How low can the S&P 500 go?

The demand shock created by the Coronavirus outbreak has already created historic levels of market volatility. Today, the market plunged after the Fed announced in a call on Sunday that it would cut rates to zero and implement buying programs for US Treasuries and Mortgage Backed Securities. During such periods of market volatility, we keep an eye on both “technical” analysis, and fundamental “value”. One question we’ve been asked repeatedly by clients is when they should consider entering the market.

Our short answer is not yet, unless you see a compelling opportunity in an individual stock. The companies trading at the steepest discounts are the ones most affected by the current virus driven downturn, oil, travel, airlines, hospitals, restaurants etc. Since the real economic impact and the length of the widely expected global downturn is still unknown, we advise investors to be very cautious when evaluating such stocks.

The follow-up question is always, well when should we begin to buy. That is a question we cannot answer definitively, but we can identify levels that are of interest to an investor looking for a signal of a market bottom.

We are going to outline a case that S&P 500 levels can go far lower, as a means of stress testing our theses. We do not know what the magnitude of the economic shock the US and global economies will suffer. It does appear though, that large and extensive are the operative words. The Empire State Manufacturing survey (an indicator of economic activity in New York state), fell by the largest amount ever. Estimates of GDP in China (which appears to have controlled the outbreak) are extraordinary. Industrial output declined more than 13.5%, retail and investment were down more than 20%, auto sales have dropped 80%. These are traumatic adjustments and we are nort persuaded by the view that consumers and businesses will snap back to normal when the quarantines pass.

Jim Reid, a strategist at Deutsche Bank, added that “the impact of the various Western World shutdowns will mean that at its peak the Covid-19 impact on the global economy will likely be worse than the peak of the financial crisis.” — Stocks gain after biggest Wall Street sell-off since 1987

https://www.ft.com/content/a9d76acc-67ee-11ea-a3c9-1fe6fedcca75?shareType=nongift

Tuesday will deliver a number of US economic indicators including Advance Retail Sales, Industrial Production and Business leaders survey, so we will get a better look at how the US economy fared in these very early stages. While we await better data, we can work with simple assumptions about earnings.

S&P 500 index earnings for 2019 were slightly over $140. Let’s assume earnings drop 25% for 2020. That’s not unimaginable given the extreme stress on oil, airlines, retail, yield curve, durable goods, trade etc. That gets us to $105 earnings. This sounds extreme, but might in fact be optimistic since it doesn’t account for losses, which are widely expected in some sectors. A 5% drop in revenues can drive a 25% drop in earnings in many industries.

$112 is equivalent to 2016-2017 earnings, when index levels were roughly 2000-2400. It is worth noting that this is a global event, and different economies are being impacted at different times. Most of Asia has led, with enormous impacts in Q1. Europe, the US, Africa, South America are following, with impacts in late Q1 and Q2. In our globalized world, as economies try to recover, they could be dragged down by the fact that others have not fully recovered or are entering recession.

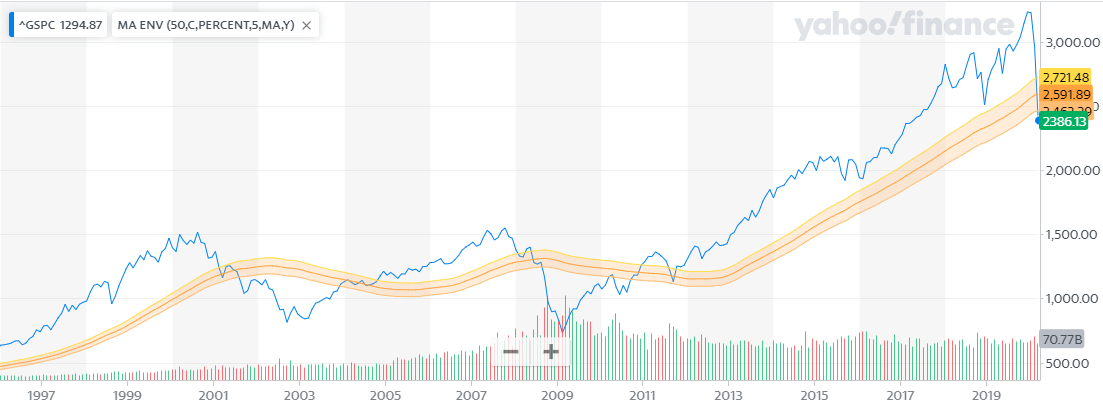

Now let’s discuss multiples. Today’s close around 2400 puts prices at 17x trailing earnings (i.e. a p/e of 17). We generally assume there will be support at 10-12.5x from long cycle timers (we include ourselves in that cohort). So we end up with 4 critical levels for the S&P 500:

- 2400 (Dec 2018 low)

- 2000 (2016/2017 levels)

- 1300 (12.5x estimated $105 in 2020 earnings)

- 850 (very long term trend line support)

The 2000-2400 levels are corroborated by other value investors. GMO, one of the large investment managers we follow, publishes a 7 year return expectation for each asset class. In January, they forecast the annual expected return on US large cap equities (S&P 500) was -4.7%. That implies GMO believes the S&P 500 would deliver a 0% return at 70% of its January levels. In January, the index was at 3270. 70% of that is roughly 2300.

A measure we follow closely is Robert Shiller’s Cyclically Adjusted P/E (CAPE), which averages 10 year earnings to smooth out cyclical effects. In January, with the S&P 500 at 3270, CAPE was over 31. In 2009, CAPE bottomed out at about 13. CAPE at 13 would place the index at 1300.

We understand that the last two levels may be shocking. However, we were last at 1300 in 2012, that’s 8 years ago. In 2009, the S&P re-trenched to a level last seen in 1996, 13 years prior. We were last at 850 in 2009, which was 11 years ago. So by that reversion metric, even 850 is not outlandish.

Many investors believe stocks bottom out in a recession at 10x earnings, a 40% reduction in 2019 earnings would get us to $84 earnings. 10x $84 places us at 840. Notably, this is a significant long-term trend-line extending from many major lows, including 1929 and 2009.

Of course, it is possible that none of these scenarios materialize and we recover from current levels. However, we have to consider that possibility as well. We are beginning to see some buying opportunities, but we do not see the market action that would suggest a bottom has been reached. We have seen dramatic declines based entirely on expectations of poor economic data. If the measured economic readings reach levels seen in China, or the economy stalls due to distress among a spate of small/medium sized businesses, we could see the lower cases materialize.

For long-term investors, it is very important to note that timing such swings in very difficult. Our approach is to take gradual steps to return to long-term allocations. We believe the next 6-9 months are critical. Ours is a resilient species, society and economic system. We will, in good time, recover from this challenge as we have from so many that came before. We are prepared to act on behalf of clients to invest in attractive equity issues when the timing warrants.

We wish you and your families good health as we work through this serious contagious disease.

Regards,

Subir Grewal, CFA, CFP Louis Berger