We rarely deliver a mid-quarter email, but the last two days of large drops in the equities markets and recent conversations with clients have prompted us to provide this update.

On Friday, the Dow Jones Industrial Average dropped 666 points (2.6%), which was followed by a 1,175 point drop (4.6%) today.

The S&P500 (a far broader index of stocks) dropped 60 points (2.1%) on Friday, followed by a 113 point drop (4.1%) today.

Intra-day action was even more extreme, with the market down over 6% mid-day today (almost 1600 points on the Dow).

These drops have brought us 1% below where the market was at the beginning of the year and below where broad markets traded when the tax bill was passed in December.

Though these are large point drops, they are not particularly extreme when seen in percentage terms. 4% one-day drops are relatively frequent, occurring every several years, the last one was in 2011. The Dow has dropped by over 7% on 20 separate occasion, four of those drops occurred in 2008 alone.

In its 95 year history, the S&P 500 (which includes a far larger group of stocks) has dropped by more than 5% on at least 20 separate days. Today’s drop, though severe, did not make it into that list.

Viewed in a broader perspective, these drops are severe, but not extreme.

That said, as we cautioned in our annual outlook, stocks remain at historically high levels with various indicators suggesting headwinds for businesses and stock market investors. Stock market valuations are at cyclical peaks. The US economy has been expanding for 9 years, making this one of the longest booms in history. Job growth has slowed over the past year, signalling some economic cooling, though unemployment remains very low and corporate earnings are strong. Underlying economic conditions are still robust, but elevated valuations remain a concern.

In our view, the recent skittishness in equities markets is driven mostly by interest rates. Interest rates on long dated bonds (10-30Y) have continued to climb. The 10Y treasury yield in particular has risen sharply this year. These long-term rates drive key economic decisions and are one of the indicators we watch closely. The 10Y rate is used to price most mortgages, and many companies use 5-10 year rates to evaluate the costs/benefits of projects and investments. Rising rates increase costs for home-buyers and all long-term investments, reducing activity in these sectors. Rising rates also impact disposable income for investors who carry credit card balances (which are at an all time high), and for investors who trade on margin (margin balances are also at an all time high). Most importantly, rising rates impact corporate earnings. US corporate debt stands at almost $9 Trillion. Not all of it is held by public companies, and rates on most corporate debt is pre-set for a period of years. Still, every 1% rise in interest rates translates into tens of billions in additional interest expense for corporations, reducing corporate profits.

Though today saw a large drop in longer-term rates as investors rushed to the safety of Treasuries, we believe this is temporary and rates will continue to rise in the near term. The Fed will continue to unwind its bloated balance sheet to the tune of $30 billion a month, providing a source of supply for skittish equities investors retreating to bonds.

Overall, higher interest rates act as a brake on economic activity. It is this anticipation of higher interest rates and an end to the Fed’s unprecedented policy of quantitative easing that is driving the stock market declines.

We reiterate our year-end advice. Investors should adopt a cautious allocation and be aware of the headwinds we face.

Please give us a call at 646-450-9772 if you would like to discuss your specific circumstances.

Regards,

Subir Grewal, CFA, CFP Louis Berger

2018 Economic Themes: Machines, Bitcoins, Space and Technology.

We trust you’ve had a wonderful holiday season and a good start to the New Year.

As we dig ourselves out from one of the first winter storms and a biting cold front, we have been considering the year ahead and what it may bring for investors. 2017 ended with a remarkable rally in December. This was fueled by the passage of a tax bill that generally favors investors and corporations. Though this tax-bill may have provided some short-term boost to the markets, we believe it’s long term impact will be quite mixed. The bill is estimated to create an unfunded deficit of approximately $1.5 Trillion. This amount of deficit spending would generally give rise to fears of inflation, which seem to have been largely ignored. We are also skeptical about the claim that the bill simplifies the tax code significantly. It is true that a larger proportion of individual filers will now claim the standard deduction, but there are several other complexities introduced by the bill for both individual and business filers which will be argued over by tax accountants for years.

In many other countries, the tax authorities prepare a return/statement at the end of the year for tax-filers which can then be contested/corrected. No such mechanism for low/middle-income Americans is anticipated in this bill. We are also skeptical about claims that the corporate tax cuts embedded in this bill will spur investment or boost anemic wage growth. Corporations are already holding record cash reserves, and wage growth in the US has been slow for decades, largely due to the legislature’s failure to increase the minimum wage. As such, we believe the tax bill will have a limited impact on medium-term prospects. Given our view on the 2018 mid-terms, there is a good chance many provisions will be reversed within a year.

2018 Economic Themes: Machines, Bitcoins, Space and Technology.

Slow But Steady Rate Rise. The Fed has signaled no intention to halt its program of bond sales and interest rate hikes. Over $400 billion worth of the Fed’s Treasury bond holdings will come due in 2018. The normalization program announced in 2015 suggests the Fed will not reinvest most of the principal. Many billions in principal repayments on the Fed’s MBS (mortgage-backed securities) holdings will also not be reinvested. In aggregate, we expect the Fed’s normalization actions will withdraw $300-$400 Billion from money supply in 2018. We expect the Fed to maintain the normalization plan and continue tightening rates in 2018 with the Fed Funds rate ending the year in the 2%-2.5% range. Both these actions will place additional pressure on stocks.

Year of the Donkey. We expect the mid-year election of 2018 to mark a sharp reversal for Republicans, who currently control all three branches of federal government. We expect the Democratic party to win a majority in the House of Representatives and we suspect there is a real possibility (40%) they will take the Senate as well. Such a result would stall or reverse the Trump administration’s legislative agenda. We expect congressional investigations of the administration to intensify as a result.

The Bull Runs Out of Steam. We expect 2018 to be a difficult year for equities markets given the extremely high levels attained over the past two years. Margin debt is now at all time highs, at 1.6 times the peak reached in 2007. We have been advising caution for the past few years while the market has continued to rise. However, we see no reason to change our short/medium term forecast given stretched valuations and the age of this bull market (now entering its 9th year).

Rise of the Machines. 2017 saw various automation/AI technologies gain a firm foothold among consumers. Siri, Alexa, Google Home and several voice activated car-technologies have become second nature to millions of people. We believe this trend will continue in 2018 and we will see the initial emergence of voice-activated AI/automation being married with robots/machinery. This has already begun in cars, but we expect intelligent home devices to begin controlling autonomous vacuum cleaners, window washing drones and other small devices. As we did in 2017, we expect AI/Automation stocks to outperform consumer discretionary stocks.

International Beats Domestic. We expect international stocks, especially European markets, to outperform the US in 2018. Emerging market fundamentals remain broadly positive, and we expect these markets to perform reasonably well while we are expecting a negative year in the US.

Bitcoin Bust. 2017 saw immense interest in crypto-currencies, particularly Bitcoin. Prices were driven up by sky-high demand and fixed supply (the total amount of Bitcoins in circulation increases only by a very small percentage each year). The sharp rise was partially fueled by speculation around new ETFs that seek to track Bitcoin prices and open up the market to more traditional investors. We believe some of the technologies embedded in Bitcoin, especially the peer-to-peer transactions and public ledger/blockchain, are innovative and do have a future. That said, Bitcoin prices themselves are in a speculative bubble which we expect will reset in 2018.

Renewables Redux. 2017 saw renewable energy YieldCos outperform conventional fossil-fuel based electric utilities. We expect this trend to continue through 2018 as YieldCos will benefit from robust demand for renewably sourced electricity (by both the public and private sectors), increased efficiency from solar and wind power, newer fleets that require less maintenance and a smaller scale that allow them to operate more nimbly compared to their conventional peers.

Organics Go Mainstream. Organic food products are the fastest growing segment of the US food industry. Sales have increased by high single digits in recent years while the overall food market has remained stagnant. Though some of the major food behemoths have launched their own organic food lines or acquired smaller start-ups, they continue to play catch-up in this arena. We think organic food stocks will outperform conventional food stocks this year.

New Dawn of Space Race. 2018 will see a number of commercial space ventures mark milestones, including manned-flight into low-earth orbit and potentially a lunar orbital space tourism mission. As commercial space missions become routine and the prospect of mining asteroids and the moon becomes a reality, we expect a secular rethinking of the prospects for natural resource mining enterprises that are earth-bound. The trend itself will take a couple of decades to reach fruition, but we expect earth-side mining for certain materials to decline over time in favor of extraction in space. We realize this sounds far-fetched, but technological changes over 20 year cycles can be immense (for example, compare internet ubiquity with where we were in 1997). The technology to permit the creation of largely automated mines on the moon or an asteroid are largely available today.

Net Neutrality Fallout. Though the revision of net neutrality rules was overshadowed by the tax bill negotiations, it was a landmark change. We expect to see tangible impact to the way consumers experience the internet as a result of the FCC’s contentious decision to remove net neutrality. This reversal tilts the playing field towards telecommunications companies and away from content providers. We expect telecommunications firms will seek to exploit the ability to meter bandwidth and extract rents from content providers. ISPs will start to create fast lanes and we may see some of the large content firms seek to create their own networks. Telecommunications firms have risen in the past month as a result of this ruling, but we believe the medium and longer term prognosis is less rosy, with the prospect of new entrants and even more consumer dissatisfaction.

2017 was an uneven year for our market predictions. We were right on five calls, half right on one call and wrong on four calls. Continued bullishness and investor support for the Trump administration (despite abysmal poll numbers) torpedoed three of our calls.

? Fed stays the course: We expect the Federal Reserve will continue to raise rates as stated. We expect the Fed-Funds rate to rise above 1.5% over the course of 2017. The Fed started 2017 with a target interest rate of 0.50%-0.75% and finished the year with a target rate of 1.25%-1.50%. While the Fed raised rates, they met but did not exceed 1.50%, so we’re giving ourselves half a point on this one.

× Equities Caution: We continue to advocate for a cautious allocation to stocks and expect to see negative returns for US equities this year. We were dead wrong on this call as US equities continued their bull market run through year eight.

? Artificial Intelligence: We expect performance for companies providing intelligence features in devices to outpace the consumer durables index over the next three years, we will evaluate ourselves annually on this call. Artificial Intelligence-related companies had a very strong 2017 as the Global Robotics and Artificial Intelligence Index was up 57.62%. Comparatively, the S&P 600 Consumer Discretionary Index was up 17.13%.

? Continental shifts: Over the next several years, we expect Indian markets to outperform those in China and the developed world. We were right on year one of this call. The S&P BMI India Index was up 29.56% in 2017. This compares to 26.67% return for the S&P Greater China Index and 21.83% return for the S&P 500 Index.

× European upheavals: We believe European stocks to be more attractively priced than US equities…we expect European stocks to outperform US equities. While European stocks performed in-line with our expectations — S&P 350 Europe Index was up 10.75% on the year — the unexpectedly strong performance of US stocks (21.83% return for the S&P 500 Index) easily outperformed this total.

× Dollar strength continues: We expect the dollar to remain strong against major currencies worldwide. Despite rising interest rates, the USD weakened against a basket of international currencies in 2017.

? Drones are going to be delivering much more than bombs: We expect companies building these technologies to outperform the freight and shipping transportation companies. While we view this as a long term trend, 2017 saw drone-related companies outperform. The Solactive Robotics and Drones Index was up 38.7% while the S&P 500 Transportation Index was up 23.52%.

? Renewable Utilities: Though the incoming administration is not supportive of renewables, we think renewable utility companies or YieldCos will outperform conventional, fossil-fuel based utility stocks. YieldCos saw a strong rebound in 2017 and handily outperformed traditional utilities. The Global YieldCo Index saw returns of 22.87% while the S&P 1500 Utilities Index returned 12.16%.

? Retail Real-Estate: We expect real estate companies that own large portfolios of malls and brick and mortar stores to underperform other real estate investments. This prediction came to fruition as brick and mortar stores, and particularly malls, continued to see a decline in foot traffic and a loss of market share to online shopping in 2017. The FTSE NAREIT Regional Malls Index was -2.68% and the FTSE NAREIT Shopping Centers Index was -11.37%. Meanwhile, the FTSE NAREIT Composite was up 9.29%.

× Optimism about Trump presidency short-lived: We expect any investor-optimism surrounding the Trump presidency to evaporate rather quickly in 2017 as markets find he is unable to follow through on his lofty campaign promises. As we expected, President Trump has been unable to follow through on his campaign promises, and his approval ratings are among the lowest ever recorded for a first year presidency. However, a strong economy, robust corporate profits and the prospect of a tax cut allowed investors to shrug off his policy failures, chaotic management style and a criminal investigation to send equity markets to all-time highs.

We trust you’ve had a restful and enjoyable summer.

This was a difficult hurricane season for many of our fellow Americans, especially those in Puerto Rico and across the South. A number of category 4 and 5 hurricanes made landfall in the US, causing enormous damage in Puerto Rico, Houston, Florida and the Virgin Islands. Several Caribbean islands have suffered almost complete devastation. Aside from the enormous human toll exacted by the loss of lives and homes, the hurricanes have also impacted US industry. Several sectors were impacted, including tourism, oil and pharmaceuticals (Puerto Rico is home to several pharmaceutical plants). Many hourly workers missed work for days or weeks, affecting their earnings. The impact is visible in the September jobs report, which shows a loss of 33,000 jobs.

This loss breaks a consecutive streak of 83 months of employment gains, stretching back to 2010. Markets largely shrugged off the terrible jobs report due to these effects, which are believed to be temporary. We expect October’s report will be skewed in the other direction as many workers head back to work.

Taking a longer term view, it seems clear that man-made climate change leads to warmer ocean and air temperatures. These conditions produce larger, more destructive storms which arrive with greater regularity. In the West, we have seen a series of destructive forest fires this year. Climate change has also expanded the range of invasive insect species which have killed off large stands of trees in our forests. Under hot, drought conditions brought on by global warming, these dead trees become kindling for forest fires. Our changing climate will pose major issues for insurers/re-insurers and local governments, particularly in flood and drought-prone areas. Communities will have to review zoning regulations in the face of these fires and storms. The cost of adaptation and recovery will be high, and doubtless some communities will be unable to recover fully.

The Fed has signaled it will treat the September jobs report as an outlier and stick with its plan to normalize monetary policy. This is almost certain to include one more interest rate hike before year end, likely in December. The Fed has also indicated it will proceed with its plan to reduce its 4.5 Trillion dollar holdings in bonds. These were purchased between 2008 and 2014 as part of the “quantitative easing” program, in an effort to stabilize financial markets. Based on its published plans, we expect the balance sheet to shrink by 250 Billion in 2018 and up to 400 Billion in 2019 and subsequent years, depending on economic conditions. These are substantial numbers, and we expect them to maintain steady upward pressure on interest rates across the maturity curve. We expect Janet Yellen will be replaced as Fed Chair when her term ends at the end of Jan 2018. This raises critical questions about the Trump administration’s ability to nominate and confirm a candidate who is credible and seen as independent of political pressure.

Stock markets continued their upwards drift, hitting new highs this quarter. These moves were supported by steady economic numbers, including GDP and employment. Corporate earnings have also remained steady, though insurance sector earnings are expected to be down significantly in the third quarter. Gains have been led by the technology and financial services sectors, which have grown to become the largest components in the S&P500. Both sectors are cyclical, and in our view a long expansion and the increasing ubiquity of technology has driven some of these stocks to unsustainable levels.

The market seems to have largely ignored Washington, tuning out several dramatic weeks in Congress as major legislation to transform health-care, infrastructure and deregulation have stalled or collapsed. A Republican effort to pass a tax reform bill is still underway, but it looks increasingly unlikely that this effort will pass either. The tax reform package proposed has not been scored by the CBO, but most analysis indicates it will add to the deficit. The proposal includes several modifications to deductions and tax brackets. Overall, its impact would be to reduce the tax burden on the very wealthiest of Americans, and shift some of those charges on the poorest and on Americans earning less than 400k a year. The scale of the proposal, the major uncertainties involved, and the haphazard manner in which it was developed lower the chances of passage. We do not believe the tax reform proposal will be enacted in its current form. At best, we believe the administration may be able to pass a severely watered-down bill.

Looking ahead to the end of the year, we expect equities markets to largely ignore Washington DC, unless the administration managers to pass significant legislation. The prospect of interest rate hikes and the Fed’s plans to shrink its balance sheet are likely to exert downward pressure on stocks. We continue to maintain our defensive positioning, with lower than average allocations to higher-risk assets like stocks and long-term or high-yield bonds.

The 2nd quarter saw the Fed continue its strategy of withdrawing stimulus from the US economy. Since December 2016, the Fed has raised rates three times, bringing the target rate up to 1.25%. Their most recent statements suggest the target rate will continue to rise if unemployment and inflation stay relatively stable. There have been several statements this month from Fed governors indicating the central bank plans to begin selling or rolling off the 3.6 Trillion dollars in bonds it has acquired since the financial crisis of 2008/2009. The Fed’s decision to increase its bond holdings by 400% during the financial crisis was an unprecedented action, and the reduction to more normal levels has been expected for some time.

The net effect of these moves for investors will be a rise in interest rates, a reduction in liquidity, and a less attractive environment for risky assets. Bond investors should see rates continue to rise towards more normal levels, a relief since bond yields have been historically low for the past several years. The sale of the Fed’s bond portfolio will also reduce the amount of money in circulation (the money supply) as private investors purchase the assets the Fed sells. This is expected to put further pressure on stock prices and riskier assets as funds are directed into these purchases.

Over the past few days, we have also seen the risk of political instability in the US rise to remarkable levels. It seems increasingly likely that the various investigations underway may lead to very senior members of the Trump administration and campaign facing a variety of charges.

From a valuation perspective, stock prices continue to look overvalued. Remarkably, the top five components of the S&P 500 (Apple, Alphabet/Google, Microsoft, Facebook and Amazon) are all technology companies. What’s even more surprising is that with the exception of Apple, they are all trading at prices over 30 times earnings. Much of that gain has been recent, four of the five have seen gains of over 20% in the past six months (the exception is Microsoft). Taken together, these five companies represent almost 12.5% of the index.

Overall market valuations are extraordinarily high, with the current P/E ratio for the S&P500 over 25. A longer term measure, which looks back at ten years of earnings (Cyclically Adusted or Shiller P/E) is illustrated in the chart below, alongside interest rates. Cyclically Adjusted P/E is at levels that have only been exceeded twice; before the tech-wreck of 2000 and Black Tuesday in 1929. This is partly because interest rates remain at historic lows. As discussed above, that is changing.

As a result of these factors, we continue to maintain a defensive posture and recommend clients an underweight allocation to high-risk assets.

Data source: Robert Shiller – Yale University

We would like to use the rest of our quarterly letter to discuss a longer-term risk, one that impacts not just the markets, but all of human civilization.

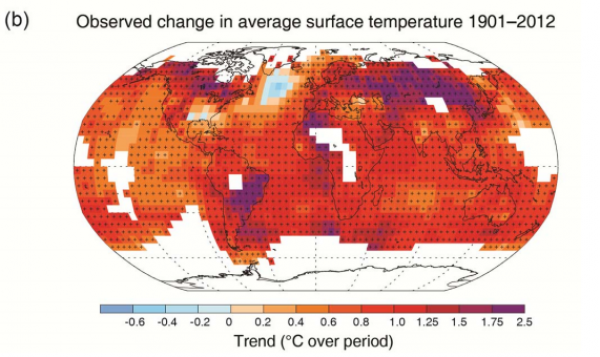

For several decades now, scientists focused on studying global warming and climate change have shared their increasingly dire findings about the impact of human activity on the Earth’s biosphere. It is now abundantly clear to all, except the intentionally obtuse and dishonest among us, that human activity has impacted the Earth’s climate in a significant way. Our species’ use of fossil fuels has released an extraordinary amount of greenhouse gases into the atmosphere, raising the average temperature across the world by 0.2° Celsius (0.36° Fahrenheit) each decade.

Economists have long understood that markets can mis-price public goods or services that have concentrated benefits for a few while costs are diluted among many. Within the economic literature, this is called the “tragedy of the commons”. The classic example is shepherds grazing their flocks in a meadow that is commonly owned. In standard political and economic theory, the government is meant to intervene to enforce a solution that furthers the general good and recognizes and allocates the true costs of such activity.

At this point, we should admit that US political institutions have failed to deliver on addressing climate change. The vast majority (85%) of greenhouse gases released into the atmosphere have been generated since World War II. Over that period, the United States has been, by far, the largest greenhouse gas emitter. So, much of the responsibility for climate change lies with us. Yet, we have been for decades, and still remain, the chief impediment to decisive action on climate change. The Trump administration has made a very bad situation even more dire by announcing a withdrawal from the Paris agreement.

Nature, of course, couldn’t be less concerned about human politics. The content of greenhouse gases like carbon dioxide and methane has continued to rise, driving surface temperatures higher. This has manifested itself in a variety of ways. Glaciers have retreated across the world. The five hottest years in recorded history occurred within this decade, and 2016 set a new record. Coral reefs across the world are bleaching as water temperatures rise, stressing the marine eco-system. Hotter summers are impacting humans as well, with extreme temperatures rising causing heat-strokes, dehydration and deaths.

Most climate change models have assumed a 0.2°C increase per year in surface temperatures will leave the Earth’s with an average temperature 2°C (3.6°F) higher by 2100. Those assumptions now look woefully inadequate. Since we have not measurably reduced our greenhouse gas emissions, and the Paris agreements seem to have collapsed, 2°C degrees is an underestimate and the case for a 3-4°C rise becomes stronger.

As climate change and research into it has advanced, the risks of a runaway feedback loop have become clearer as well. Permanently frozen ground in the arctic regions of Asia and North America traps a large amount of methane. As the ground gets warmer, this methane leaches into the atmosphere. As temperatures rise and water becomes scarce, plant life across the world will be stressed. The risk and incidence of forest fires increases, and the loss of trees leaves more CO2 in the atmosphere. If rising temperatures, fire and drought impact major CO2 sinks like the Amazon forest, temperatures will rise even faster.

There is a reasonable likelihood that temperatures will have risen by 4-6°C (7-10°F) by 2100. 90°F days will be 100°F days. 100°F days will be 110°F days. Phoenix saw temperatures rise above 118°F last month, grounding flights. What happens when temperatures approach 128°F? If such an extreme rise in temperatures were to occur, the world is looking at a series of major catastrophies that could largely destroy human civilization.

Drought and heat would cause widespread human suffering and deaths. Food stocks would be harder to grow with much of the world’s breadbasket regions in China, India, Central Asia and North America undergoing desertification. Much of the southwestern United States could become an uninhabitable desert. Tens of millions of people would need to be resettled. This pattern would be replicated across the world. A NASA study indicates the Middle East is suffering through a 20 year drought that is more severe than any in the past 900 years. There are indications that crop failure and rising food prices have contributed to societal upheaval in the region. The Mediterranean as a whole is susceptible to drought and desertification.

The impact on agriculture worldwide would be many times more severe than seen during the dust-bowl. Marine life and fisheries would be devastated as ocean temperatures rise. And yes, sea-levels could rise 10 feet or more, making most coastal cities uninhabitable without civil works on a scale we have never seen before. Much of New York, London, Mumbai, Shanghai, Sydney, Rio De Janeiro, Singapore, Dubai, Miami, almost all of Bangladesh, and many island nations, would be lost.

It is virtually certain that such extreme conditions will lead to widespread forced migrations and fuel conflict between nations and individuals. This is one of the reasons the US Department of Defense treats climate change as the largest strategic threat to the country. Governments and political structures will undergo immense stress and opportunistic charlatans could come to power across the world.

All of this would significantly impact incomes, growth rates, earnings and most importantly health and well-being. We do not intentionally seek to be alarmist. However, the data and projections we have seen demand urgent responses and are alarming. There is a grave likelihood that we leave our children with a world in crisis. Without urgent, concerted action, large portions of our planet will become inhospitable to human inhabitation within our children’s lifetime.

Clearly, these events will impact investors and markets in profound ways. As we engage in long-term, inter-generational planning for clients, we want our clients to know that we take these risks very seriously and will continue to keep these considerations in mind.

The first quarter of 2017 was full of eventful news for markets. We saw a Fed rate hike, record low unemployment rates, all time highs for US equity markets and a new administration sworn in, with Republicans now in full control of Congress. In our view, this likely marks an inflection point for the current business cycle and market levels.

Since the election, we have received several queries from our socially responsible investors about the fate of environmental and climate change regulation under the Trump administration. We understand and share many of their concerns. We hasten to add, however, that infrastructure spending and projects are usually undertaken with long time frames in mind. Enterprises making decisions about what kind of power plants to build will consider the costs over a long term. They are well aware that the current administration and its policies are not set in stone.

We do not expect a raft of coal plants to be built over the next four years — in fact, 2017 has seen an acceleration of the closure of several legacy coal plants. Large plants typically take 3-5 years to build and operators have to factor in the possibility that they will face a changed regulatory environment just as the plants come online. Natural gas prices are likely to play a much larger role in determining what resource mix generates our electricity. The cost of utility scale renewable solar power continues to fall, and though it is not yet competitive with cheap gas, it is not far off either. The IEA estimated the average capital costs of photovoltaic solar plants under construction to be 35-45% higher than natural gas plants per unit of energy produced. An array of tax credits make solar competitive with gas. though the precise economics are driven by regional factors and weather. Wind and hydroelectric power are already competitive with natural gas.

At the risk of appearing sanguine, we think that technological advances, consumer preferences, and the economics of scale have brought us to the point where renewable energy will be competitive with conventional electricity generation going forward. Installed renewable capacity will continue to increase, with or without incentives. If fuel costs move higher, renewables will be become very attractive.

In our view, purchasing certain sectors based on the administration’s stated policy preferences is unlikely to lead to consistent gains. Our reasoning is based on the Trump administration’s penchant for changing direction at the drop of a hat, and secondly on the opposition to various aspects of their policy agenda from either side of the aisle in Congress. In the medium and long-term, valuations and the business cycle will determine investor success. Neither looks particularly fortuitous at the moment for risk assets (equities, or long-term/lower-quality bonds). We continue to recommend a defensive shift for clients based on these factors.

We hope you have had a good start to the New Year and wish you the best for 2017. As always, in our first letter of the year we have attached a review our 2016 investment themes and a list of our investment themes for 2017.

The fourth quarter of 2016 revolved around politics, with a focus on the US presidential election. In Jan 2016, we wrote there was a “strong possibility one or both major party nominees will be from outside the establishment mainstream”. In retrospect, that looks like an understatement. A series of unusual news stories and the eventual surprising result of the US presidential election led to sharp drops in US equities in early November. Markets recovered quickly and ended the year close to or at their highs. In some ways this is a relief rally, driven by the realization that much of the Republican establishment will support the Trump administration and vice-versa.

The political upheavals of the past few months have not changed the underlying economic realities confronting investors. We are likely at the tail end of a bull-market that is almost 8 years old, and several risks loom on the horizon. Interest rates in the US will continue to rise as the Fed attempts to normalize historically low borrowing rates. This will modify the calculus for investors as interest bearing assets become attractive and rising rates impact the denominator in equity valuations.

The results of the US election have created enormous uncertainty about the US’s future economic policies, particularly with respect to trade. We believe that workers’ concerns about economic insecurity do require political solutions. We are not, however, convinced that protectionist barriers are the answer to job-losses in the US manufacturing sector (the last US experiment with high tariffs, 1930’s Smoot-Hawley Act, likely exacerbated the effects of the Great Depression). Nor do we believe it is in the US’s long-term interests to loosen environmental rules. The incoming administration seems bent on trying or threatening one or both of these approaches.

Roughly 50% of sales for S&P500 companies occur overseas. This underscores the global nature of the world we live in, and the degree to which US businesses rely on foreign operations. The prospect of a full-fledged trade war with major regions or countries should worry investors deeply. Though some investors may have been emboldened by the November/December recovery, we would advise caution given the significant headwinds and uncertainties facing us.

Fed stays the course: We expect the Federal Reserve will continue to raise rates as stated. We expect the Fed-Funds rate to rise above 1.5% over the course of 2017.

Equities Caution: We continue to be cautious on US equities, as we have been for the past several years. S&P 500 is priced at over 25 times last-year’s earnings. Even if we use projections that forecast a recovery in energy sector prices, P/E ratios are over 20. Rising rates erode support for outsized price-earnings ratios. We are also in the eighth year of a long bull market with a number of credit related issues in markets across the world. We continue to advocate for a cautious allocation to stocks and expect to see negative returns for US equities this year.

Artificial Intelligence: Technology continues to come at us hard and fast, but the groundwork has been around for decades. We recall using voice-recognition software to dictate texts almost 20 years ago. It was slow and cumbersome. Modern voice recognition is vastly improved by faster hardware and refined software. When coupled with the ability to search for information and issue instructions to connected devices, this technology can seem very much like science fiction, evoking both fears and dreams. Yet, asking Alexa to lower your blinds is in essence no different than using “the clapper” to turn on the lights. We expect this to be the year that voice activated instructions come to various devices, including cars and household appliances. Companies with effective voice activated solutions will find themselves partnering with manufacturers of all sorts of devices, not simply computer and phone makers. The revenue and earnings implications are less clear. Licensing fees may not amount to much and a large part of the value for technology companies may derive from sales of media and in Amazon’s case, all sorts of goods. We expect performance for companies providing intelligence features in devices to outpace the consumer durables index over the next three years, we will evaluate ourselves annually on this call.

Continental shifts: For much of human history Asia has been the center of the global economy. That changed in the centuries following the European industrial revolution and colonial expansion. Over the past thirty years, rapid growth in China has brought gross East/South Asian annual GDP (ex-Russia) to roughly 25 Trillion USD. This exceeds both that of North America and Europe/Central Asia, both around 20 Trillion USD. The big laggard in Asia has been India, where per capita GDP is 20% that of China. We expect India’s growth rate to exceed that of China’s for the next several years, with the relative difference in per capita GDP falling. Despite the numerous hurdles to doing business in India, we expect investors will begin to pay more attention to companies with exposure to India and an India related strategy. Over the next several years, we expect Indian markets to outperform those in China and the developed world.

European upheavals: This will be a busy year of European politics, there are major elections in France and Germany. Looming over it all is last year’s British decision to exit the Europe zone. Any or all of these have the capacity to inject more policy uncertainty and create market upheavals. Though we believe European stocks to be more attractively priced than US equities, these concerns give us pause. Nevertheless, we expect European stocks to outperform US equities.

Dollar strength continues: We expect the dollar to remain strong against major currencies worldwide. This impacts the returns dollar-based investors can expect to realize from foreign investments.

Drones are going to be delivering much more than bombs: Many of us have been concerned about the impact of automated weapons on conflicts across the world. This technology raises numerous difficult ethical questions, alongside legal dilemmas. Less attention has been paid to the revolution soon to overtake transport and delivery services of every form. Remote operations and autonomous guiding systems are approaching the point where not just driverless cars, but pilot-less planes, captain-less ships and person-less food delivery are about to become a reality. These technologies are going to create immense disruptions for various work-forces across the aviation, shipping and transport sectors. As with so many other technologies, the armaments industry has led the way. But the long-term impacts on our economy, politics and lives will be driven by the commercial applications of these technologies. We expect companies building these technologies to outperform the freight and shipping transportation companies.

Renewable Utilities: Though the incoming administration is not supportive of renewables, we think renewable utility companies or YieldCos will outperform conventional, fossil-fuel based utility stocks. Despite a high likelihood of loosening EPA standards, we think YieldCos benefit from a newer fleet of power plants and stock prices that haven’t recovered much from the energy crash of 2014/15.

Retail Real-Estate: We believe the retail real estate sector will come under pressure from rising interest rates and a secular shift towards online purchases. We expect real estate companies that own large portfolios of malls and brick and mortar stores to underperform other real estate investments.

Optimism about Trump presidency short-lived: We expect any investor-optimism surrounding the Trump presidency to evaporate rather quickly in 2017 as markets find he is unable to follow through on his lofty campaign promises.

This was a difficult year for our prognostications. We were wrong (or early) on core calls including rising interest rates and an equities bear market, that undercut many other themes that relied on those predictions. Our score was 3.5 out of 10.

×Fed stays the course: We expect short term rates to rise by 1% over 2016, and believe long-term rate rises will be roughly commensurate. We believe the Fed’s board will stick with their stated intentions, it would require dramatic events to make them change course during an election year. As we expected, the Fed was cautious in an election year. Our expectation that the board of governors would vote for a series of quick rises early in the year was wrong, the Fed chose inaction during the election year.

×A return to risk: We believe risk concerns will weigh on markets all year… US equities markets will be down for the year, with a strong possibility that we see a decline of 20% or more over the course of the year. Broader US equity markets ended up 10% for the year, and though the S&P 500 saw a decline of over 11% earlier in the year, this wasn’t as much as we were looking for.

?Oil is red: We expect oil prices to continue to be weak in 2016, oil is likely to see the $20-25 range… Oil bottomed at $26 a barrel and remained below $50 for most of the year, a big departure from the $100 prices in 2014.

?Emerging markets comeback: We believe smaller emerging market equities will outperform developed markets in North America and Europe which we expect to be stuck in the doldrums during 2016… With total returns of 8.58%, the MSCI Emerging Markets index outperformed most developed markets, except the US (where returns were in the double digits).

?A Tech-wreck redux: Technology companies have been among the strongest performers over the past few years… However, extremely optimistic valuations for unproven business models have become the norm and we believe the inevitable reckoning is quite likely to occur this year. High profile stocks such as Twitter and LinkedIn suffered large declines this year (LinkedIn was eventually sold), and the Nasdaq composite (7.50%) underperformed the broader S&P500 (11.96%). That said, the broader decline for technology stocks we were expecting did not materialize.

×Commodity economies fumble: Australia and Canada were both spared the worst of the global financial crisis… We believe both will be among the worst performing markets in 2016. Though the Australian market had relatively moderate performance in 2016 (the ASX rose roughly 5%), the Canadian market was one of the best performers (with the TSX up almost 15%).

?The greenback still rules: We expect upheaval in a number of markets to drive a flight to safety and support USD through 2016. We believe the dollar continues to remain strong in 2016 against Euro and other major currencies. We were right on this call, the dollar has gained over the course of the year, against both the Euro and other major currencies.

×Renewables: We are long-term believers in the prospects of the renewable energy industry and the recently concluded Paris accords should support prices in the sector…We expect renewables to continue outperforming their conventional energy counterparts. We were wrong on this one. Renewable energy companies had moderate to flat performance, with the Nasdaq Clean Edge index ending the year down over 4%, while the S&P Energy index was up over 20% for the year.

?Presidential election: 2016 is a US presidential election year and an unusual one to boot. We believe the sentiment favors non-traditional candidates who reject the status-quo. There is a strong possibility one or both major party nominees will be from outside the establishment mainstream. In part this reflects a broad decline in deference to the governing class after the financial crisis of 2008 and the decade that preceded it. Recent European elections in France, Hungary and Greece have reflected similar sentiments. If as we suspect, a candidate opposed to the status-quo ends up on a major party ticket, this will create additional uncertainty weighing on markets in 2016. We were right on this call. We thought there was a high likelihood that one of the nominees would be from outside mainstream US politics. We believe there was a low likelihood that a non-traditional candidate would win the election. That outlier scenario was realized.

×Unemployment Rises: We expect headline unemployment in the US to end the year above 5%. The softening in global demand, rising rates (however slight) and lackluster earnings we expect will also impact employment within the US. This is in keeping with our expectations of an economic downturn during 2016. We were wrong on this call, we ended 2016 with unemployment at 4.7%.

India’s demonetization: it’s like pixie-dust for bank balance-sheets

Many motives have been advanced for the great Indian demonetization of 2016. These include reducing the informal/untaxed “black-money” economy, removing counterfeit notes from circulation, making terrorist financing more difficult etc. Might there be another, unstated, reason apparent to central bank watchers? A subtle subterfuge to reduce the perceived level of non-performing assets (NPAs) at Indian banks.

By March 2016, Indian banks held 6 Trillion rupees (or 6 lakh crore) in NPAs. This amounted to 7.6% of their aggregate balance sheets as outlined by the RBI in its June 2016 financial stability report, up from 5.1% over six months. That large jump was the result of an Asset Quality Review initiated by the RBI. Indian banks had been using various devices to avoid classifying bad debts as NPAs. The RBI’s re-classification tore down this hall of mirrors. The RBI also projected NPAs could rise to 8.5% by March 2017.

Within two months, Raghuram Rajan had been removed from his post by the present Indian government. Eight weeks after that, Prime Minister Modi announced the shock demonetization of existing Rs. 500 and Rs. 1,000 notes.

Since then, 90% of the demonetized currency notes (14 Trillion rupees) have been deposited into the system. We can reasonably assume the bulk of these funds have remained in the banking system since withdrawal limits are in effect and large cash transactions are being discouraged.

If the denominator for NPA ratios has indeed risen from 79 Trillion rupees to 93 Trillion rupees. gross NPA ratios would fall to 6.4%. Just like that, we have a seemingly magical improvement in the credit quality of bank balance sheets.

Who knew a “digital economy” would have such fringe benefits?

First, we think a Trump victory is quite unlikely. That said, the probability is not zero, it’s likely to be around 15-25%. We routinely analyze even less likely events and their impact on markets, so we have considered the reaction of markets if Mr. Trump were to win the general election.

There will be almost no place to hide from the initial volatility after an unexpected Trump victory. We expect significant turmoil in the financial markets and we believe that in the short-term (days/weeks) there will be few safe havens. Mr. Trump’s economic policies are so unconventional, and his temperament so mercurial, that we expect almost all sectors and asset classes to be somewhat affected by negative uncertainty. Precious metals may be the only asset that benefits from a flight to safety.

Bonds have traditionally served as a safe haven in times of turmoil. We believe bond investors should not remain sanguine if Mr. Trump does win the presidency. As a leveraged developer, Mr. Trump has had a colorful and combative history with lenders. His natural bluster has been intermittently aimed at bond markets during this campaign and the prospect of a Trump administration in control of the US Treasury is bound to spook bond investors. He has suggested he would unilaterally default on US sovereign debt (arguably not a novel position since the Republican congress toyed with a similar position in 2011) and seek to renegotiate principal amounts.

Mr. Trump has made combative comments about the Federal Reserve and its current policies. He has also expressed dissatisfaction with the current low interest rate regime. Taken together, these sharp, unusual policy views create immense uncertainty about how Mr. Trump would manage the credit and repayment of US debt, the government’s relationship with the Fed, and other issues of concern to the broader credit markets. We expect FX markets to exhibit a flight to perceived safety which historically has benefited the Swiss Franc and Japanese Yen. Uncertainty about bonds and rates will also hit real assets heavily dependent on credit markets. We do not expect real-estate to do well.

When it comes to stocks, we expect broad declines in the short term, but some sectors will be harder hit than others. The banking and financial sector is likely to see a steep decline in market sentiment and levels. Mr. Trump has made several negative statements about banks and their business models. Banks are also naturally leveraged and very sensitive to market sentiment. None of this augurs well for the banking or financial sectors.

Given Mr. Trump’s combative stance on trade and trade agreements, we would expect sectors dependent on imports/exports in their global supply chain to be battered. This includes consumer discretionary, technology, heavy industry, materials, and depending on precise global footprint, energy companies. In contrast, consumer staples should play their standard defensive role.

The immediate sentiment towards the defense industry is somewhat more uncertain. Mr. Trump has, at times, advocated a combative posture on national security and war matters. In almost direct contradiction, he has also proclaimed he would reduce the defense budget and the number of military bases overseas in line with his “America First” pledge. Defense contractors dependent on Pentagon contracts for services to troops overseas are likely to see sentiment and stock prices decline. Large defense manufacturers should decline as well since Mr. Trump has expressed skepticism about some expensive weapons programs (the F-35 in particular). The foreign policy and defense team Mr. Trump puts in place will determine how this plays out in the longer-term.

Beyond the initial few weeks and months, we expect much will depend on the composition of Mr. Trump’s administration and his demeanor during the transition. A prospective Trump administration caught up in balancing spending, debt, legislative priorities and political considerations would normally be constrained. However, Mr. Trump is likely to have a compliant Congress, with Republican legislative majorities and both Senators and Representatives eager to please the new force in American politics. It is impossible to make longer-range forecasts of what a Trump administration’s policies would look like, simply because we do not know his true priorities. We would advise investors to be extremely cautious about bargain-shopping in the immediate aftermath of a Trump victory.

Mr. Trump is unlikely to win the election, but in the event he did, we believe markets will react very poorly, at least initially. He is in many ways, the opposite of a traditional conservative politician, disdaining societal norms and conventional politics. Mr. Trump’s election would engender policy uncertainty on a scale not seen for decades, upending long-range business plans and reducing risk-appetites across the board. We would advise investors to exercise caution in the event Mr. Trump wins.

If a presidential candidate berates the Fed and no one pays attention, do markets still react?

The Federal Reserve chose not to raise rates in September, despite speculation by many participants that they would. The decision went as we expected since the Fed is generally unwilling to move rates this close to a presidential election. As an institution, the Fed is very reluctant to take actions that could be interpreted as favoring one or another party. Absent a genuine crisis (as in 2008), Fed governors will heavily favor inaction in a presidential election year. Inaction in this instance means an expansionary monetary policy with very low rates, and this does indeed benefit the incumbent party. In our view, this is more accidental than deliberate.

For a number of decades, central bankers have walked a fine line. They are political appointees, but their decisions are supposed to be apolitical, and they enjoy a degree of independence not afforded to the heads of other government agencies. Like all senior government officials, Fed governors are politically attuned and they undoubtedly have personal political preferences. In a normal election year, with a more typical slate of candidates, Fed inaction might lead to quiet grumblings within DC circles. But this is not a normal election year.

We have seen Mr. Trump repeatedly attack the Federal Reserve chair, Janet Yellen, in very personal terms for keeping rates low. This has received very little attention among all the other political news and outrageous statements by Mr. Trump in this cycle. As with so many things this year, we cannot say whether or not berating Fed officials will become the political norm.

What we do know is that in most countries, the slightest hint of overt political “interference” in central banking decisions can spook markets. The enormous volatility of the South African Rand over the past year is a case in point. European markets saw similar gyrations during the months leading up to Mario Draghi’s succession of Jean-Claude Trichet.

Though berating the Fed is a small part of Mr. Trump’s political plank, we had to go back to Williams Jennings Bryant’s candidacies of 1896 or 1900 to find an instance where central bankers and monetary policy was dragged into an American political contest in such a way. And that was back when US dollars were backed by gold in a fixed amount. Neither the Nixon administration’s abrogation of the gold standard nor Mr. Volcker’s unremitting steps to control inflation elicited such personal invective. As long as Mr. Trump’s chances of winning the presidency remain slim, the market will remain sanguine. If the prospect of a Trump presidency were to become more likely, we expect the future monetary policy of the US to become an area of immense concern for the markets.

We have discussed interest rates extensively in our previous letters, and would like to briefly turn our attention to debt levels. Extremely high levels of debt were the primary cause of the 2006-2009 financial crisis and generally make for a riskier financial system. Though US households and enterprises continue to reduce debt (deleverage), global debt levels have continued to rise. Looking at World Bank and IMF data, we can see that global private sector credit now exceeds 2008 levels (measured as a percentage of GDP). US private sector debt, at almost two times GDP, remains higher than the global average. Much of the growth in global debt levels has come from China where debt to GDP levels have risen significantly. In 2008, the World Bank pegged Chinese domestic credit at 100% of GDP. By 2015, this had risen to 150%.

Chinese debt has not yet reached extreme levels, but the rate of growth is more extreme than it was in the US between 1994 (when debt was 120% of GDP) and 2008 (when it reached a peak of 206%). Economies linked to China in the Asia-Pacific region (Australia in particular) have seen increases of similar magnitude. Latin America and the Middle East round out the regions where debt loads have increased, but levels remain relatively low, around 60-70% of GDP. China remains the biggest risk, since it has a relatively immature credit market which has seen enormous growth in the past decade.

In the US, equities markets have remained in a tight range for the past three years as consumers chose to reduce debt and forgo spending. The S&P 500 has continued trading between 1800 and 2200 since 2014. This can also be partly attributed to the tail end of the business cycle, with no immediate catalyst for either further growth or a retraction. At this stage, we would expect inflationary concerns to force interest rate hikes, but inflation is low to non-existent as consumers continue to reduce leverage and remain price-conscious. For the Fed, this remains a challenging period, with few answers available in textbooks. That said, we expect the Fed will raise interest rates in December, after the election is safely settled, likely by 0.25%.

Investors face similar uncertainties and we continue to advocate for cautious asset allocation and a focus on defensive companies and sectors.

The second quarter of 2016 saw some stabilization in global equities after a very volatile Q1. But this calm was short-lived as the surprise results of the Brexit vote roiled markets in the last weeks of the quarter.

We do not believe the Brexit referendum in itself will have a significant impact on the global investment climate or opportunities for investors. Whether the UK remains within the EU, or exits and reaches an alternate trade agreement with the EU, is of marginal significance to investors, especially those outside of Europe. The initial impact is almost certainly restricted to the UK itself, which may see a political disintegration if Scotland dissolves the union with England and Wales. Peripheral EU countries with significant deficits/debt (Greece, Spain, Portugal, Italy) would see a further erosion in confidence as a large, economically vibrant member leaves the EU. The financial industry in the UK is bound to see some contraction if Britain exits. The large London-based banks employ tens of thousands of workers, many carrying European passports. If the pool of available recruits narrows, banks are likely to expand offices in other cities. Dublin, Frankfurt and Paris are obvious alternatives, Switzerland is another continental (though non-EU) option. An exit will also mean personal data that pertains to EU nationals can no longer be stored or retained in the UK. This will impact technology companies and data-centers, where, as a result, the UK will find its market in those industries contracting as well.

An exit would permit the UK to enter into trade agreements with third (non-EU) countries, including former colonies such as India, with far more freedom than it would enjoy within the EU. After a period of adjustment, we would expect the UK economy to resume whatever long-term trajectory it would otherwise have had given demographic trends. The costs of adjustment if Britain does exit will be extensive. Regulations will need to be re-written, border procedures modified, passports re-issued, and undoubtedly the political costs will be enormous. Bickering over the result is bound to continue for years and indeed decades. But these costs will not continue into perpetuity.

This is not to say Brexit is insignificant. From a political perspective, it is extremely significant. It is yet another important signal that the enormous economic, demographic, environmental and political changes of the past few decades have left large segments of many populations with a sense of discontent and loss. Since the collapse of the Soviet Union, we have seen enormous changes in rapid succession. Technology has disrupted many industries, expanded markets and brought new competitors to formerly isolated corners of the world. Online marketplaces allow distributors to reach virtually every person in an increasingly connected world with ubiquitous network access. It has also led to an increasing concentration of wealth in many parts of the world. Environmental and political upheavals have created a historically high number of refugees fleeing war or lack of opportunity. Urbanization is on the rise virtually everywhere with populations moving to cities in record numbers. Large cities across the world, and their surrounding areas, have become ever more diverse and globally inter-connected. Asia, with its enormous population, has historically been the center of global trade and economic activity. After almost two centuries of relative decline, Asian economies are seeing rapid, sustained growth.

Brexit reminds us that these changes are unwelcome to many. Rural areas across the world, industrial areas in the western world, those with nationalist sentiments, and older populations everywhere see an erosion of all that is familiar and comforting. Every crisis is seen as an indictment of an global elite forcing such changes on a reluctant population. In many ways these political forces are not new. They have always been with us and have simply gathered force as the impact of changes has risen. Every era of change and migration has encountered some degree of resistance; this includes prior periods of urbanization and industrialization across the world. Yet, even in the recent UK referendum, 48% of voters, and large majorities of younger voters, opted for remain.

The broader question for us as investors is whether or not political systems will be able to manage these changes peacefully and with as little disruption to daily activity as possible. Quite clearly, this is not the case in many parts of the world. Our view is that democracies have a better chance of managing such change peacefully. Yet, even in the US, the remarkable strength of an openly nativist and populist candidate such as Trump should serve as a warning. Enormous changes such as those we have seen over the past three decades have to be managed with care lest they alienate large portions of the population. That alienation, if allowed to fester, can create a window of opportunity for disruptive forces to attain power. This would pose a real risk to continued stability and the prosperity and well-being that accrue from it.

Quite apart from the significant political risks ahead, equities markets are at cyclically-high valuations. Bond prices too are at high valuations with interest rates at low levels. In our view, as value oriented investors, we see limited rewards for taking excess risk. Accordingly, we continue to advise clients to maintain a relatively conservative portfolio allocation, keeping in mind their long-term objectives and recommended allocation.

Regards,

Subir Grewal, CFA Louis Berger

2016 Q1 letter: Negative interest rates cap a rocky quarter

The first quarter of 2016 saw market gyrations far rockier than many prognosticators had expected. A sharp drop in commodities prices and oil in particular sparked fears of a global slow-down and impacted all asset classes. Increased oil production in North America and the prospect of renewed imports from Iran led to expectations of a supply glut. Slowing economies in China, Brazil and Russia along with concern about potential slumps in the EU and US drove demand expectations down. Together, they combined to drive oil below $30 a barrel, causing great distress among the highest cost operators. Producers relying on deep sea projects (Brazil) and hydraulic fracturing (or fracking, in North America) have been among the most severely affected. Many small to mid-sized servicers and production companies are facing possible bankruptcy and have been liquidating assets. This has impacted the high-yield bond market (where many of these companies raised capital) and led to job losses in states where fracking had created small oil booms.

The commodity decline also caused steep retrenchment in various equity markets and drove the Federal Reserve to signal a pause in its plan to raise interest rates to 1% this year. The S&P 500 dropped as much 13% during the quarter and the MSCI Global stock index fell 11%. The S&P 500 has since recovered for the year, along with oil prices. In our view, the concerns that drove the asset market declines have not abated. Global growth continues to be weak and numerous markets are showing the signs of a waning seven year bull market. We would continue to urge caution when investing in risk assets across most markets.

Policy makers in several countries seem to have reached the end of their imagination when it comes to additional market stimulus. About 25% of the global economy now has negative interest rates. That includes the Euro-zone, Japan, Switzerland and Sweden. Banks are now being charged to maintain balances at the central bank. In a number of cases, banks have begun to pass these negative rates on to customers. This is bound to create great consternation. Depositors are not accustomed to being charged interest to maintain deposits. They may be used to seeing fees deducted from checking accounts, but most will be shocked to see savings accounts charged interest. In an environment where banks are already suspect in the eyes of many, this will lead to even more discontent.

From anecdotal evidence, customers have already begun to protest negative rates. We believe there is little sense in keeping rates negative for extended periods of time. In theory, it sounds reasonable to say there should be no zero-bound for rates. But humans are not theoretical creatures. We find being charged to keep our money in a bank rather strange, and customers will develop all sorts of behaviors to avoid this. These include keeping large sums of cash at home and purchasing safe haven non-financial assets (real-estate, precious metals etc.). Such behavior undermines the stated aims of negative rates, i.e. increasing the level of bank lending. The longer we maintain negative rates, the more distortions we introduce into the savings/money markets. In our view, this is not a policy that regulators should maintain for any period of time. It would be far more effective to apply fiscal stimulus in the form of government spending.

While markets have seemingly stabilized after a very volatile start to the year, we expect 2016 will see continued ups and downs with high risk assets remaining vulnerable to a price correction. We think this will present buying opportunities and we will continue to look for good entry points to buy equities we see as undervalued. We expect the market for bonds to remain very challenging for investors since rates are extremely low and corporate credit is deteriorating alongside the dip in global growth.

After almost seven long years at effectively zero interest rates, on December 16th the Federal reserve raised rates 25 basis points and signaled a handful of similar increases to come over the course of the year. This move was not unexpected, and there are numerous caveats and complications since so many unconventional tools have been used over the past seven years. That said, the unequivocal signal is that there has been a “regime change” at the Federal Reserve. We are moving from loose monetary policy to tighter monetary policy. Regardless of whether or not the Fed’s moves actually raise rates across the yield curve or reduce lending, the signal has been received and will have implications for capital markets. For several quarters, we have sought to limit maturities in client bond portfolios in preparation for such a move.

We expect US equity markets to be weighed down heavily by the hikes over the course of 2016. Though 1% may not seem like much, a 1% rise in rates can reduce the present value of a future cash flow stream by over 10%. We also expect significant political and tax-related uncertainty generated by an unusual election cycle in the US to affect stocks. Clients should expect the same headwinds to impact lower quality bonds as well.

Commodities have had a tough 2015 and we expect this to continue. Though we believe emerging markets (ex-China/Russia) will be one of the better performing assets of 2016, we do not believe this will flow into commodities markets which shall continue to be weighed down by reduced infrastructure build in China and dampened demand in the US and Europe. We have more detailed assessments for the year ahead in our top ten themes for 2016 (attached).

On the personal front, 2015 has been a fruitful year for us from both a personal and business perspective. Subir and Molly welcomed their second daughter, Rosalind into the world in June. We thank all our clients for their trust and confidence in us.

Regards,

Subir Grewal Louis Berger

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.

Dear Friends,

Dear Friends, Fed stays the course

Fed stays the course