driving the market higher. The stock market has rewarded any corporate announcement of spending on AI. To us, this has begun to resemble the heady days of the tech cycle at the turn of the millennium. When any and every company that made a “.com” announcement was applauded with an immediate bump in its stock price.

Something similar is happening today. As with the 2000 tech bubble, we have also seen a number of “circular transactions” in this cycle. A GPU manufacturer “invests” in a customer and the customer buys a few tens of billions in GPUs. The market cap of both companies rises by a multiple of the additional “revenue”. A database company makes an announcement with an eye-catching headline figure about a customer that has outsourced a datacenter build (and the capex) to it. The database company becomes one of the most valuable companies in the world.

Such transactions blur the lines between revenue and investment and bring into question the assumption that most sales happen at arm’s-length. If hardware manufacturers and AI service companies are joint ventures, how should “sales” between them be valued? Thus far, the market has brushed off any concerns about these questions.

Meanwhile, real business applications for generative AI have remained limited. Classic internet search is quickly being replaced by generative AI search, but this is more of a like for like replacement rather than a truly new feature. Internet marketers have glommed on to conversational AI, which is clogging our voicemails and e-mails. Meanwhile, internet shoppers are using AI to search for better deals. Researchers are using generative AI to accelerate research projects. Middle school students are using AI to accelerate their homework. In the longer term, we see many productive real-world applications such as embedded, specialized models operating robotic equipment, machinery and vehicles.

In the early days of the internet overbuilding of capacity led to a boom followed by a bust in networking companies and early internet retail companies. The promise wasn’t realized till a decade or more later, after smart phones became ubiquitous and many fortunes had been destroyed. A veteran tech investor reminded readers that some of the largest tech companies almost went bankrupt during the tech wreck due to out of control spending.

Dystopian uses for our current generation of crude AI have kept pace with positive ones. We have seen increased reports of generative AI used for fraudulent activity. This includes the generation of fraudulent documents and voice as well. We urge all clients to be watchful for such attempts. We have also seen reports of people developing para-social relationships with chatbots. This is true for all age groups. Large corporations have indicated a desire to market “virtual friends” to lonely consumers. In the past week a digital studio has released a portfolio of reels for an AI actress. We find these potential uses troublesome.

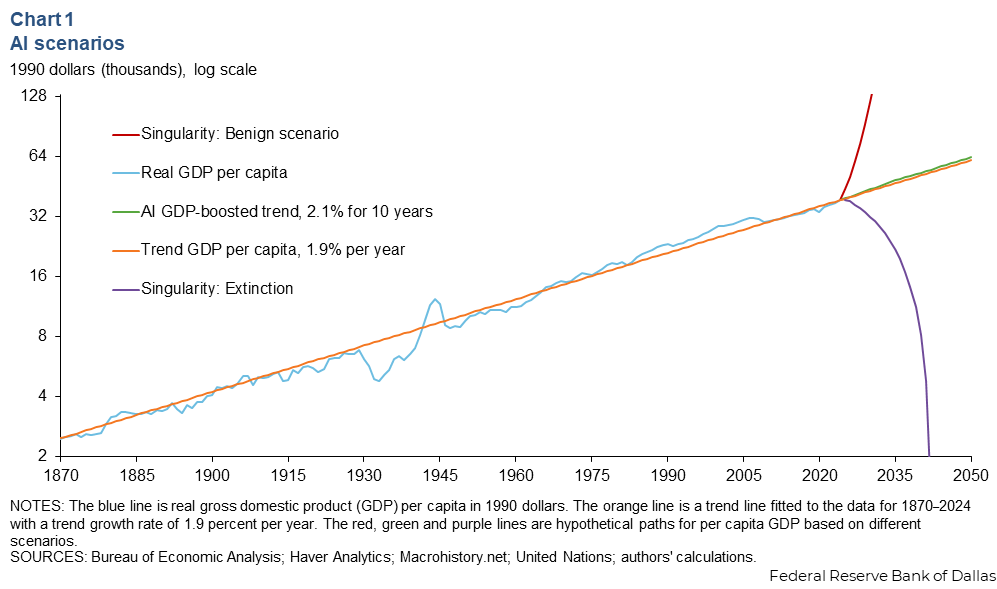

Our hopes and fears appear to be shared by policy makers at the highest levels. The Dallas Federal Reserve recently published a chart that visualizes scenarios in the event humanity can create Artificial General Intelligence (AGI).

In their analysis, AI boosts GDP by 2% as incremental improvements occur. The paths diverge however, when AGI is achieved. In the benign scenario, AGI drives enormous technological advances and GDP becomes a hockey stick. In the not so benign “extinction scenario”, GDP drops to zero. These are clearly extreme scenarios, but the Federal Reserve is explicitly drawing inspiration from science fiction. In Asimov’s classic Robots series, the author proposed “three laws of robotics” that constrained the actions of super-intelligent machines. In the Foundation trilogy, he imagined a group of scientists who create a new science and mathematics of psycho-history that aids in predicting the future trajectory of events, and this group hastens the fall of a galactic empire in decline, seeking to shorten the period of interregnum. We do not ascribe to a vision of sole global or galactic hegemony as an ideal. Nevertheless, these concepts have an eerie relevance today. Apple TV has dramatized an updated Foundation, with a plot in the last series that dwells on how the aging, self-centered emperor of an empire in decline seeks to avoid relinquishing power by destroying all potential heirs.

This is all heady stuff, but it remains speculative and we should revert to more near-term considerations.

The credit and rates markets have been eventful as well. Investors have been watching the tussle between the Federal Reserve and an administration that seeks to exercise much more direct control over interest rate policy. Thus far, the Fed appears to have warded off the administration’s attempts at direct interference, but this standoff has only been deferred.

We are also hearing more concern about the amount of private credit that has been extended in recent years, primarily to companies owned by private equity funds. First Brands, a company formed by consolidating several smaller car part manufacturers, declared bankruptcy last month. As did Tricolor, a sub-prime lender that built its business on car loans and car sales to the Spanish-speaking population.

Tricolor was undoubtedly affected by the administration’s targeting of immigrant communities. First Brands, on the other hand, tried to grow too quickly, and there have been news stories that contain questions about accounting at the firm. Each of these failures can be explained as idiosyncratic, but isolated failures can be the early signs of latent issues in the system.

The Fed has signaled that it is cautiously lowering interest rates in response to a weaker labor market. In our view, inflation concerns will likely continue to limit the pace at which it drops rates.

We continue to recommend a cautious, balanced allocation in high-grade securities for investor portfolios, including larger than typical exposure to international securities, commodities and precious metals. Equity valuations are overstretched, the credit markets appear to be showing some signs of stress, and the range of possible outcomes appears to be wider than normal. However, as the economist John Maynard Keynes once said, “markets can stay irrational longer than you can stay solvent.” So while warning signs are flashing, we recognize that markets can certainly continue their march higher despite sky-high valuations and weakening economic conditions.

Regards,

Louis Berger

Subir Grewal, CFA

Range of possible policy and market outcomes has widened

In the 1990s, policy analyst Joseph Overton proposed a theory that policy proposals were only viable if they were deemed acceptable by the mainstream of the population. Proposals that fell outside this range were deemed to be unlikely to succeed, and sit outside what was subsequently renamed the “Overton Window”. Political scientists and economists have since recognized that the Overton window can be moved, or expanded. Through repetition, proposals that might previously have seemed extreme, can gain the imprimatur of acceptability. The US is certainly experiencing an expansion of the Overton window for public policy. The old order, in both domestic and foreign affairs, appears to be on its way out.

In introductory probability theory, students are taught to work with bell-curve shaped distributions, where observations cluster around a median, mean or prior readings. Abrupt changes are rare, and trends generally shift gradually. Outcomes that are very extreme are called “tail events”, they exist out at either “tail” end of a bell curve. Probability theorists will discuss extreme events, or tail events, or refer to distributions that have more outliers as having “fat tails”.

We believe the range of possible or even likely political and economic outcomes in the medium term has widened to include more extreme events. The Overton window for political events has moved internationally as veiled and not so veiled threats are made to trading partners. It has moved internally, as masked, armed agents of the state disappear people from the streets. This administration seems to relish confrontations and in human history such confrontations generally lead to a response from countervailing forces, followed by a stronger state response, in an escalating cycle of brinkmanship. The likelihood of tail events in markets have increased as businesses and market participants orient themselves for unexpected outcomes, most of which appear to be negative.

Though we are loath to give him further attention, Elon Musk has recently exited the administration and proposed creating a new political party. His critics have countered that he should focus on his business and ignore politics. We are not admirers of Mr. Musk in his business practices or politics, but we do believe his critics are misunderstanding something. All great fortunes, such as Mr. Musk’s, and even small fortunes are dependent on the law, which in the end is dependent on politics.

The political environment in the US has shifted abruptly over the past few months. Trade is now viewed negatively and the executive branch has accused several of our trading partners of taking advantage of the US by running trade surpluses. We agree that tariffs and industrial policy are valid policy tools, however, spurring domestic growth in industries requires assuring investors that relevant policies will be stable over the course of their investment. What we have seen over the past few months from the administration is constant zig-zagging, which makes longer term investment or capital allocation difficult or impossible. At some point, as enough business managers adopt a “wait and see” attitude, a slowdown materializes. A countervailing force here is business investment in the technology sector and adjacent industries around Artificial Intelligence. The potential rewards for early movers are believed to be so large that investment has continued unabated.

Yet here too, there are significant policy risks. The US is largely a service economy, which means most of what we produce, and the value of our economy is embedded in human capital– the accumulated knowledge and capabilities of its people–rather than assets in the ground or hard goods. This certainly applies to the technology industry, including AI related enterprises.

Large swathes of the knowledge economy view their livelihoods and even their entire fields of work to be at risk under this administration. This includes researchers at universities, millions of immigrants and federal workers in specialized fields from Air Traffic Control to the National Weather Service. We have seen anecdotal reports of teams and researchers receiving offers of employment from foreign universities and enterprises as word of this administration’s hostility towards academia spreads. Relocating factories overseas atrophied domestic production lines, which will now require years or decades to rebuild. The departure or mothballing of critical talent in the US will have a long-lasting impact as well.

Our major trading and political partners have surely begun to reassess the US, and it is unlikely that many will conclude the US is a bastion of stability. In international affairs, as this administration’s actions towards Ukraine and various Middle-Eastern countries demonstrate, we are playing a destabilizing role. Even staunch allies such as Japan are therefore reconsidering where their long term interests lie. We can see this reflected in global surveys, where the US’s favorability has fallen in almost all major countries (Financial Times, July 8, 2025: Trump’s assault on American greatness)

Amongst all this uncertainty, the US consumer has continued to spend. This resilience is partly due to equity markets themselves. The US has very high levels of income and wealth inequality compared to other developed economies. Almost half of all consumer spending is driven by the top 10% of US households. These households are wealthier and tend to have larger investment portfolios. That means they are more susceptible to the “wealth effect” which postulates households spend less when they feel less wealthy (for example if their investment portfolio value falls). Conversely, their spending remains unaffected if equity markets remain high as they have this year, despite the tariff-related selloff in Q1.

The US lost its AAA rating from Moody’s this quarter. Moody’s was the final holdout, the other major rating agencies had downgraded the US years earlier. This news came on the eve of Congress passing a budget that starkly erodes public finances. The CBO estimates the budget will add $2.7 Trillion to the US deficit over the next 10 years. The credit-worthiness of any borrower, even one as large as the US Treasury, rests on two factors: the ability to pay back its debts and its willingness to do so. This budget further erodes the US’s ability to repay its debt, but that is not all. Individuals close to the current administration have suggested it could unilaterally force foreign bondholders to swap their holdings for cheaper bonds, a prospect that creditors would view as a selective default (Financial Times, May 2, 2025: How China is quietly diversifying from US Treasuries). We can envision a day where we hear senior administration officials argue that a selective default targeting NATO members is one way to get allies to share the cost of past spending for armed forces. The administration has also broadly and repeatedly undermined the Federal Reserve (Financial Times, June 29, 2025: Donald Trump’s fiscal policy and Fed attacks imperil US haven status, say economists). Taken together, most sober analysts will conclude that the US has eroded both its ability and willingness to repay its debts.

That said, some of these events could surely blow over, and all administrations float ideas to gauge public sentiment, before backing off unpopular ones. While it remains to be seen how this all plays out in the coming months/years, we will be watching these developments closely.

We are occasionally asked what we see other investors as doing, and particularly those investors we consider to be the “smart money”. We will interpret the views of three investment firms we consider worth paying attention to in matters or asset allocation or risk analysis.

1. Berkshire Hathaway is a large conglomerate which has been led by legendary investor Warren Buffet for many decades. Since the beginning of 2024, Berkshire Hathaway has more than doubled its holdings in cash, from $167 billion to over $350 billion. The explanation from its management team is that there is a paucity of profitable investment opportunities. That is another way of saying Berkshire’s leadership believes equity prices are too high.

2. GMO is a Boston-based asset manager. Unusually for large institutional asset managers, GMO actively allocates within different asset classes and is a proxy for what the smart money on the “buy side” is thinking. GMO estimates the annualized 7 year, fair value return for Large Cap US equities to be -4.9% as of May 31, 2025. GMO does believe international stocks and certain “deep value” stocks in the US offer positive return outlooks for a seven year horizon, but growth stocks which make up the largest portion of major US equity indexes appear very much overvalued in their opinion.

3. Goldman Sachs, the global investment bank, has for the past several decades carved out a niche as one of the better connected and astute sell side firms on Wall Street. No major investment bank will publicly espouse a bearish position. We can, however, see what Goldman is doing with its own book. The Fed recently completed its annual stress test for systemically important institutions, which includes Goldman Sachs. Notably, Goldman’s portfolio suffered very small losses in the scenario outlined by the Fed which includes a 40% drop in US equity prices. (Financial Times, July 2, 2025: How Goldman Sachs won big in the Fed’s annual stress test). Many observers have suggested this indicates some foreknowledge at Goldman of the test’s contours. The simpler and more direct interpretation is that the leadership at Goldman has decided to hedge much of its tradable securities portfolio because it does not like the risk-reward profile.

In Q2, equity markets rebounded from the tariff-driven selloff in March/April to set new all time highs. Some of this rally can be attributed to institutional equity managers who became overly defensive during the selloff and either went entirely to cash or shorted equities to hedge their portfolios. They are now playing catchup and have been deploying cash back into the market now that the rally has shown legs. While equities may continue to push higher from here, the circumstances that precipitated the sell-off – the Trump administration’s unpredictability around policy, their aggressive tariff stance and signs of weaker economic data– remain largely unchanged. As a result of this recent rally, equities are once again trading near all-time multiple valuations, which in the past has been a red flag signalling an eventual correction.

Because of these factors we continue to recommend a defensive, balanced allocation for most investors, in keeping with their long term goals.

Many years ago, Subir had a front row seat as his wife realigned the production of apparel and accessories across factories in Asia on behalf of a large retailer which is a household name. The aim was to achieve a saving of around 2% on duties and diversify production out of China. The business unit spent over 500 million producing products in factories across the world. The resulting cost saving approached eight figures. The work took months as raw materials sourced from Europe, Africa and other parts of Asia were redirected to a new set of factories in South-East Asia. In many cases, production was moving from a factory in one location, to one owned by the same manufacturer in another country. Nevertheless, the move required re-organizing the entire supply chain, and months of preparation. A raw material supplier in Italy that had shipped the prior season’s fabric to a factory in Guangzhou might be instructed to split the following season’s materials between plants in Vietnam and Philippines. Working relationships had to be established with personnel at the new plants, In certain cases, line workers had to be trained on new machines, or new techniques to produce a type of garment or bag they had not worked on previously. Samples produced earlier in the cycle were of limited value since the people and factory that had produced them would not produce the production run. Would the color, strength and luster of the red thread a Philippines factory used match what had been used in Guangzhou? Would line workers apply glue in exactly the same way at the same temperatures, so as to pass quality checks? Would the new factory package the finished goods in the same way? Would the freight forwarders in the new location work on the same timelines and deadlines? The questions, and the answers, and the late night calls to resolve them went on and on and on.

It took almost a year to plan, test and execute this migration from one factory to another, for a business where the product line changes 4 times a year and everyone involved is used to getting new specifications, for new products, every 3 months. There are businesses impacted by the new tariff regime that have made the same product at the same factory for years, without any change to specifications or materials. In the case of durable goods, the production line may involve thousands of parts, and simply retooling the final assembly line is an effort that costs millions.

All to say that the impact of our new tariff regime is, in our view, being underestimated by politicians. The administration has tuned out the business community’s legitimate concerns by conflating it with political agendas. It may also be true that in our popular democracy, every other generation of voters needs to learn the hard lesson of tariff wars that their grandparents did. The last time US tariffs fell into the 25-50% range for major trading partners was 1930. The infamous Smoot-Hawley act of that year began a trade war that most historians believe exacerbated the Great Depression.

Since the 1940s, the Global Agreement of Tariffs and Trade (GATT) has helped avoid such tariff wars along with the World Trade Organization (WTO) framework. The GATT/WTO era has seen a regime of predictable duties that businesses can plan around. That predictability seems to have ended, in the most dramatic fashion possible.

At millions of businesses across the world, the cost and margin implications of taxes such as duties and tariffs have become the most important issue to address. Enterprises with finished goods or materials “on the water” are going to face taxes that they did not account for when shipped. In many cases, these have to be delivered to customers at contractually agreed prices. In such cases, enterprises will have to absorb the cost of the tax and increase prices later. In other cases, they will pass on the costs immediately, and prices will rise immediately. In either case, we now have an environment where most businesses face price uncertainty. Companies will re-evaluate their unit sales expectations to account for higher costs. Consumers are likely to reduce discretionary consumption as food and other prices rise due to duties. We import virtually all our coffee for example. Business enterprises considering investments will have to account for higher costs. If you are building a factory or datacenter, you now face higher costs for machinery and raw materials. Some projects will be shelved or delayed due to the uncertain outlook. Leveraged businesses and those most affected may find they are no longer solvent. And if you still believe duties are unimportant, recall that the American revolution was at least partly driven by a change in tariffs on tea.

Earlier in the year, this administration took actions that dramatically raised insecurity for federal employees. Federal employment and more broadly government sector jobs have historically been a shock-absorber for overall employment. Positions in government don’t pay as well as equivalent roles in the public sector, but they were considered secure and reliable. The federal government has the capacity to smooth out its operations in a way that no private enterprise can. When the Trump administration began to fire Federal employees and cut federal programs, it sent shockwaves through that community. Consumer spending was down slightly in January, recovered in February, but our expectation is that spending by public sector employees will remain soft. Fear of additional job losses and tariff driven inflation are also likely to pressure consumer spending.

The sharp and sudden hike in taxes have delivered a negative external shock to the economy. The tariffs are a tax, no doubt about it. Prices for most goods will rise, creating an inflationary shock. We have already seen the market respond dramatically, with a steep drop in equities, concentrated on consumer discretionary and associated industries. This has brought us into bear market territory. If the administration were to reverse course now, the air of caution that has descended on the global business world will remain. Even if the brinksmanship at play produces the stated result and leads to trading partners agreeing to the administration’s terms, and the tariffs on such compliant trade partners are dropped, the animal spirits of the bull market will have receded.

There is a further risk that has not been discussed extensively. The US runs an overall goods and services trade deficit. We are increasingly a services economy, and we run an overall trade surplus in services (banking, software, entertainment etc), while running a deficit in goods (apparel, toys, consumer durables etc.). The current round of US duties target goods only. Trade partners may retaliate by targeting the US’ services exports alongside goods.

With these large tariff increases, the Fed is likely to find itself struggling to balance its twin objectives of price stability and full employment. Employment statistics are going to struggle under multiple short-term pressures. The Fed is likely to face a situation where they have to choose between ignoring rising unemployment or risk exacerbating inflation. Our read is that the Fed governors need to see very poor unemployment numbers to lower target interest rates significantly.

Up until April 2, much of what the Trump administration had said on trade was being discounted as bluster. We are now at a stage where these threats have been taken seriously and a recalibration is underway. The impact will deepen when the first round of tariffs takes effect on April 5. It will set in further on April 9 when the second, higher set of tariffs are implemented. Even if the administration is spooked enough to withdraw or delay the tariff regime, enough damage has been done to trade and price stability that a negative shock is baked in. President Trump has not hidden his desire to create a theater of trade deals by inviting the world leaders to directly negotiate with him. Various surrogates have echoed this invitation, thus far the Vietnamese president is the only one to have taken up the offer. Notably, the Chinese administration has not offered up a negotiation with President Jinping. Instead the ministry of trade announced an equivalent tariff. We are not sure how the current administration will respond to such perceived slights, we fear it will harden its combative elements.

So what does all this mean for investors?

There is a great deal of uncertainty ahead, but we do know a few things with high confidence.

Market strategists have begun to revise their targets downwards for 2025. Prominent strategists and economists now believe a recession is more likely than not in 2025. Price targets for companies and indices are being revised downwards. Earnings estimates will also trend downwards. Forward guidance delivered alongside first quarter results is another important indicator. We expect guidance to be negative for many listed companies. Friday saw leveraged investors (including hedge funds) confronted with a rash of margin calls.

Taken together, these observations tell us that consensus opinion has begun to shift to a negative outlook, which tends to be a self-fulfilling prophecy.

Risk assets remain close to cyclical highs in terms of valuation. The S&P 500 is at a trailing P/E ratio of 26. Major bear markets (1994, 2000, 2006, 2010) have seen this ratio approach reach or breach 15. Last week’s drop has left the Nasdaq Composite index and the Russell 2000 Index in technical bear markets. It typically takes the market 6 to 18 months to find a bottom in a bear market. Bear markets do often see short-lived, volatile rallies. But they end when long-term cycle timers, convinced that stocks now look cheap, begin buying.

We recommend extreme caution and adopting a defensive portfolio position. This is a change from our prior recommendation to stick with a balanced allocation. We will be in touch with clients this week to discuss portfolio rebalancing steps.

Regards,

Subir & Louis

The foregoing contents reflect the opinions of Washington Square Capital Management and are subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or constructed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

We trust you and yours had a warm holiday season and a good start to the New Year.

Sadly, we know some of our friends are dealing with the impact of the massive fires in Los Angeles over the past month. We know of several families in our extended network who have been displaced and some who have suffered devastating losses. Our thoughts are with them and their loved ones.

The immediate human impact of the fires has been apparent for weeks. In our view, there are three long term impacts which will take longer to manifest themselves over the coming years.

Firstly, the role of climate change in the extent of these fires cannot be denied. Seasonal rains have failed to materialize in Southern California. This coupled with the hottest year on record globally and high winds, created the conditions for a devastating group of wildfires. The impact of climate change has been evident for decades, yet efforts to limit it have barely made a dent in the growth of greenhouse gas emissions. The largest advances in moving towards renewable fuels have been made outside of the various diplomatic efforts to reduce emissions, driven by certain countries (primarily China and India) seeking to address the fact that they do not have significant fossil fuel reserves. The move to electric vehicles has now gained enough momentum to bend the emissions curve in the medium term, but we will still have to contend with the impact of the warming that has already occurred.

Second, the failure at national and global levels to limit greenhouse gas emissions is coupled with the unwillingness or inability of local governments to prepare for the impacts of climate change. Los Angeles’ building codes and local services were unprepared for such a disaster, despite many premonitions. Local officials are unwilling to institute the tough budgetary and zoning measures that would harden their environments. This is not unique to Los Angeles. Various cities with waterfront property are unprepared for storm surges and the rise in sea levels implied by our current 1.5 degrees of global warming. Los Angeles is one of the wealthiest places in the world, as is California. Poorer regions and cities will have to contend with far fewer resources to deal with the coming impacts of climate change. It is also unreasonable for us to expect that we might be insulated from the impacts by wealth or individual preparedness. A widespread series of natural disasters will impact us all. As Los Angeles vividly demonstrates, the wealthiest regions of the world shall not be immune to the deleterious effects of climate change. Even in wealthy areas, retro-fitting housing and other structures to harden them against climate change will face funding obstacles and opposition from naysayers. The eventual result is likely to be a series of entirely predictable disasters, with pliant local authorities absolving their inaction by references to acts of god. This pattern is likely to enhance the appeal of strongmen for a citizenry that is frustrated by the inaction and lack of vision exhibited by the status quo.

Third, the losses are going to change the behavior of the insurance industry. On one day in January, we saw estimated insurance claims from the LA fires rise from $10Bn to $50Bn, with total losses estimated at over $150Bn. These losses can easily be covered by US property & casualty insurers and global re-insurers. However, close on the heels of the $25Bn losses from Hurricane Helene, mostly inland, insurers have begun to change their risk assessments. We expect many insurers to exit markets they deem uninsurable, especially in areas prone to flooding during storms and those vulnerable to wildfires.

Risk assets continued their rise in 2024, with the S&P 500 ending the year close to all time highs. This was coupled with an election that unified control of the executive, legislative and judicial branches in the hands of Republican officials. We suspect internal divisions among Republican factions may limit action on certain controversial proposals, but tax and regulatory policy can be expected to be less strict under this administration. This would normally argue for a risk-on strategy, but two factors should limit such exuberance. Firstly, internal divisions and the unpredictable nature of the Trump administration is likely to cause concern among investors, though in contrast to the first Trump administration, large American businesses are lining up to ally themselves with the current administration. Secondly, market valuations remain at cyclical highs, advocating for more moderate positioning.

We continue to recommend a balanced allocation that includes exposure to commodities and fixed income, especially given the more attractive rates that are on offer. While growth stocks have substantially outperformed value over the past two years, we expect investors will start to rotate back into value stocks if inflation continues to moderate and economic growth cools. Since Trump’s election win, investors have been concerned with the inflationary risk inherent with two of his major policy goals – immigrant deportation and tariffs. While these concerns are certainly warranted, it’s very possible they have already been fully baked into market expectations and there could be a disinflationary surprise if the Trump administration is unable to fully deliver on these campaign promises. Either way, we expect 2025 will likely see heightened volatility compared to the past two years as the market adjusts to this new political reality.

Regards,

Subir and Louis

The foregoing contents reflect the opinions of Washington Square Capital Management and are subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or constructed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

We trust you have been well and had a pleasant summer.

The storms of the past month reminded us of the precariousness of life and the old quote from radio broadcaster Paul Harvey: “despite all our accomplishments, we owe our existence to a six-inch layer of topsoil and the fact that it rains”. We have friends and acquaintances in the Asheville, NC area who have lost homes and had their lives upended. It is clear that man-made climate change has made weather events much more powerful and capable of dropping enormous amounts of rain far further inland than previously imagined. We saw a very similar set of floods in the mountains of Vermont after Hurricane Irene. As we write this, Hurricane Milton has just torn through the western coast of Florida after record-high water temperatures in the Gulf of Mexico fueled it to become the fastest hurricane on record to reach category 5 level.

We have witnessed decades of inaction on climate change by American lawmakers in both parties, who are largely captive to domestic fossil fuel interests. Thankfully, the other large global economies, Europe, China, Japan and India do not have large, domestic fossil fuel energy reserves. Over the past few decades, these countries have begun to treat fossil fuel imports as a national security issue and prioritized a transition to renewables (and nuclear energy in some cases). This has dramatically changed the energy consumption mix of the world. Over the next 10-20 years, we expect to see fossil fuel use begin to drop in many large economies. Let us hope it isn’t too late to prevent enormous suffering.

As widely anticipated, the Federal Reserve began cutting interest rates in September with a 50 bps initial reduction. This comes on the heels of continued softening of inflation data as the Fed has now determined that higher rates are unnecessarily restrictive on the economy. We expect a slow, steady pace of rate cuts going forward, and, absent extraordinary circumstances, we would expect the Fed to aim to stabilize at around 3%. This is good news for bond investors who have had to muddle through roughly 20 years of near-zero interest rate policies.

That said, there are significant tail risks that could drive markets and rates in extreme directions. The Israeli bombing and invasion campaigns in the Middle-East, and unwavering US support for them are contributing to a change in long-term political alignments in Asia and much of the global south. When coupled with the US’s active sanctions policy and actions like the Biden administration’s ban on Chinese electronic components in cars, the potential exists for a dramatic shift in global trade.

The US currently imposes some form of sanctions on roughly 20% of the world’s economic activity. Successive US administrations have increased the pace of sanctions, viewing it as a convenient policy tool. The result is that the US now imposes hundreds of sanctions each year.

This is rapidly isolating the US, and it is becoming increasingly difficult to claim sanctions are driven by a moral imperative when the US supports questionable, but pliable regimes on multiple continents. We can easily imagine a future where China and Russia establish, or re-establish parallel technology, trade and industrial systems to protect themselves from US sanctions. We can also see a future where Asian, Latin American and African industry shift to these alternative trade, industry, technology platforms. Such a move would not be unprecedented. We have seen such shifts in trade and industry during the Industrial Revolution, the rise of the US and Soviet Union in the 20th century, and throughout human history. This change is made possible by the trajectory India and China are on to recover the positions they occupied as industrial powerhouses prior to the 19th century. Within the US, such changes can exacerbate a difference in views between the East and West coasts, with elites in the west looking towards Asia, while those in DC and the east continue to look towards Europe as their primary partner in trade. Whether these tensions are resolved, or lead to breaks, may determine the long-term health and state of the US economy.

Despite increased geopolitical tensions and the specter of a potentially chaotic presidential election on the near horizon, markets have continued to remain remarkably resilient this year

as risk assets have scaled new highs over the past month, in spite of a short-lived correction during the summer. Long term measures of equity market value (Shiller P/E) are at near record highs (37x times earnings). The last time we saw multiples at these levels were briefly in 2021 and before that in 1999/2000 during the run-up to the dot com bust. During that period, the Shiller P/E level reached the low 40’s before falling precipitously with the stock market in 2001/2002. It’s possible markets revisit those stratospheric valuation levels, but if they do, it’s likely the aftermath will be particularly unpleasant for equity investors.

With the Fed launching into their easing campaign, we think dividend stocks, bonds and precious metals continue to look compelling as interest rates come down and the USD weakens in response. For now, economic data has been holding up relatively well, but if we see signs of a slowdown, we would expect the speculative growth tech stocks that have been fueling the rally of the past two years to sputter. So far that has not been the case, but we are keeping a close eye on the data and will look to reduce risk when appropriate.

Let us know if you’d like to discuss any of the above.

Best,

Subir and Louis

The foregoing contents reflect the opinions of Washington Square Capital Management and are subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or constructed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

As we head into spring, we are reminded of new beginnings. Like most people of a certain age in the northern hemisphere, we have been pottering about in our gardens. Pulling out old growth and planting the new. It seems to us that the American economy has been in the throes of a decades-long process that mirrors spring planting, in a way, but that this process has been lacking clear direction.

In the middle of the last century, American industrial might reigned supreme. Most competitors had seen their industrial capacity destroyed by the war, and it took decades for them to recover. American enterprise had almost no meaningful competition in certain sectors. The US built an extensive network of roads, airports and ports that helped transport goods across the country and the world.