Tariffs and Federal firings undermine confidence

Friends,

Many years ago, Subir had a front row seat as his wife realigned the production of apparel and accessories across factories in Asia on behalf of a large retailer which is a household name. The aim was to achieve a saving of around 2% on duties and diversify production out of China. The business unit spent over 500 million producing products in factories across the world. The resulting cost saving approached eight figures. The work took months as raw materials sourced from Europe, Africa and other parts of Asia were redirected to a new set of factories in South-East Asia. In many cases, production was moving from a factory in one location, to one owned by the same manufacturer in another country. Nevertheless, the move required re-organizing the entire supply chain, and months of preparation. A raw material supplier in Italy that had shipped the prior season’s fabric to a factory in Guangzhou might be instructed to split the following season’s materials between plants in Vietnam and Philippines. Working relationships had to be established with personnel at the new plants, In certain cases, line workers had to be trained on new machines, or new techniques to produce a type of garment or bag they had not worked on previously. Samples produced earlier in the cycle were of limited value since the people and factory that had produced them would not produce the production run. Would the color, strength and luster of the red thread a Philippines factory used match what had been used in Guangzhou? Would line workers apply glue in exactly the same way at the same temperatures, so as to pass quality checks? Would the new factory package the finished goods in the same way? Would the freight forwarders in the new location work on the same timelines and deadlines? The questions, and the answers, and the late night calls to resolve them went on and on and on.

It took almost a year to plan, test and execute this migration from one factory to another, for a business where the product line changes 4 times a year and everyone involved is used to getting new specifications, for new products, every 3 months. There are businesses impacted by the new tariff regime that have made the same product at the same factory for years, without any change to specifications or materials. In the case of durable goods, the production line may involve thousands of parts, and simply retooling the final assembly line is an effort that costs millions.

All to say that the impact of our new tariff regime is, in our view, being underestimated by politicians. The administration has tuned out the business community’s legitimate concerns by conflating it with political agendas. It may also be true that in our popular democracy, every other generation of voters needs to learn the hard lesson of tariff wars that their grandparents did. The last time US tariffs fell into the 25-50% range for major trading partners was 1930. The infamous Smoot-Hawley act of that year began a trade war that most historians believe exacerbated the Great Depression.

Since the 1940s, the Global Agreement of Tariffs and Trade (GATT) has helped avoid such tariff wars along with the World Trade Organization (WTO) framework. The GATT/WTO era has seen a regime of predictable duties that businesses can plan around. That predictability seems to have ended, in the most dramatic fashion possible.

At millions of businesses across the world, the cost and margin implications of taxes such as duties and tariffs have become the most important issue to address. Enterprises with finished goods or materials “on the water” are going to face taxes that they did not account for when shipped. In many cases, these have to be delivered to customers at contractually agreed prices. In such cases, enterprises will have to absorb the cost of the tax and increase prices later. In other cases, they will pass on the costs immediately, and prices will rise immediately. In either case, we now have an environment where most businesses face price uncertainty. Companies will re-evaluate their unit sales expectations to account for higher costs. Consumers are likely to reduce discretionary consumption as food and other prices rise due to duties. We import virtually all our coffee for example. Business enterprises considering investments will have to account for higher costs. If you are building a factory or datacenter, you now face higher costs for machinery and raw materials. Some projects will be shelved or delayed due to the uncertain outlook. Leveraged businesses and those most affected may find they are no longer solvent. And if you still believe duties are unimportant, recall that the American revolution was at least partly driven by a change in tariffs on tea.

Earlier in the year, this administration took actions that dramatically raised insecurity for federal employees. Federal employment and more broadly government sector jobs have historically been a shock-absorber for overall employment. Positions in government don’t pay as well as equivalent roles in the public sector, but they were considered secure and reliable. The federal government has the capacity to smooth out its operations in a way that no private enterprise can. When the Trump administration began to fire Federal employees and cut federal programs, it sent shockwaves through that community. Consumer spending was down slightly in January, recovered in February, but our expectation is that spending by public sector employees will remain soft. Fear of additional job losses and tariff driven inflation are also likely to pressure consumer spending.

The sharp and sudden hike in taxes have delivered a negative external shock to the economy. The tariffs are a tax, no doubt about it. Prices for most goods will rise, creating an inflationary shock. We have already seen the market respond dramatically, with a steep drop in equities, concentrated on consumer discretionary and associated industries. This has brought us into bear market territory. If the administration were to reverse course now, the air of caution that has descended on the global business world will remain. Even if the brinksmanship at play produces the stated result and leads to trading partners agreeing to the administration’s terms, and the tariffs on such compliant trade partners are dropped, the animal spirits of the bull market will have receded.

There is a further risk that has not been discussed extensively. The US runs an overall goods and services trade deficit. We are increasingly a services economy, and we run an overall trade surplus in services (banking, software, entertainment etc), while running a deficit in goods (apparel, toys, consumer durables etc.). The current round of US duties target goods only. Trade partners may retaliate by targeting the US’ services exports alongside goods.

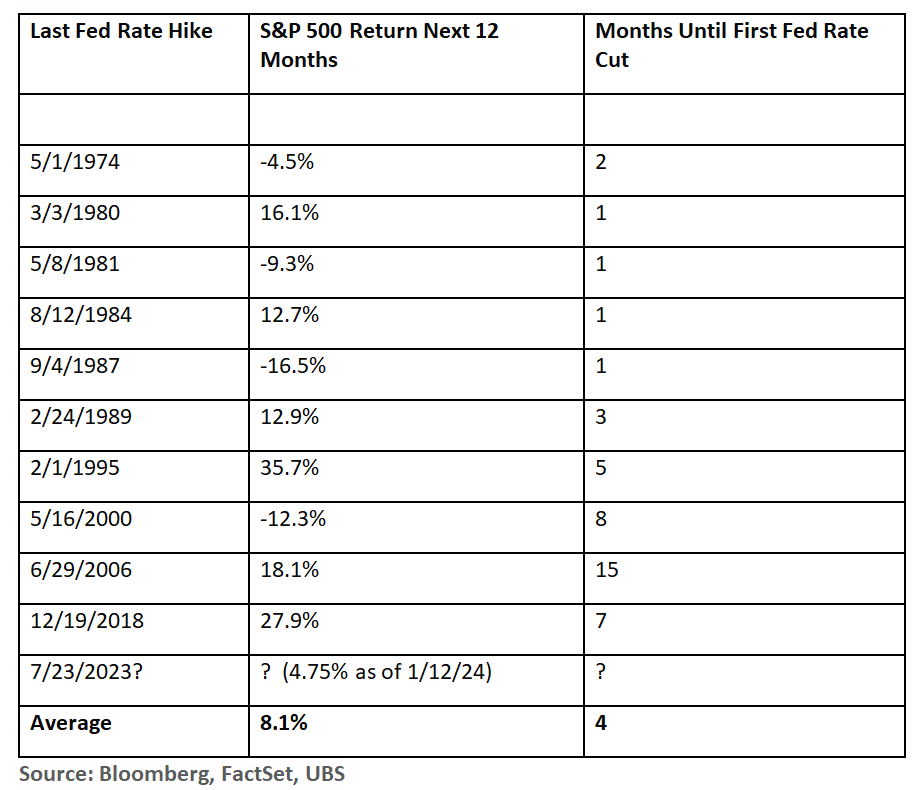

With these large tariff increases, the Fed is likely to find itself struggling to balance its twin objectives of price stability and full employment. Employment statistics are going to struggle under multiple short-term pressures. The Fed is likely to face a situation where they have to choose between ignoring rising unemployment or risk exacerbating inflation. Our read is that the Fed governors need to see very poor unemployment numbers to lower target interest rates significantly.

Up until April 2, much of what the Trump administration had said on trade was being discounted as bluster. We are now at a stage where these threats have been taken seriously and a recalibration is underway. The impact will deepen when the first round of tariffs takes effect on April 5. It will set in further on April 9 when the second, higher set of tariffs are implemented. Even if the administration is spooked enough to withdraw or delay the tariff regime, enough damage has been done to trade and price stability that a negative shock is baked in. President Trump has not hidden his desire to create a theater of trade deals by inviting the world leaders to directly negotiate with him. Various surrogates have echoed this invitation, thus far the Vietnamese president is the only one to have taken up the offer. Notably, the Chinese administration has not offered up a negotiation with President Jinping. Instead the ministry of trade announced an equivalent tariff. We are not sure how the current administration will respond to such perceived slights, we fear it will harden its combative elements.

So what does all this mean for investors?

There is a great deal of uncertainty ahead, but we do know a few things with high confidence.

Market strategists have begun to revise their targets downwards for 2025. Prominent strategists and economists now believe a recession is more likely than not in 2025. Price targets for companies and indices are being revised downwards. Earnings estimates will also trend downwards. Forward guidance delivered alongside first quarter results is another important indicator. We expect guidance to be negative for many listed companies. Friday saw leveraged investors (including hedge funds) confronted with a rash of margin calls.

Taken together, these observations tell us that consensus opinion has begun to shift to a negative outlook, which tends to be a self-fulfilling prophecy.

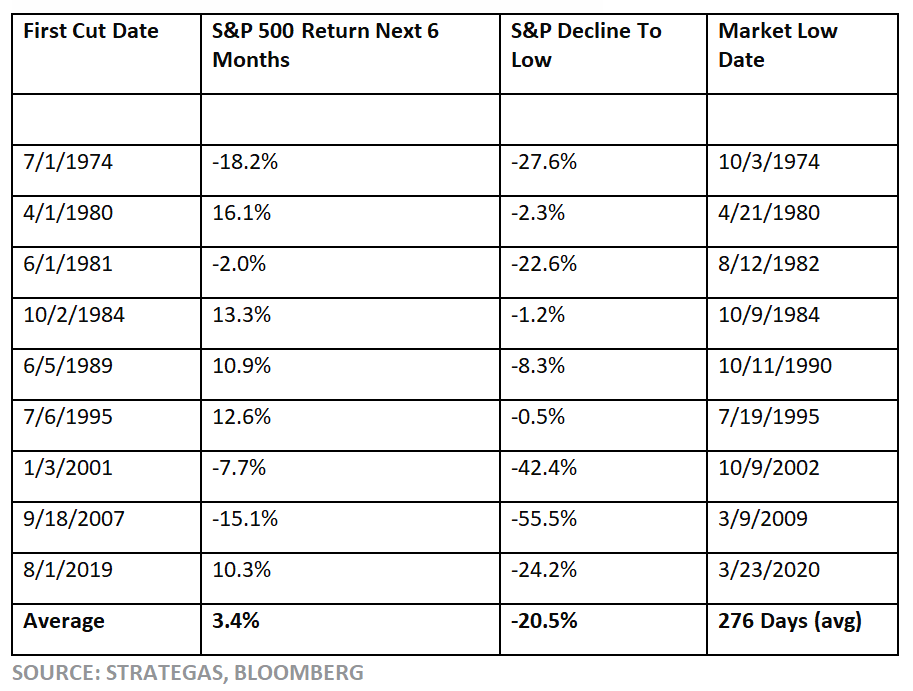

Risk assets remain close to cyclical highs in terms of valuation. The S&P 500 is at a trailing P/E ratio of 26. Major bear markets (1994, 2000, 2006, 2010) have seen this ratio approach reach or breach 15. Last week’s drop has left the Nasdaq Composite index and the Russell 2000 Index in technical bear markets. It typically takes the market 6 to 18 months to find a bottom in a bear market. Bear markets do often see short-lived, volatile rallies. But they end when long-term cycle timers, convinced that stocks now look cheap, begin buying.

We recommend extreme caution and adopting a defensive portfolio position. This is a change from our prior recommendation to stick with a balanced allocation. We will be in touch with clients this week to discuss portfolio rebalancing steps.

Regards,

Subir & Louis

The foregoing contents reflect the opinions of Washington Square Capital Management and are subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or constructed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct.

Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.