It was the best of times, it was the worst of times.

Friends,

The past several months have been a very challenging time bringing dramatic changes to all our working and personal lives. We hope you and your family are safe and in good health.

In the capital markets world, the past quarter has been nothing short of remarkable. In March, we saw the quickest descent into a bear market in S&P 500 history, driven by the extreme measures required to contain the spread of the Covid-19 pandemic. The S&P 500 hit a low of 2,237 for the year in late March. The 10Yr Treasury rate fell below 1% for the first time in its history. Since then, buoyed by trillions of dollars of stimulus support from governments and central banks around the world, many equity markets have recovered from those lows. The S&P 500 closed the second quarter at 3,100, only 10% below it’s all-time high reached in February. Most international equity markets have made similar recoveries as investors have shrugged off the economic fallout from COVID-19 with a view that any economic downturn will be short-lived and overcome by the flood of liquidity provided by central banks.

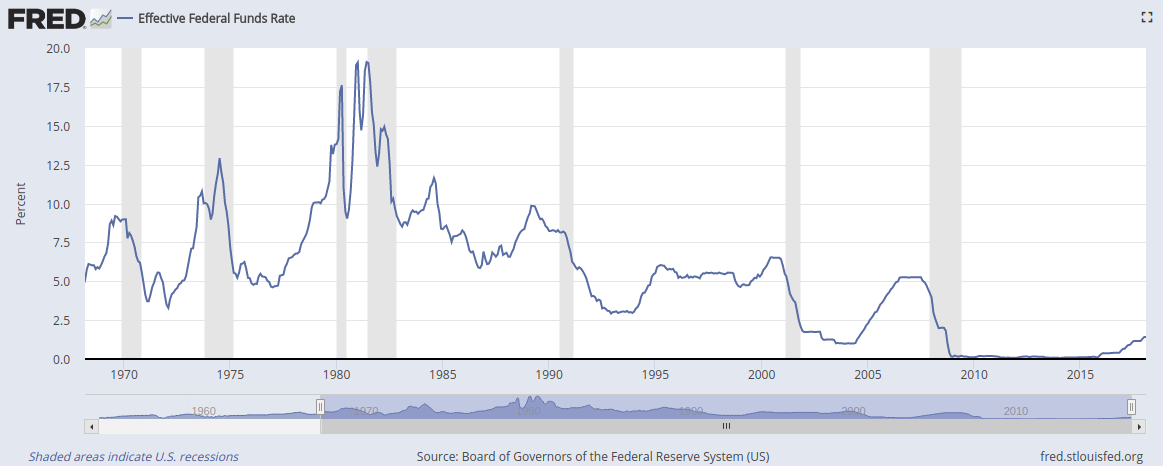

Bond markets are, in contrast, pointing to a far more pessimistic outlook. The 10 year treasury continues to trade below 0.70%, a level never reached before 2020. Buyers of 10 year Treasuries believe rates in the US will remain below 1% for most of the next 10 years. The 10 year rate for German bonds is -0.47%. That’s not a typo, it is a negative rate. Investors are paying the German government for the privilege of giving it money. Bond markets, which are larger and tend to be more restrained than equities markets, point to a deep and extended recession across much of the world.

Economic indicators seem to support the bond market’s view. In February 2020, over 152 million people in the US were employed in non-farm related activity. By May, that number had fallen to 130 million, as several industries largely shuttered their doors. June has seen some limited gains, with non-farm employment increasing to 138 million. The resurgence of Covid-19 cases in various parts of the country puts much of that partial recovery in employment at risk. And there’s concern that as the pandemic drags on many of these job losses may be permanent.

This pandemic has also stretched to the limit, the finances of many municipalities and states. Government entities generally maintain more stable levels of hiring and employment, but we have begun to see furloughs and layoffs in the government sector as well.

The public health response in the US has been decidedly mixed. State governments across much of the North-East and Pacific coast appear to have acted on the advice of public health experts. In contrast, state governments across the south and south-east have been less careful, opening many public venues, beaches and businesses earlier than public health experts recommended. The unfortunate, predictable result is that the south and south-east of the country now have confirmed case rates that are as high as the north-east at its peak.

This pandemic has also exposed sharp differences in the response and capabilities of public health officials in different countries. When compared with the well-coordinated action taken in other countries, it seems clear to us that the US government has bungled its response to this pandemic. The rate of new infections has fallen sharply in much of Europe and several Asian countries like Japan, Taiwan, Vietnam and China. In contrast, the US, India and Brazil are reporting record numbers of new cases each day. And unlike India and Brazil, the US is a developed nation that should have the organizational and healthcare infrastructure capacity in place to handle this type of crisis.

Back in February and March, there was a faint chance that a strong, coordinated global response might contain and then end the spread of the virus. The prior experience with SARS gave some hope. With confirmed global cases now at 13 million and rising sharply, it is clear that containment is not possible, unless far more draconian social isolation measures are implemented immediately across the world. This scenario seems highly unlikely. Our best hope now is that a vaccine or cure is found and the long-term health impact of contracting this virus is contained.

A great deal of uncertainty remains around the future trajectory of economic conditions and asset prices. A lot depends on the efficacy of potential vaccines and treatments for those sickened by the virus. The ability and capacity of businesses to adapt to changed circumstances is another key factor. Many businesses operating on thin margins have experienced enormous financial stress over the past few months. We have seen several high profile bankruptcy filings and expect to see many more before year-end. The response of consumers and workers to dramatically changed living and working conditions will play a large role in determining the level of economic activity in the months to come. Many households in the US and across the world have undergone severe financial strains over the past few months as several industries like hospitality, travel and entertainment have seen revenues dry up. When these workers return to their old jobs, or find new ones, we expect they will be more cautious about their consumption habits for quite some time.

Our view is that the US and economies around the world remain in the midst of a sharp global recession. The ineffective pandemic response in several large economies virtually guarantees that the impact of the pandemic will be with us through the rest of the year. As value investors looking at the level and direction of economic indicators, we see severe challenges for most businesses, a weak earnings environment and a significant drop in consumer demand. While governments and central banks around the world have thrown trillions of dollars as a stopgap to address economic fallout, we don’t see this as a solution so long as the pandemic continues its current trajectory. That said, can asset prices continue to rise despite being completely untethered to the underlying economy? The answer is yes. The past few months have shown how flooding liquidity into the marketplace can boost stock prices. But rather than fixing the underlying problems in the economy, this liquidity is merely blowing up an asset bubble and stretching valuations to heights we haven’t seen since the dotcom bust in 2000. As any long term investor knows, the problem with asset bubbles is they eventually pop, often without any advance warning.

We recommend investors remain very cautious, and limit allocations to risk assets like equities. We think investment grade bonds, inflation protected bonds, emerging market bonds and precious metals (gold and silver) are good alternatives in this environment. We continue to believe there will be an opportunity to buy high quality risk assets at significant discount in the coming months.

Regards,

Subir Grewal, CFA, CFP Louis Berger

Dear Friends,

Dear Friends, Fed stays the course

Fed stays the course