On hard and soft landings

Dear Friends,

We hope you’ve enjoyed a restful holiday season and a wonderful start to 2024.

The fourth quarter saw heavy volatility across nearly all asset classes as inflation and the Fed’s response continued to be the main driver of market direction. October began with long term interest rates continuing their upward trajectory as the “higher for longer” narrative took hold and investors expected the Fed would need to raise rates considerably higher in order to rein-in inflation. Due to the projected increase in borrowing costs, this move in rates put considerable pressure on stocks, particularly stocks in capital intensive industries. From the end of July to the end of October, the S&P 500 suffered a 10% correction despite near-record corporate earnings. But following a cooler than expected inflation print for October–3.2% vs. 3.3% expected in the Consumer Price Index–and dovish commentary from Fed Chairman Powell, both stock and bond markets reversed course in November and rallied strongly into year-end, with the S&P 500 ending within striking distance of all time highs.

As discussed in previous letters, our expectation was to see a sharp rally in risk assets once the Fed signaled a pause in rate hikes and inflation looked to be under control. And markets responded accordingly in November and December. The key question for investors is will this rally have follow-through into the New Year?

For 2024, like 2023, we think market direction will continue to hinge largely on inflation and the Fed’s response. The market currently expects the Fed to begin cutting rates this year as inflation cools (as signaled by the Fed Board of Governors). However, as we saw in October, market expectations don’t always jibe with how things eventually play out.

Going forward, there are three paths the economy can take this year with regards to inflation and Fed response:

- Soft landing: In this scenario, inflation continues to cool, reaching the Fed’s target of 2% in a gradual and controlled manner without triggering a significant spike in unemployment or an economic recession. The Fed would slowly ease rates and we would expect to see stocks and bonds continue to perform well.

- Hard landing: In this scenario, the Fed’s rate hikes cool the economy too much, triggering an economic recession and a significant spike in unemployment. This would lead the Fed to cut rates aggressively in order to re-stimulate the economy. We would expect to see stocks (particularly growth stocks) perform poorly while investment grade bonds and treasuries would perform well (acting as a safe haven).

- No Landing: In this scenario, inflation would reignite and remain sticky, settling in at a rate 1-2% points above Fed target with continued economic overheating. This would cause the Fed to keep nudging rates higher. We would expect floating rate bonds and commodities to perform well while longer term bonds would perform poorly. Growth stocks would likely outperform value stocks.

Which scenario is most likely? A no-landing scenario is very uncommon (and somewhat controversial) – one could argue the last time the US economy experienced anything like this was in the late 1970’s/ early 1980’s. This period also coincided with the last time the economy encountered a similar spike in inflation, so, while unlikely, one can’t rule this scenario out entirely.

A soft landing, which is the ideal scenario for the Fed, policy makers and investors, has more historical precedence. The most recent clear example would be in the mid-90’s, where the rate hiking cycle ended in April of 1995 and there was no subsequent economic recession.

The end of the last three rate hiking cycles arguably resulted in hard landings: Jan 1999-July 2000 culminated in the Dotcom bust, May 2004-July 2006 preceded the Great Recession, and Nov 2015-Jan 2019 preceded the Covid crash. Some current and former Fed officials argue that Fed interest rate policy was not directly responsible for the Great Recession and the Covid crash and that the economic contraction following the rate hikes of 1999-2000 was mild. There may be some credence to this argument, but as investors we believe it’s important to consider that the end of the last three rate hike cycles (cycles in which the Fed has had an increasingly influential role) presaged significant market corrections.

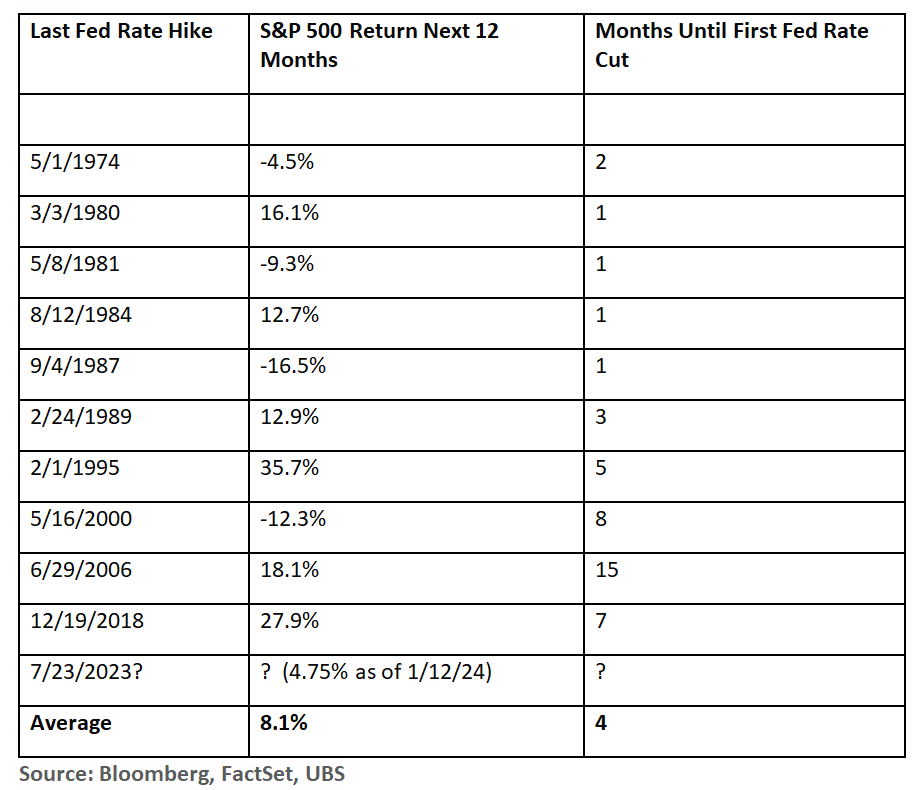

All that said, if market expectations are correct and the Fed is done hiking and we eventually see a hard landing, does that mean it’s now time for investors to run for the hills? Not necessarily. If we look at the end of previous rate hike cycles since 1974, the S&P 500 averaged an 8.1% return over the 12 months following the last hike. Four out of the last five cycles saw double digit positive returns (the exception being the 2000 cycle).

If we are to assume the Fed is done raising rates for this cycle, the S&P 500 has returned 4.75% from the last hike date of 7/23/23 through 1/12/24. This is below the 8.1% average, implying there could be further upside for equities.

But what happens when the Fed starts cutting rates?

Things look decidedly less rosy.

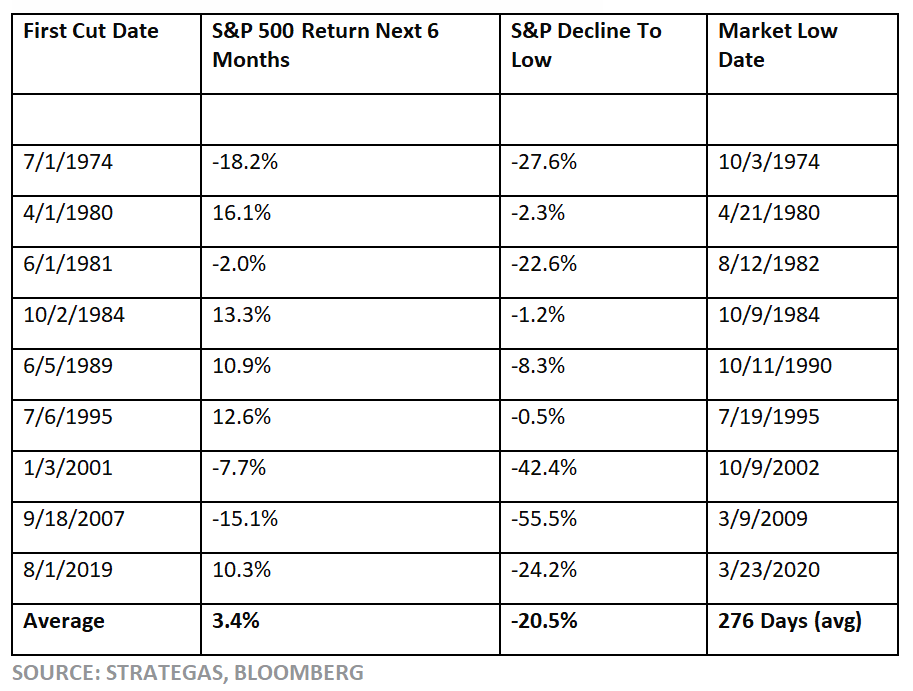

Looking again at rate cycles from 1974, once the Fed begins cutting, the S&P 500 has returned an average of 3.4% in the following 6 months. However, when considering the S&P 500 cycle low from the date of the first rate cut, the average return is -20.5% with a duration of 276 days to the cycle low from the first cut date.

When looking at the data, you can see the gold standard for soft landings occurred in 1995, when the S&P 500 returned 12.6% over 6 months following the first rate cut and saw a cycle low of just -0.5% 13 days after the first rate cut. On the flip side, the hard landing of the Great Recession saw the S&P 500 return -15.1% 6 months after the first rate cut and saw a cycle low of -55.5% 538 days after the first rate cut.

So what conclusions should investors draw? When the Fed concludes its rate hiking cycle and pauses, historically on average, equity markets tend to perform pretty well over the following 12 months. However, once the Fed begins to cut rates, near term upside for stocks is muted and downside risk increases significantly after the first 6 months. So, in our view, investors should view a rate cut as a signal to reduce risk across all assets.

Of course, each market cycle is unique and past performance is no guarantee of future results. Also, 2024 is a year in which there is a presidential election and what looks to be a pronounced uptick in geopolitical conflicts. These types of events of course can and will influence markets and upend prior narratives.

We continue to believe a well-diversified portfolio with exposure to US and international stocks along with bonds and commodities is a prudent approach to the current market environment. Should we see a slowdown in economic growth that leads the Fed to begin cutting rates, our approach will be to reduce equity exposure and increase exposure to short term treasuries.

Let us know if you would like to discuss any of the above in more detail.

Best,

Louis and Subir

The foregoing contents reflect the opinions of Washington Square Capital Management and are subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or constructed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.